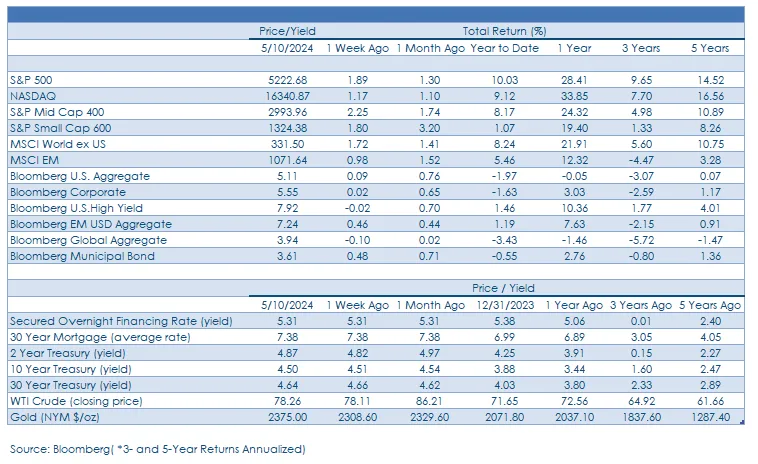

Stocks: U.S. Large Cap Stocks Reach New All-Time High; Breadth Impressive With All But One S&P 500 Sector Higher On The Week; Short Covering, Falling Treasury Yields Lead To Small Cap Surge; Emerging Markets Rally As Dollar Weakens And China Stimulus Drive Inflows.

Download Weekly Market Commentary | May 20 2024

What We’re Watching:

- Nvidia, the 3rd largest constituent within the S&P 500 and one of the drivers and beneficiaries of the rise of Artificial Intelligence, will report earnings after market close on Wednesday. The information technology sector and related areas could key off this earnings release, and a continuation of the S&P 500’s upward trend/momentum could hinge on strong Nvidia guidance.

- U.K. Consumer Price Index (CPI) for April is released Wednesday and is expected to rise at a 3.7% annualized rate, which would be a deceleration from 4.2% year over year in March. The Bank of England is expected to ease policy in June and this reading could factor into that decision.

- Minutes from the Federal Open Market Committee’s May meeting are released Wednesday.

- U.S. Purchasing Managers Index (PMI) for May is released Thursday with a Composite reading of 51.4 expected, a modest improvement from 51.3 in April. Manufacturing PMI is expected to rise to 50.3 from 50.0 in April, while Services PMI is expected to make a move to 51.5 from 51.3 the prior month. A reading above 50 indicates expansion/growth, while a reading below 50 indicates contraction.

Key Observations

- Stocks and bonds marked time leading up to the release of the April Consumer Price Index (CPI) on Wednesday, but relative calm quickly gave way to a buying frenzy with most equity and fixed income indices moving higher over the balance of the week as Treasury yields fell.

- U.S. large cap stocks made a new all-time high mid-week before trading sideways into the weekend, digesting gains and building up energy for the next advance. Smaller capitalization stocks rallied as in-line inflation data put downward pressure on Treasury yields, and investors looking for relative value and areas to play catch-up could increasingly look to this cohort in the coming weeks/months.

- Emerging markets were the big winner on the week as the U.S. dollar weakened and China’s government stepped up support for the housing sector. Hopes for additional stimulus down the road in China, combined with the prospect of U.S. dollar weakness persisting, are reasons to remain constructive on both stocks and bonds tied to emerging markets.

What Happened Last Week:

Stocks: U.S. Large Cap Stocks Reach New All-Time High; Breadth Impressive With All But One S&P 500 Sector Higher On The Week; Short Covering, Falling Treasury Yields Lead To Small Cap Surge; Emerging Markets Rally As Dollar Weakens And China Stimulus Drive Inflows.

A New All-Time High For The S&P 500 IS Hardly Bearish, But Some Consolidation, Digestion Would Be Healthy. The S&P 500 made a new all-time closing high last Wednesday, ending the day at 5,308 as the April CPI release boosted hopes for rate cuts and an economic soft landing. It is likely, in our view, that equities move higher still over the coming months as new highs tend to draw capital into stocks as investors fear missing the rally and additional gains. With that said, we would not be surprised if the S&P 500 moves sideways to modestly lower over the near-term, digesting gains through time, but a potential re-test of the 5,250 level that had been a previous ceiling of resistance shouldn’t be ruled out along the way. Headwinds from higher Treasury yields and reduced liquidity have reversed course to some degree in recent weeks, leaving us incrementally more positive on stocks, broadly speaking, into the summer.

S&P 500 Breadth A Feather In The Cap Of Bulls. While the S&P 500 making a new all-time high last week is far from a bearish event when taken at face value, it was the broad- based participation and the mix of sectors leading the way that is even more encouraging. Ten of the eleven S&P 500 sectors ended the week with gains, with industrials the only sector in the red, and information technology led the way with a 3% weekly gain, followed by real estate, health care, and financial services, each of which turned out a return of 1.5% or more on the week. What is most notable about last week’s leadership is how impressive it is to see secular growth (information technology), bond proxies (real estate, utilities), defensives (health care), and economically sensitive cyclicals (financial services) all rallying in unison. We would have liked to see consumer discretionary, and industrials participate in the rally, but all in all we can’t quibble too much with last week’s price action. It’s encouraging to see that over 70% of S&P 500 constituents now trade above their 10- day moving average, while just shy of 80% trade above their 200-day, further evidence of broad-based strength on both a short and longer-term time frame which puts the index on firm footing going into the summer.

Heavily Shorted Stocks Spike As Meme Stock Mania Returns. “Meme stocks” were back in the headlines last week as high short-interest names surged early in the week amid a flurry of short covering before profit taking took hold, with many impacted names experiencing a round- trip, closing at the prior week’s prices or below. GameStop, a video game retailer at the center of the meme craze in 2021, rose 74% and 179% in the first two days of trading last week before declining over the back half of the week and ending the week higher by 27% The video game retailer was not the only stock prone to wild intra-week swings as heavily shorted names like AMC, Petco, and Plug Power, among others, also experienced fits and starts, but due to their small position size within mid-cap indices these names had only a marginal impact on return. Notably, AMC and GameStop took advantage of the rapid run up in their share prices by issuing stock to raise capital at higher prices, diluting those partaking in the meme stock rally. This trading environment is certainly not a hallmark of a conventional market environment, but it does serve to shakeout shorts in the near-term and may even push short sellers to rethink making bets against stocks until the dust settles. The uptick in speculation is a bit unnerving but appears limited in scope for now, far from the levels seen in the post-COVID runup.

U.S. Dollar Weakness, China Stimulus Boosts Emerging Markets. he MSCI Emerging Markets (EM) index turned out a 2.7% weekly return with U.S. dollar weakness and China’s government stepping up support for the country’s distressed property market driving gains. Strength across developing markets was broad-based with country indices tied to China, India, and Taiwan each rising 2.8% or more on the week, but it was China that garnered headlines into the weekend. The MSCI China index rallied another 4% on the week as the Chinese government announced a series of measures it would take to stabilize the country’s beleaguered housing market, an announcement that has been rumored for weeks and has contributed to a 19%+ one-month gain out of the MSCI China index. The MSCI EM’s rally puts the index narrowly behind the MSCI EAFE developed markets index year to date on a total return basis, with both benchmarks returning north of 9%.

Technology stocks continue to lead the charge as the largest weight in the MSCI EM index with Alibaba, Taiwan Semiconductor, and Tencent all contributing to last week’s gains. Real estate companies in China were another contributor to return as the government eased mortgage rules and encouraged local governments to buy back unsold homes from developers with $42B of funds provided by the People’s Bank of China (PBoC) that lifted securities in the space. The clear sense of urgency and commitment we’re seeing out of officials in China is extending the runway for equities that still appear under-owned with most trading at a discount to both future earnings and current cash flows.

Bonds: Treasury Yields Fall Sharply As Inflation Data Allows Investors To Breathe A Sigh Of Relief; Emerging Market Debt Outperforms As U.S. Dollar Weakness Improves The Fundamental Outlook, Drives Inflows.

April Consumer Price Index (CPI) Spurs Treasury Rally As Odds Of A September Rate Cut Rise. There was minimal movement in bond yields leading up to the release of the April Consumer Price Index (CPI) on Monday, but Treasury bonds caught a bid and rallied on the heels of the release. Headline CPI rose 0.3% month over month, below the 0.4% estimate, and year over year rose 3.4%, in-line with the consensus estimate and below the 3.5% reading from March. Policymakers pay more attention to Core CPI which rose 0.3% month over month, in-line with the consensus estimate and 0.1% below the March reading. Year over year, core CPI rose 3.6%, a deceleration from 3.8% in the prior month. After the April PPI release on Tuesday, market participants speculated that CPI could come in cooler than expected, so we were a bit surprised at the size of the move lower in Treasury yields on the heels of the release.

The 10-year U.S. Treasury yield fell 9 basis points on Wednesday to close at 4.36% as Fed funds futures shifted and placed a 60% probability on a rate cut in September, up from 50% the day prior to the April CPI release. For the 10-year yield, 4.35% is a level we have highlighted as a potential floor of support that could cap any rally in long-term Treasury bonds. Last week’s move down to that level and failure to close below it reinforces its importance, in our view. The CPI release last week shouldn’t alter the path forward for monetary policy as the FOMC won’t have the required confidence that inflation is moving toward its 2% target in a sustainable manner to cut the funds rate in June or July, in our view, which leaves September as the most likely meeting for a rate cut to materialize. With this backdrop in place, the 10- year yield should find staunch resistance in the 4.30%/4.35% area on the downside leading up to the FOMC’s mid-June meeting, and we still see a ceiling of support at 4.70%/4.75% on the upside.

April PPI Less Hot Than The Headline Reading Would Suggest. Last Tuesday, the April Producer Price Index (PPI) was released, and the headline reading came in at 0.5% month over month versus the 0.3% consensus estimate, while core PPI, which excludes food and energy, also rose 0.5% month over month, topping the 0.2% consensus estimate. Under the surface, the details of the release were less worrisome for the inflation outlook and the prior month’s reading was revised sharply lower from 0.2% growth to a drop of 0.1%. The April PPI reading initially put upward pressure on Treasury yields, but after digesting the details market participants concluded that the CPI release to follow on Wednesday might be cooler than expected, and Treasury yields fell with the 10-year yield ending the day 3 basis points lower at 4.45%.

A Good Week For Emerging Market Bonds As Weaker U.S. Dollar Improves The Fundamental Outlook. Emerging market bonds have dealt with macroeconomic headwinds at every turn in 2024 but that backdrop is shifting as U.S. inflation and bond yields drift lower, albeit at varying paces. Bonds issued by developing economies topped other fixed income sub-asset classes we track last week, evidenced by the Bloomberg Emerging Market USD Aggregate Index returning 0.7% on its way to a 1.9% year-to-date return. The dollar’s path lower over the balance of last week was fueled by Wednesday’s in-line CPI reading which was accompanied by a move lower in Treasury yields which led local currency bonds to outpace the USD-denominated bonds we favor. We still prefer U.S. dollar-denominated EM debt as these bonds offer superior risk, or volatility- adjusted return potential, even if they lack the upside of the local currency debt should the U.S. dollar weaken materially from here.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.