Stocks: S&P 500 Makes A Move Back Toward 6,000, Potentially Setting Up For A Year-End Santa Claus Rally; Small-Caps Surprisingly Strong As Biotech Bounces; Dollar Strength To Remain A Drag On Emerging Markets.

Download Weekly Market Commentary | November 25 2024

What We’re Watching:

- The Conference Board releases its November Consumer Confidence Survey on Tuesday and a rise/improvement to 111.8 from 108.7 in October is expected.

- Minutes from the Federal Open Market Committee’s October meeting will be released Tuesday and could provide additional insight into the Committee’s thinking regarding future rate cuts and lead market participants to ratchet expectations for a cut in December higher or lower in response.

- October Personal Consumption Expenditure (PCE), the FOMC’s preferred inflation gauge, is released Wednesday. Headline PCE is expected to rise 0.2% month over month and 2.3% year over year versus 0.2% and 2.1% readings in September. Core PCE is expected to rise 0.3% month over month and 2.8% year over year versus 0.3% and 2.7% the prior month.

Key Observations

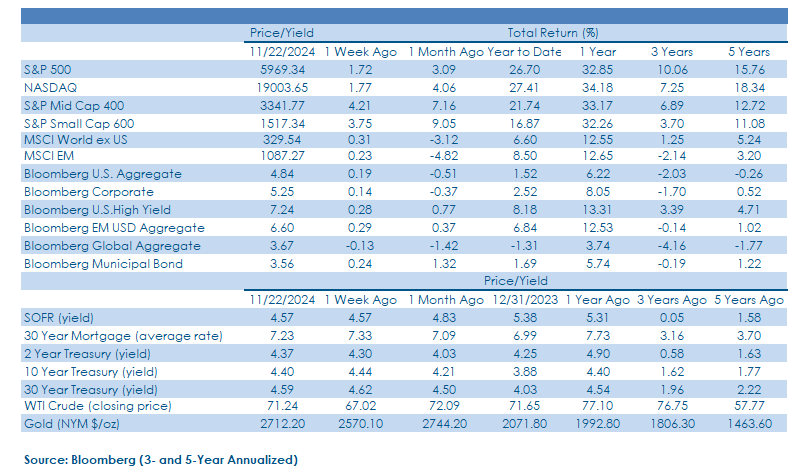

- U.S. stocks shrugged off rising geopolitical tensions to end the week in positive territory as the S&P 500 continued to digest post-election gains. Smaller capitalization stocks outperformed their large-cap peers as the consumer discretionary, financial services, health care, and industrials sectors, which together account for over 60% of the S&P 600 index, continued to rally.

- With Nvidia earnings in the rearview mirror, U.S. stocks could be poised to move higher post-Thanksgiving into year-end as a positive seasonal backdrop, an absence of tax-loss selling, and ample liquidity boost animal spirits. While we expect large-caps to outperform small- and mid-cap (SMid) into year-end, SMid should still participate in any Santa Claus rally as ‘good cheer’ boosts sentiment and risk appetite for a bit longer.

- U.S. Treasuries caught a ‘flight-to-safety’ bid early in the week on rising geopolitical tensions between Russia and the United States, but fixed income investors ultimately clipped their coupons as yields closed the week little changed. Relative calm has returned to the Treasury market in the past two weeks with yields steady, but interest rate volatility could ramp up in the coming weeks with inflation data (PCE) and the November nonfarm payrolls report potentially market moving.

What Happened Last Week:

Stocks: S&P 500 Makes A Move Back Toward 6,000, Potentially Setting Up For A Year-End Santa Claus Rally; Small-Caps Surprisingly Strong As Biotech Bounces; Dollar Strength To Remain A Drag On Emerging Markets.

U.S. Large-Cap Stocks Working Off Post-Election Euphoria, Potentially Setting Up For A Retest Of All-Time Highs Before Year-End. U.S. large-cap stocks shrugged off rising geopolitical tensions to close with a 1.7% weekly gain in the lead-up to the holiday-shortened Thanksgiving holiday. Early in the week, rising tensions between the U.S. and Russia weighed on risk appetite and pulled U.S. stocks lower leading to a continuation of the drawdown experienced the prior week, but buyers began to step in Tuesday afternoon and again late Wednesday in the lead up to Nvidia’s earnings release. Nvidia posted impressive results with 94% year over year earnings growth garnering headlines, but the stock initially traded lower on the heels of the release as results fell short of lofty expectations. Encouragingly, dip buyers quickly stepped in, and the stock ended the day with a 0.5% positive return but ultimately sold off sharply Friday and closed out the week virtually unchanged. Performance out of the ‘Magnificent 7’ was a mixed bag on the week with four constituents ending higher (Apple, Meta, Microsoft, and Tesla) two closing lower (Alphabet, Amazon), and one unchanged (Nvidia). Nvidia’s report could prove to be a clearing event of sorts with earnings season winding down and 70% of the S&P 500 still trading above their important 200-day moving average, and we expect U.S. stocks to climb higher from Thanksgiving through year-end as a positive seasonal backdrop, ample liquidity, and elevated corporate buyback activity provide tailwinds.

A Surprisingly Strong Week For Small Caps, With Growth Outperforming Value. With the S&P 500 generating a 1.7% weekly gain, we would have expected the S&P Small Cap 600 Index to close the week higher, which it did by 3.7%, but what stood out to us was the positive momentum behind the S&P Small Cap 600 Growth Index which jumped 4.2%. After digging into the driver(s) behind the 600 Growth’s weekly gain, we were pleasantly surprised to see health care as the one of the biggest contributors after the sector rose 5.7% on the week, outperforming the S&P 500 health care sector’s more modest 1.6% return. The health care sector overall and pharmaceutical stocks, specifically, have lagged meaningfully post-election due to uncertainty surrounding the impact Robert F. Kennedy’s appointment as Director of Health and Human Services (HHS) could have on drug and vaccine manufacturers. A great many high-profile names in the pharmaceutical and biotechnology industry groups reached deeply oversold territory in recent weeks, and we believe the selloff in most cases to be overdone and based on little more than fear at present. The selloff in health care stocks in recent weeks is one of many dislocations we can point to post-election as providing an opportunity for longer- term investors to potentially take advantage of.

A Half-Hearted Bounce Out Of Emerging Markets As Dollar Strength Remains A Headwind. The MSCI Emerging Markets (EM) Index eked out a relatively paltry 0.2% weekly gain as strength out of India, South Africa, South Korea, and Taiwan was offset by weakness out of China and Mexico. We were pleased that the EM Index was able to close the week in positive territory given the Bloomberg U.S. Dollar Index, or DXY, made a two-year high above 107.50 on Friday. However, with the dollar strengthening due to a combination of better expected U.S. economic growth and the prospect of new tariffs being levied on China and Mexico, among others, it’s likely that EM, broadly speaking, remains a challenging spot to deploy capital into 2025. The DXY has rallied over 6.5% just since the end of September, so some near-term give back wouldn’t be a surprise, but with trade uncertainty set to dominate in the first half of 2025, and with optimism building that U.S. economic growth could surprise to the upside next year due to potential deregulation and other pro-growth policies out of the Trump administration, we are increasingly of the belief that U.S. dollar strength could be a secular, not cyclical phenomenon. With this backdrop in place, it is increasingly difficult to paint a positive picture for emerging market stocks and bonds.

Bonds: Treasuries Briefly Boosted By A ‘Flight-To-Safety’ Bid, But End The Week Little Changed; Corporate Bonds Continue To Give Stock Investors The ‘All Clear;’ PCE This Week And November Nonfarm Payrolls Post-Thanksgiving Worth Watching, Could Shift December Rate Cut Odds.

Yields Stuck In Neutral As A ‘Flight To Safety’ Bid Only Briefly Boosts Treasuries. The safe-haven status of U.S. Treasuries pulled in capital early last week as geopolitical tensions flared with saber-rattling between Russia and the U.S. ramping up, but downward pressure on Treasury yields was muted in magnitude and short lived. The 10-year Treasury yield, specifically, continued to trade in an extremely tight range between 4.40% and 4.45% over the balance of last week and the longer it continues to do so the larger the move out of that range is likely to be. We believe odds favor the next 15-20 basis point move on the 10-year being higher due to inflationary pressures remaining sticky, with a potential re-test of the late May level of 4.62% potentially in the cards on the heels of this week’s release of the November Personal Consumption Expenditure (PCE). Conversely, if PCE is cooler than expected, Treasuries could rally, and the 10-year yield fall back into a trading range between 4.25% and 4.40%.

Credit Spreads Remain Tight, Supportive Of Risk Taking Into Year-End. Investors in most segments of the fixed income market were in coupon-clipping mode last week, and that was also true for those allocated to investment- grade and high yield corporate bonds. The Bloomberg U.S. Corporate Index ended the week with a 0.1% gain while the Bloomberg U.S. High Yield Corporate Index fared a bit better, rising 0.2%. Credit spreads on investment- grade and high yield corporate bonds remain within just a few basis points of year-to-date tight levels and only widened modestly as profit taking hit stocks the week before last, evidence that investors believe current yields adequately compensate them for taking credit risk, largely due to optimism surrounding the U.S. economy. Market participants often view corporate bonds as a canary in the coal mine for stocks as, historically speaking, a selloff in riskier corporate bonds portends downside and/or volatility ahead for equities. With that in mind, at present, tight credit spreads on corporate bonds appear to be pointing toward a constructive backdrop for risk taking and likely additional gains for stocks and riskier corporate bonds into year-end.

After PCE This Week, November Nonfarm Payrolls Becomes The Next Data Point Worth Watching. The October nonfarm payrolls report released earlier this month showed just 12k jobs were created last month, but the report was largely dismissed and viewed by market participants as little more than noise given the negative impact of hurricanes, worker strikes (Boeing), and the reversal of positive seasonal adjustment factors. The October payrolls report likely had no impact on the FOMC’s decision to cut the funds rate earlier this month given the noisiness in the release, but the November payrolls report released the first Friday in December could alter the path forward for the Fed. The current consensus estimate calls for 175k jobs to have been created during the month, but last week state-level data was released that has market participants wondering if payrolls growth might surprise to the upside in November, perhaps surprisingly so. The Fed funds futures market views the likelihood of a cut at the FOMC’s December meeting as a coin-flip, but still favors a cut ever so slightly over a pause. A strong November payrolls report would likely give the Committee greater confidence that the labor market is on firmer footing into year-end and lower the probability of a rate cut next month. Our base case still calls for a 25-basis point cut in December, followed by a pause in January.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.