Stocks: Nervousness Preceding NVDA Earnings Proves Unwarranted, Japanese Stocks Make First New High Since 1989, Chinese Stocks Stage A Comeback As The Government Steps Up Support

Download Weekly Market Commentary | February 26 2024

What We’re Watching:

- On Wednesday, we’ll get the second reading on fourth quarter GDP, with the expectation that economic growth holds at 3.3% with minimal revisions despite recent surprises.

- Core PCE is due out on Thursday with the consensus anticipating a decline from 2.9% to 2.8%, a move in the right direction on inflation but a miss to the upside may be taken as confirmation that market pricing of rate cuts is still too optimistic.

- ISM Prices Paid are expected on Friday, last month input prices were in focus after surprising to the upside, but it will be interesting to see if that trend continues as the January data is subject to construction noise.

- University of Michigan Consumer Sentiment is slated for Friday as well, with the forecast suggesting a flatline in sentiment from last month when the gauge moved up modestly.

Key Observations

- US equities stalled prior to Nvidia’s upside earnings surprise that rekindled market optimism, depicting how deserving a select few companies are of current valuations.

- Japan’s Nikkei 225 stock index made a new all-time high, its first since 1989, driven primarily by manufacturers and the semiconductor-related surge of AI enthusiasm.

- Fixed income indices found welcome reprieve last week as tighter spreads more than offset higher yields on short- dated treasury paper.

What Happened Last Week:

Stocks: Nervousness Preceding NVDA Earnings Proves Unwarranted, Japanese Stocks Make First New High Since 1989, Chinese Stocks Stage A Comeback As The Government Steps Up Support

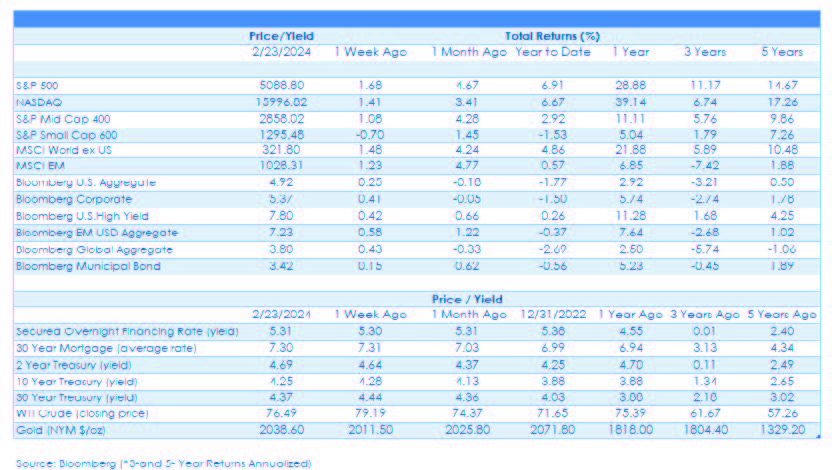

Another Upside Earnings Surprise Out Of Nvidia Drives Gains For The NASDAQ. Markets struck a cautious tone in the first half of the holiday-shortened trading week before ultimately marching higher as Nvidia impressed on earnings, pushing the S&P 500 up 1.6%. The change in sentiment was most apparent for the tech-heavy NASDAQ which pivoted from a 1.2% loss midweek to a 1.4% gain by Friday. There remains a host of reasons to stay skeptical on the short list of mega-cap names that sit atop the index, but for Nvidia, specifically, the stock is up over 1,020% since the end of 2019, but earnings have grown 1,060% during that same timespan. Admittedly this is a cherry-picked time frame, but that trend of prices tracking earnings shines through in the other top names as well with Apple seeing price appreciation of 142% and earnings growth of 335%. Artificial Intelligence (AI) is certainly permeating markets, at times used to superficially shield disappointing results, but select tech names like Nvidia are seeing shifts in their business that have translated to earnings. Sell-offs and earnings misses are inevitable quarter-to-quarter especially as analysts revise estimates higher, but long- term earnings growth aligns with market optimism. The broader semiconductor industry has benefited from the rising AI tide surging 2.9% last week and 11.6% since the start of 2024.

Record Highs Rolling In Abroad As Japanese Stocks Reach Highest Levels Since 1989. The Nikkei 225 made a new high for the first time in over 30-years this week, with the Index returning 16.8% year-to-date and outperforming all other markets up to this point. Gains this week of 1.6% were sourced from cyclicals including industrials and financials, with chipmakers lumped into the former sector. Currency moves have provided a tailwind for Japanese stocks, with the yen weakening in the last two-months as it did for most of last year, while interest rates remain anchored at current levels. That could start to shift should the Bank of Japan begin tightening policy, but the country’s recent GDP reading indicating a surprise recession introduces new concerns. Japan wasn’t alone in making a new high last week as the Euro Stoxx 600 also notched a record closing price above its 2021 peak. Notably, the record comes during a week in which the eurozone index returned just 0.8%. Markets appeared content with EU CPI flat for the month at 2.8%, but headline numbers could struggle as recent tailwinds from disinflation in electricity, gas, and fuel costs dissipate. PMI data out of France and Germany last week also left much to be desired, and for now we continue to prefer stronger fundamental and macro stories as the cheap valuations in Europe are simply not enough to interest us.

Policy Support Pushes Up Equity Prices In China. Chinese equities experienced a third consecutive weekly gain after washing out at the start of the month, on further government intervention in markets. This iteration of support was in the form of easing the country’s benchmark for mortgage rates and stepping up commitments for equity purchases from state-owned investment firms. The reduction in lending rates was a surprise move, but again these are minor tweaks relative to the colossal task of turning around the housing market. The proliferation of small-scale stimulus leaves us concerned that equities in the nation could become more dependent on cash infusions rather than a more durable improvement in investor confidence and potentially economic growth. Investors appear to have perked up as discussions around China again providing concessions in a push to garner international capital have swelled of late, but thus far they appear to be listening rather than putting capital to work in China.

Bonds: Corporate Spreads Tighten On Robust Demand; Japan’s Yield Curve Flattens As Front End Rates Rise and Emerging Bonds Benefit From High Yield Countries

US Corporate Bond Valuations Rise Further, Regardless Of Quality. The Bloomberg Investment Grade Corporate Bond Index returned a modest 0.4% on the week as spreads tightened to 89bps over Treasurys. Competition to own high grade corporate debt has been fierce with deal volume surpassing $53B as order books were approximately five times oversubscribed compared to last year’s average of three times. Concessions continue to grind lower, and AbbVie’s $15B offering last week was no exception with virtually zero new issuance premium. The debt proceeds were supplemental funding for recent acquisitions rather than more typical refinancing, another positive indicator for credit appetite. High yield credit spreads also narrowed, falling by 8bps to 306bps, in line with the high-grade index returning 0.4%. These levels are well below historical averages but positive signals from the labor market and economy make it tough to skip out on the excess yield in credit. Higher government bond rates took their toll on the front end of the yield curve, but long yields moved sideways or lower staying below the technical barrier for now, leaving most intermediate and long duration segments unphased.

Short Rates Rising In Japan On Central Bank Confidence. Upward pressure on global short-term rates last week had roots in the far east, as Japan’s yield curve flattened on wagers the Bank of Japan could be closer to its first hike than most developed nations are to their first rate cut. Despite the potential roadblock from Japan slipping into a surprise recession for the fourth quarter, markets anticipate minimal delay with futures still pricing the first hike from the BoJ coming in June. FOMC minutes affirmed that the Committee may be slower to cut, as the minutes emphasized concerns progress on bringing down inflation could stall while conceding the Fed funds rate still appear to be at its peak. Markets on the other hand may end up swinging too far on Fed rhetoric, with futures now pricing the first cut in July. We wouldn’t rule out late summer, but an over-correct in expectations could whipsaw those looking to trade around duration especially should we see better inflation prints in the coming weeks.

Emerging Market Debt Sees Strength Out Of Some Of The Riskiest Issuers. Lower rated countries benefited from an advance in risk-sentiment within developing country bonds as the Emerging Bond Index was one of the best performers, rising 0.6% last week. Argentina and Venezuela were the headline leaders, as reforms in the former are showing signs of uneven progress while J.P. Morgan disclosed a plan to reintroduce $53B in Venezuela bonds to its index suite. The decision was largely based on loosened trading restrictions that could be reactivated should unfair political practices reemerge, but the bonds’ nonperforming status likely precludes them from inclusion in actively managed portfolios until signs of life materialize. Argentina’s bonds saw price improvement as eclectic new president Milei’s government is instituting stark spending reforms that could curb the countries rampant inflation and currency devaluation. Morgan Stanley published a note citing concern from a political perspective but alluded to signs of potential austerity in keeping pacts to balance the budget and cut central bank spending entirely. Egypt and Sri Lanka experienced price improvements during the week as well, while high yield holdings in Africa declined.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.