Stocks: U.S. Indices Post Gains Despite Credit Fears, Trade Uncertainty; Big Banks Kick Off Earnings Season With Positive Results; Record High For Small Caps As FOMC Chair Strikes A Dovish Tone; Eurozone, Japanese Equities Rally, While Strength Out Of South Korea Is Offset By Weakness Out Of China.

Download Weekly Market Commentary | October 20 2025

What We’re Watching:

- Quarterly reporting season ramps up in a big way with 122 companies in the S&P 500 slated to post results in the coming week.

- The U.S. Consumer Price Index (CPI) for September is released Friday with the headline reading expected to rise 0.4% month over month and 3.1% year over year, which compares to 0.4% and 2.9% readings last month. Core CPI, which is more closely watched by policymakers, is expected to rise 0.3% month over month and 3.1% year over year, which would fall in-line with readings from the prior month. Should the data come in as expected, this would provide further evidence that inflationary pressures remain sticky but are not at risk of becoming unanchored, which could give the FOMC comfort to cut the Fed funds rate later this month.

- S&P Global releases its monthly Purchasing Managers Index (PMI) for October on Friday. Manufacturing PMI is expected to fall to 51.8 from 52.0 while Services PMI is projected to fall to 53.5 from 54.2 the prior month. A reading above 50 indicates expansion or growth, below 50 contraction.

Key Observations

- Credit concerns rippled through stock and bond markets, generating volatility and weighing on investor risk appetite over the balance of the week. Two high profile bankruptcies made headlines and generated chatter surrounding whether these were isolated events or more systemic in nature and evidence of cracks forming in the credit market. We see these credit-related hiccups as one-offs at present, but with stocks and corporate bonds richly valued, a reset for positioning, sentiment, and valuations would likely be a healthy event, and could occur via time or price.

- Some of the ‘froth’ came out of highflyers tied to the AI theme and buildout of data center infrastructure last week, but broader U.S. indices still managed to finish with gains. This is ideal for keeping the rally going as some of the more overbought areas cooling off as capital rotates between sectors leaves indices on firmer footing into the seasonally strong November through January stretch in the calendar.

- The bankruptcies of auto parts supplier First Brands and subprime auto lender TriColor created skittishness in the equity market, but indices tracking investment grade, high yield, and leveraged loans in the corporate bond market barely seemed to notice. This resiliency is noteworthy, but we will be monitoring these areas in the coming weeks for any widening of credit spreads and potential signs of stress.

What Happened Last Week:

Stocks: U.S. Indices Post Gains Despite Credit Fears, Trade Uncertainty; Big Banks Kick Off Earnings Season With Positive Results; Record High For Small Caps As FOMC Chair Strikes A Dovish Tone; Eurozone, Japanese Equities Rally, While Strength Out Of South Korea Is Offset By Weakness Out Of China.

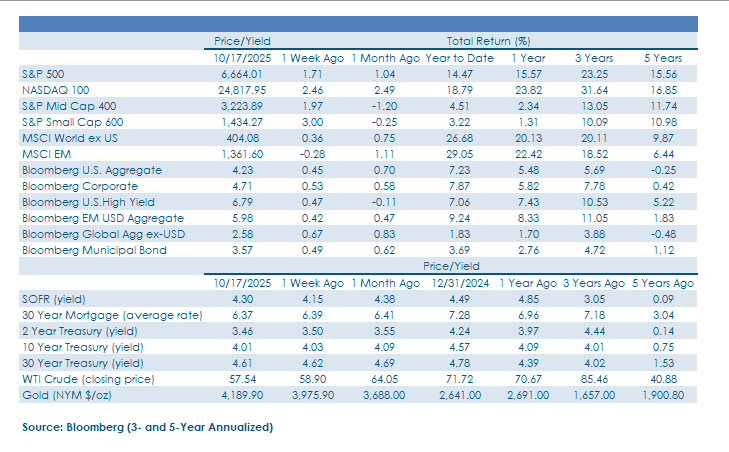

U.S. Indices On Healthier Footing Into Year-End After Last Week’s Positioning, Sentiment Shift. The U.S. and China continued to trade jabs surrounding China’s curbs on exports of rare earth minerals which are used in a broad swath of high-tech applications. This is a hot button issue in Washington D.C. due to negative implications for the U.S. military industrial complex should rare earth minerals need to be sourced elsewhere. This led to concerns that a trade war between the two countries was potentially back on after a six-month hiatus. While trade rhetoric dominated headlines early in the week, it took a back seat to credit concerns as comments made by J.P. Morgan’s CEO, along with a couple of smaller regional banks reporting credit losses tied to alleged fraud, led to concerns that some recent high profile bankruptcies could be just the tip of the iceberg with more “cockroaches” likely to come into the light in due time. Trade and credit concerns weighed on risk appetite over the balance of the week, but the S&P 500 still managed to eke out a 1.7% weekly return and recoup some of the prior week’s losses, while small cap stocks fared even better. We suspect credit concerns will subside, but it may take another week or two for positioning and sentiment to sufficiently reset after such a sizable and unchecked move higher for U.S. indices off the April lows. We remain constructive on U.S. stocks into year-end and expect quarterly earnings and a reopening of the corporate buyback window to ultimately turn the tide back toward the bullish camp, but it may be November before we see those tailwinds materialize.

Big Banks Post Big Earnings Beats, Set Positive Tone, But Credit Concerns Weigh On Regionals. The financial services sector of the S&P 500 closed the week lower by 0.3% as strong earnings results out of Bank of America (BAC), Citigroup (C), J.P. Morgan (JPM), and Wells Fargo (WFC), along with Goldman Sachs (GS) and Morgan Stanley (MS) set a positive tone for the sector, but were overshadowed by credit concerns out of a small cadre of regional banks into the weekend. On balance, management team’s struck an optimistic tone surrounding the state of the U.S. economy, but J.P. Morgan’s leadership cited a $170 million charge-off tied to loans made to subprime car lender Tricolor Holdings as “not our finest moment,” and noted that the bankruptcies of Tricolor and auto parts supplier First Brands could be the tip of the iceberg after more than a decade of easy credit. The ‘Big 4’ banks, along with Goldman and Morgan Stanley, posted positive results last week with the group expecting robust capital markets activity (equity/debt underwriting, M&A) in the coming quarters and pointing toward a resilient consumer set an upbeat tone for earnings season. But those constructive comments took a backseat to credit concerns as regional banks Zions and Western Alliance disclosed credit losses tied to the same alleged fraud in the non-depositary financial institution space, which spurred selling across the financial services sector.

Small Caps Rally As FOMC Chair Powell Strikes A Dovish Tone. While risk appetite was subdued over the balance of last week due to the ongoing U.S./China trade spat and concerns surrounding the credit market, the S&P Small Cap 600 still gained 3% on the week and outpaced the S&P 500. The rally in small caps accelerated Tuesday as FOMC Chair Jerome Powell made remarks that market participants took to imply he was supportive of a rate cut later this month, and perhaps another in December, while he also noted that it could be appropriate to end balance sheet runoff, or quantitative tightening (QT), in the coming months. Taken together, less restrictive monetary policy in the coming months, along with the end of QT could keep a lid on yields and lower borrowing costs for smaller companies in a material way.

A Good Week For Eurozone, Japanese Stocks, While China’s Losses Offset South Korea’s Gains. The MSCI EAFE developed markets index rose 0.6% on the week, while the MSCI Emerging Markets index continued to digest sizable gains from August and September and fell 0.3%. Developed market indices were buoyed by Eurozone and Japanese stocks while the U. K’s FTSE 100 index closed little changed. Measures of near-term breadth or participation have improved in the Eurozone and U.K. in the past month, which is encouraging after the EAFE marked time from May through August. The most notable moves on the week occurred in developing country indices tied to China and South Korea, with the former falling 3.8% and the latter rising 4.3%, serving to offset one another. We remain more constructive on emerging markets than we are on developed markets abroad but acknowledge that recent price action appears supportive of further gains for both areas into year-end.

Bonds: Treasuries Rally As Risk Appetite Wanes On Corporate Credit Concerns; 2-Year Yield Gives The Fed Cover To Cut Later This Month; No Signs Of A Rush To The Exits In Riskier Corporate Bonds.

Skittishness Spurs Treasury Rally, But Upside For Prices Of Long Bonds Likely Remains Limited. The 10-year U.S. Treasury yield dipped below 4% intra-day last Thursday for the first time since Liberation Day in early April but failed to close out the week below that level. With the 10-year yield still holding above 4% at last Friday’s close, our view on long-term Treasuries remains that upside to total return/downside for yields is limited in the near-term, but with trade and credit uncertainty dominating, near-term downside for price/upside for yields is also likely limited. We remain of the opinion that bond investors are in a clip your coupon environment for the foreseeable future, and it would take a weekly close below 3.85% or above 4.20% on the 10-year Treasury to alter our view.

Drop In The 2-Year Yield Provides The Fed Cover To Cut Later This Month. FOMC Chair Jerome Powell spoke mid-week and struck a dovish tone, in our view. The Chair noted that it may be appropriate for the Fed to end balance sheet contraction known as quantitative tightening (QT) in the coming months, a shift that would give the central bank flexibility to buy bonds should intervention be necessary and one that would also likely serve to put a cap on long-term yields. The 2-year yield is often viewed as a proxy for where the bond market believes the Fed funds rate should be, and with the 2-year closing out last week at 3.46%, the bond market is telling the FOMC that the Fed funds could be another 50- to 75- basis points below its current level in relatively short order. On the heels of the credit issues outlined by J.P. Morgan, Western Alliance, and Zions last week, Fed funds futures are now fully pricing in two quarter-point rate cuts between now and year-end and now place a 3% probability on the FOMC doing even more than that. While the FOMC won’t likely have the September nonfarm payrolls report in hand by the time it meets on October 28-29, barring a sizable upside surprise/shock to CPI this week, the FOMC appears to have the necessary cover to deliver another “risk management cut” when it meets later this month.

No Signs Of A Rush To The Exits In High Yield Corporate Bonds Despite Worrisome Credit Commentary. Bankruptcies tied to auto parts company First Brands and subprime auto lender TriColor reverberated across markets early last week as investors questioned whether these events were the canary in the coalmine and cause for concern surrounding the high yield leveraged loan market broadly, or if they were just one-offs. There were few signs of stress in the corporate bond market last week as the Bloomberg U.S. Corporate High Yield index closed higher by just shy of 0.5%, hardly indicative of a rush for the exits and all out flight to safety. Even the Bloomberg U.S. Leveraged Loan index, which is made up of high yield, often syndicated floating rate loans such as those made to First Brands and TriColor, ended the week flat – this would not be the case if fixed income investors viewed these bankruptcies and underwriting lapses as just the tip of the iceberg. Notably, despite concerns surrounding credit underwriting standards of some financial institutions, the credit spread over the Treasury curve for the Bloomberg U.S. Corporate High Yield index narrowed from 301-basis points on 10/10 to 290 last Friday, evidence that equity investors appear to be more worried about widespread defaults/bankruptcies than credit investors are at the present time.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.