Stocks: Tariff Pause, Well-Received Treasury Auctions Force Short Covering, But This Remains A ‘Sell The Rips’ Market; (Very) Early Returns From Earnings Season Encouraging; Take Note When Stocks Rise On ‘Bad News;’

Download Weekly Market Commentary | April 14 2025

What We’re Watching:

- Quarterly reporting season ramps up in a big way this week with 44 S&P 500 constituents slated to post results. Names such as Bank of America, Goldman Sachs, Netflix, and UnitedHealth Group are reporting this week, and could dictate the near-term direction for stocks, assuming an absence of market-moving news on the tariff/trade front.

- March Retail Sales are released Wednesday with the consensus expecting Control Group sales to rise 0.6% after a 1.0% rise in February.

- Initial Jobless Claims for the week ending April 12 and Continuing Claims for the week ending April 5 are released Thursday. Initial claims for unemployment insurance are expected to rise modestly to 225k from 223k the prior week.

Key Observations

- The U.S. announced a 90-day pause on reciprocal tariffs on its trading partners, excluding China, mid-day on Wednesday which led to short covering and a sizable rally in U.S. equity indices. The S&P 500 turned out its best one-day performance since October of 2008 on Wednesday, but market participants appeared eager to sell into any strength and forced the S&P 500 sharply lower on Thursday. Friday initially had the feel of a buyer’s strike as market participants didn’t want to be too long or too short going into a weekend, but stocks staged an afternoon rally as investors positioned for some positive market moving news.

- Treasury yields rose sharply over the balance of the week due to concerns that liquidity was drying up and that governments and central banks abroad would be less willing to buy U.S. government debt in the coming quarters as they seek leverage in trade negotiations. Results from 10- and 30-year Treasury auctions mid- week were encouraging and briefly allayed concerns surrounding demand from abroad. The move higher in yields appeared to attract some buyers late in the day Friday and the 10-year yield closed just a few basis points shy of 4.50%.

- The U.S. Dollar Index (DXY) weakened materially over the balance of the week, closing at its lowest level in three years. Dollar weakness alongside the sharp rise in Treasury yields is a worrisome combination as it points toward capital flight out of the U.S. The trend of capital being repatriated abroad may have further to go, putting additional downward pressure on the dollar and upward pressure on yields, providing a tailwind for foreign stocks and bonds and a headwind for U.S.-based assets.

What Happened Last Week:

Stocks: Tariff Pause, Well-Received Treasury Auctions Force Short Covering, But This Remains A ‘Sell The Rips’ Market; (Very) Early Returns From Earnings Season Encouraging; Take Note When Stocks Rise On ‘Bad News;’

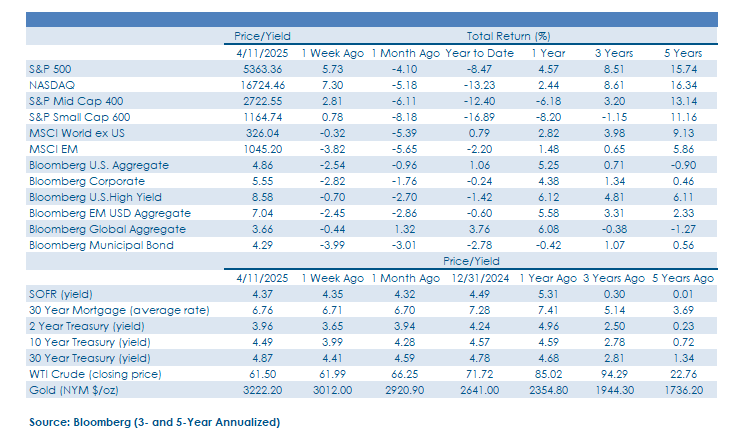

Announcement Of 90-Day Tariff Hiatus Spurs A Relief Rally, But This Still Has The Feel Of A ‘Sell The Rips’ Market As Trade Uncertainty Persists. The S&P 500 closed out a volatile week sharply higher, as U.S. large-cap stocks turned out a 5.7% gain and recouped some of the prior week’s sizable loss. Volatility remained elevated throughout the week as the S&P 500 traded in a 9% trough-to-peak range on Monday, which was both awe inspiring and unsettling, but that volatility paled in comparison to Wednesday’s 9.5% rally which saw the index higher by over 10% intra- day, as the index turned out its best single day return since October of 2008. The equally weighted S&P 500 rose 8% in Wednesday’s rebound, evidence of strong breadth, but many of the stocks that turned out the largest one-day gains were the most beaten down and heavily shorted names in the market, leading us to the view that the bulk of Wednesday’s rally was driven by short covering, not long- only investors buying the dip. This view was reinforced by the S&P 500 selling off by 3.4% on Thursday as investors took advantage of the market bounce to exit positions and re- hedge portfolios to prepare for a potential re-test of the Wednesday low. While the announcement of the 90-day pause on reciprocal tariffs is an undeniable positive, a 10% blanketed tariff remains in place on all U.S. trading partners, and the Trump administration has levied 145% tariffs on Chinese imports to the U.S., which is, in effect, a trade embargo on Chinese goods. The tariffs that are currently in place will lead to supply chain shifts and potentially rising costs in addition to tariffs, most of which could be passed through to retailers and consumers in the coming months. To what degree these higher costs negatively impact corporate profits remains to be seen, and a cloud of policy uncertainty will remain over stocks as market participants attempt to reevaluate what they are willing to pay for an increasingly uncertain earnings outlook. We expect continued volatility and continue to wait patiently for U.S. stocks to find support and carve out a base before becoming more constructive.

When ‘Bad News’ Lifts Stocks Take Note. Prior to Wednesday’s announcement that tariffs on a broad swath of our trading partners would be paused for 90-days, household names Delta and Walmart both withdrew earnings guidance before the market opened, citing tariff uncertainty as the primary reason for doing so. We weren’t surprised that these companies decided not to provide an earnings outlook and we expect most of the S&P 500 to do the same when they post quarterly results in the coming months. However, we were surprised at the share price reaction to the news as both Delta and Walmart were top-5 performers in the index even prior to the tariff announcement spurring a broad- based rally.

Little Lift For Small Caps Despite Tariff Delay. News of the 90-day stay on tariffs mid-week brought about a lift in domestic equities, broadly speaking, but the S&P Small Cap 600 lagged the S&P 500 in all five trading days last week and rose just 0.7% on the week. This is a sign that investors don’t believe the tariff reprieve will leave companies heavily tied to U.S. economic growth in the clear. Market participants appear concerned that 10% blanketed tariffs on the U.S.’ trading partners threaten already thin profit margins of smaller U.S. companies, and the backup in interest rates last week only fueled pessimism surrounding companies already struggling with higher financing costs. Technical indicators are suggesting pessimism could be peaking as just 13% of S&P 600 constituents were trading above their 200-day moving average late last week, a level last seen in late 2022 and early 2020. This has been a painful re-rating for small caps, with the forward price to earnings ratio for the S&P Small Cap 600 going from 15.7x at the start of the year to now just 10.9x halfway through April, but the multiple has only finished the month below the current level five times in the last 20-years. A steep valuation discount isn’t enough on its own to warrant new capital moving into this segment of stocks, in our view, but assets trading this cheap can see strong reversals and rallies, particularly in bear markets, justifying continued exposure to this cohort of stocks.

U.S./China Tensions Ripple Through Mainland Markets.

Last week we entered the escalation phase of what has the look of a trade war between the world’s two largest economies, the U.S. and China. The MSCI China index fell by 8.8% ove r the course of the week while U.S. large cap stocks gained 5.7% as the two countries hurled tit- for-tat tariffs at one another. At current lofty levels there is little reason to raise import taxes further, so we could be set to enter a new phase of these ‘negotiations.’ One commonality both countries share is the belief that they are in a position of strength and that the other will cave first, as President Trump has stated his belief China will come to the negotiating table while Chinese officials appear content to endure near-term pain after taking countermeasures. Policy makers in China floated potential stimulus measures last week to help mitigate the negative impacts of decreased U.S. demand, likely depreciating the yuan to increase their ability to ease policy, or even stepping in to buy financial assets. This duel has room to devolve further as the prospect of delisting Chinese ADRs in the U.S. has been tossed around, but neither country stands to benefit economically from escalating the situation. Outside of China, broader emerging markets benefited from the steep drop in the U.S. dollar as the MSCI Emerging Equity Index generated a 1.6% total return, breaking a three-week losing streak for the benchmark.

Bonds: A Rollercoaster Week For Treasury Yields Ends With The 10-Year Yield 50-Basis Points Higher; A Trio Of Closely Watched Treasury Auctions Shows Robust Demand From Abroad; March CPI Cools More Than Expected, But Has Little Impact On Yields As It Is Viewed As A One-Off.

Sharp, Unsettling Rise In Treasury Yields Has Our Attention.

Volatility in the rates market ramped up last week with the ICE BofA MOVE Index, the bond market’s version of the VIX, making a new 12-month high as 10-year yields topped 4.5%. The 10-year Treasury yield closed higher every day last week and jumped by 26-basis points on Monday alone on its way to a jaw dropping 50-basis point weekly rise. At least part of the sharp run-up in rates was chalked up to the potential unwind of the oft-discussed basis trade put on by leveraged hedge funds. Simplistically, the basis trade is an attempt to take advantage of perceived mispricing between Treasury bonds and corresponding futures. For instance, if a specific futures contract is cheaper than the cash bond, hedge funds buy the futures exposure to profit when they ultimately converge to one another at expiration. That trade on its own is fairly low risk and low return, but to increase the return funds add leverage, far more leverage than would be acceptable on riskier assets due to the low-risk nature of the trade. Issues arise for the basis trade when interest rate volatility spikes as it did last Monday as those trades take on losses and create deleveraging that shakes out traders before the futures can converge to the underlying cash bond. Another oddity is the dollar decline last week despite Treasury yields moving sharply higher, which is a potential sign that foreign Treasury holders are moving out of U.S. government debt with depressed trading flows requiring fewer U.S. dollar-denominated assets to balance their respective currencies.

Trio Of Treasury Auctions Garner Attention, Allay Concerns Surrounding Demand From Abroad. The U.S. Treasury auctioned off $58B of 3-year notes on Tuesday, $39B of10- year notes on Wednesday and closed out the week with a $22B issue of 30-year bonds on Thursday. More than any other auctions in recent memory, the 10- and 30-year issues were closely watched due to rising fears of decreased demand for U.S. Treasuries from foreign central banks. While this is a significant amount of supply, the results of these auctions, particularly for the 10- and 30-year securities, allayed those concerns as issuance was met with strong demand from abroad. Indirect bidders, most often foreign governments or central banks abroad, took down 67% of the 10-year auction and just shy of 62% of the 30-year issue, figures above recent auction averages that indicate foreign buyers are still very interested in buying/owning long-dated U.S. Treasuries. The recent back-up in yields likely helped generate interest, and the U.S. dollar continuing to slide in recent weeks has lowered hedging costs for some foreign buyers, making U.S. Treasuries relatively more appealing.

Inflation Cools In March But Appears To Be A One-Off Rather Than The Start Of A Trend. The March Consumer Price Index (CPI) was released Thursday with the headline reading falling 0.1% month over month, below the +0.1% consensus estimate, and year over year CPI came in at 2.4%, below the 2.5% estimate and the 2.8% reading in February. Core CPI, which is more closely watched by policymakers, rose just 0.1% month over month, also below the 0.3% estimate, and year over year core CPI rose 2.8%, below the 3.0% estimate. Falling energy prices, air fares, and lodging rates put downward pressure on the March CPI, while rising prices for used motor vehicles acted as a partial offset. While the CPI release was better than feared, with 10% tariffs going into effect on the U.S.’ trading partners last week and with few signs that tariffs were passed through to retailers and consumers in March, market participants appeared to be rightfully skeptical that this is the start of a sustainable trend of lower inflation readings. The cooling March CPI is likely to be a one-off and Treasury yields were little changed on the heels of the release, while Fed funds futures were pricing in three 25-basis point cuts by year-end on Friday, a downshift from the four quarter-point cuts expected at the end of the prior week.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.