Stocks: U.S. Large Cap Stocks Shrug Off Government Shutdown, Close The Week At An All-Time High; Selling Into Government Shutdowns Has Historically Not Been Rewarded; Small Caps Rally As Rate Cut Hopes Rise; Foreign Markets Outperform The U.S. With Emerging Outpacing Developed.

Download Weekly Market Commentary | October 6 2025

What We’re Watching:

- Minutes from the FOMC’s September meeting are released Wednesday and will be analyzed for clues as to what the Committee may do when it meets later this month.

- The preliminary University of Michigan monthly Consumer Sentiment survey for October is released Friday. The reading is expected to fall to 54.0 from 55.1 in September.

- We will be monitoring any movement out of Washington D.C. with the hopes that the government shutdown will be of short duration and that economic data will begin to flow again in short order.

Key Observations

- Despite the U.S. government shutdown, the S&P 500 bounced back from a modest loss the prior week to close out a strong 3rd quarter on a high note. The information technology and utilities sectors remained leadership for the second consecutive week, but health care was the biggest winner as biotechnology and pharmaceutical stocks rallied sharply. The energy sector was the top performer two weeks ago and proceeded to give back the bulk of those gains this past week, so it will be interesting to see if the momentum pushing the health care sector higher is sustained.

- Eurozone and U.K. equities powered the bulk of the gains generated by the MSCI EAFE developed markets index on the week, with strength broad-based in the Eurozone for what feels like the first time since May. China, South Korea, and Taiwan continued to pull the MSCI EM index higher, while Brazil and Mexico experienced modest profit taking after strong year-to-date performance.

- The U.S. equity market barely seemed to notice that the U.S. government shut down last Tuesday, but the Treasury market was prone to overreaction as yields moved lower on the heels of the September ADP employment report Tuesday. This release typically takes a back seat to the more closely watched nonfarm payrolls report, but with the government shutdown delaying that release and many others in the coming week(s), investors will look to other data sources to impact portfolio positioning.

What Happened Last Week:

Stocks: U.S. Large Cap Stocks Shrug Off Government Shutdown, Close The Week At An All-Time High; Selling Into Government Shutdowns Has Historically Not Been Rewarded; Small Caps Rally As Rate Cut Hopes Rise; Foreign Markets Outperform The U.S. With Emerging Outpacing Developed.

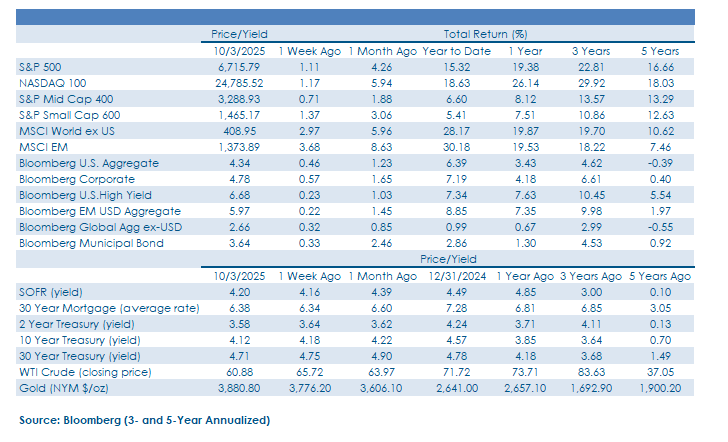

U.S. Indices Bounce Back, Close Out Strong 3Q On A High Note. The shutdown of the U.S. government garnered headlines throughout last week, but U.S. equities barely seemed to notice. The S&P 500 closed at a new all-time high on Wednesday, Thursday, and again on Friday with information technology and utilities carrying the leadership baton for the second consecutive week, but the health care sector was the big winner, rising 6.8% on the week. Biotechnology stocks were a notable standout performer across the market capitalization spectrum on the week, evidenced by a 7.1% weekly gain out of the iShares Biotech ETF (IBB). Headwinds for biotechnology and pharmaceutical companies appear to be easing and the backdrop for mergers and acquisitions (M&A) activity is looking more constructive, leading investors consistently underweight these groups to revisit their thought process and positioning. Among notable laggards were the communication services, energy, and financials sectors. Energy was the best performing sector the prior week and investors seemed eager to take profits as the price per barrel of West Texas Intermediate (WTI) crude oil almost $5 on the week to close at $60.88, less than $4 above the year-to-date low made in May. For the financials, the culprit behind weakness in the sector appeared to be the ADP employment report which put downward pressure on yields on long-term U.S. Treasuries and led to a flattening of the yield curve, a net negative for the sector due to its sizable exposure to banks.

No Guarantee History Repeats, But Buyers Amid Past Government Shutdowns Have Been Rewarded. Historically, government shutdowns have proven to be more bark than bite for stocks. Initial weakness in U.S. equity indices due to angst surrounding how long the government might be shut down and the impact the shutdown might have on the U.S. economy has more times than not proven to be a buying opportunity. In the latest instance which could provide a baseline for investors, the U.S. government partially shut down from December 22, 2018 through January 25, 2019 – this also happened to be the longest shutdown on record at 35 days – and the S&P 500 was higher by 23.3% on a total return basis in the subsequent 6-months, and 36% for the 12-months post-shutdown. It’s worth pointing out that this is a full government shutdown, not a partial one like we saw in 2018 – 2019, and there’s no guarantee the S&P 500 will turn out gains of this magnitude this time, the point remains that selling amid shutdowns has historically not been rewarded.

Small Caps Rebound As Rate Cut Hopes Rise On Weak ADP Report. The S&P Small Cap 600 index rallied 1.3% last week, outpacing the S&P 500 due to impressive upside moves out of the consumer discretionary, health care and industrials sectors. Small caps caught a bid after the weak ADP Employment report caused investors to raise their expectations for cuts to the Fed funds rate in the coming months. As was the case for the S&P 500, pharmaceutical and biotechnology stocks were big winners in small cap land and this cohort of stocks could continue to garner interest into year-end and beyond as potential candidates for mergers and acquisitions (M&A) activity.

Foreign Equity Markets Outperform On The Week. Foreign stocks, broadly speaking, fared better than U.S. indices on the week. The MSCI EAFE developed markets index benefitted from a bounce in Eurozone and U.K. stocks, while Japan posted a modest decline. Notably, after marking time throughout the summer months, Eurozone stocks caught a bid last week behind improved breadth. Country indices tied to Germany and Switzerland rose 3% and 4.7%, respectively, on the week, while France turned out a 2.9% weekly gain. The U.S. dollar weakened modestly, and it’s possible that foreign capital riding the rally in U.S. stocks in recent months was repatriated and reallocated into local markets due to the U.S. government shutdown injecting uncertainty into the outlook for U.S. economic growth. The MSCI Emerging Markets (EM) index continued to outpace its developed markets counterpart as it was pulled higher by China and South Korea, which together account for over 40% of the index and rose 4.1% and 6.2%, respectively.

Bonds: Investors And Policymakers ‘Flying With A Foggy Windshield’ As The U.S. Government Shuts Down; Treasuries Likely In A Holding Pattern Until The Government Reopens; In A Data Desert, Fixed Income Investors Will Need Patience Above All Else.

Modest Downward Bias To Yields, But Trading Activity, Volatility Could Wane As Economic Data Dries Up. There was a downward bias to U.S. Treasury yields across the curve early last week as the weak ADP Employment report on Tuesday struck a cautious tone for the bond market. However, in the wake of the government shutdown, economic data ground to a halt, with trading activity and volatility in the fixed income market following suit. In the absence of potentially market-moving data until the government reopens, our base case would call for Treasuries to be in a holding pattern with yields not straying very far from last week’s closing levels over the near-term. The Bloomberg Aggregate Bond index has produced a respectable 6.4% year-to-date total return through last week, but with credit spreads tight and a current yield-to-worst on the index of 4.3%, investors should focus on diversification to help smooth out the ride should volatility ramp up as the government reopens.

Corporates Ride The Coattails Of Treasuries To A Weekly Gain, But The Seasonal Backdrop Turns Unking In October. The Bloomberg Corporate index rose 0.5% on the week as credit spreads ended the week little changed but the fall in Treasury yields led to price gains for longer duration bonds. In recent years, the month of October has presented headwinds for investment grade corporate bonds, evidenced by the Bloomberg Corporate index falling 1% or more during the month in each of the last three calendar years. Strength in September, which saw the index rise by 1.5% with credit spreads narrowing, will make it difficult for IG corporates, broadly speaking, to rally much more in the near-term. After closing out a month in which we saw north of $200B of high-grade issuance, activity in the corporate bond market should slow in the coming month, serving to prop up higher quality bonds. But we would temper expectations at present and look to revisit this segment of the fixed income market in November after some of the dust has settled.

Bond Market Left To Take Its Cue From Other Sources As Government Shutdown Leads To An Economic Data Desert. Last week, we received the Job Openings and Labor Turnover Survey (JOLTS) from August and the September ADP Employment report, two reports that took on added importance as the U.S. government shutdown delayed the release of the closely watched September payrolls report. August JOLTS pointed toward 7,227k open positions during the month, slightly above the estimate of 7,200k. More jobs open and available than expected during the month, along with both quits and layoffs falling below estimates provided some reasons for optimism surrounding the health of the labor market, but the report is quite stale at this point. The ADP Employment report for September was less encouraging but quite noisy. The ADP release showed job losses of 32k during the month, well below the estimate of a gain of 51k. The headline reading spurred a rally in U.S. Treasuries as yields moved sharply lower, but that appears to have been an overreaction as the bulk of the miss versus the consensus estimate was due to a combination of benchmarking changes undertaken by ADP and seasonality which downwardly biased the data. The labor market is cooling, but not to the degree the ADP report on its surface would indicate. We were eagerly awaiting the September nonfarm payrolls report due last Friday, but that data release has been delayed indefinitely with the U.S. government going into partial shutdown mode last Tuesday, In the absence of data derived from the U.S. government, investors and monetary policymakers will increasingly need to rely on data such as the ADP report that in normal times are rarely market moving. How long the government shutdown lasts is anyone’s best guess, but Treasury bonds could be in a holding pattern with investors likely clipping coupons as we enter an economic data desert until it reopens. That dynamic could shift quickly and give way to elevated volatility in the bond market as investors recalibrate their expectations once data starts to flow as usual but, for now, patience is required and should be rewarded.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.