Stocks: Positive Trade Headlines Buoy U.S. Equity Indices; U.S./U.K. Come To Terms On A Trade Deal In Principle, But Heavy Lifting Lies Ahead; The S&P 500 Ends The Week In Technical ‘No Man’s Land;’ U.S. Dollar Perking Up A Constructive Development; Markets Abroad Remain A Country Selection Story.

Download Weekly Market Commentary | May 12 2025

What We’re Watching:

- The National Federation of Independent Business (NFIB) releases its Small Business Optimism Survey from April on Tuesday. The reading is expected to fall to 94.7 from 97.4 in March, potentially providing further evidence that confidence on the part of smaller businesses continued to wane due in large part to tariff uncertainty.

- The Consumer Price Index (CPI) for April is slated for release Tuesday. Headline CPI is expected to rise 0.3% month over month and 2.4% year over year, compared to readings of -0.1% and 2.4% in March. Core CPI, which excludes volatile food and energy prices, is expected to rise 0.3% month over month and 2.8% year over year versus readings of 0.1% and 2.8% in March.

- The preliminary read on the University of Michigan’s Consumer Sentiment Index for May comes on Friday with the consensus estimate calling for a modest improvement to 53.0 from 52.2 in April. This ‘soft’ data point is worth monitoring for potential signs sentiment is stabilizing, particularly the inflation expectations component, which could signal concerns surrounding the potential impact on prices stemming from tariffs has peaked.

Key Observations

- Constructive trade headlines led to fits and starts but failed to push U.S. stocks higher last week as the rally stalled. Market participants appeared eager to sell into strength as the S&P 500 approached technical resistance at its 200-day moving average on the heels of an agreement in principle between the U.S. and U.K. on a trade deal. Whether or not forthcoming trade deals turn into ‘sell the news’ events will be well worth watching.

- Rumors that the U.S. and China would meet to discuss trade ‘asks’ were initially shrugged off as much ado about nothing, and even amid signs that both sides wanted to deescalate, market participants remained skeptical that any deal or ‘thaw’ in trade relations would materialize in the near-term. With earnings season 85% complete and the Fed less likely to cut the funds rate in June, the near- term path for stocks into the summer will likely be dictated by trade talks and the underlying details of deals as they are announced.

- Encouraging auction results and the FOMC remaining firmly in ‘wait and see’ mode initially put downward pressure on Treasury yields early in the week, but the details of the U.S./U.K. deal brought sellers in and forced yields higher into the weekend. Riskier, higher yielding corporate bonds outperformed their higher quality investment-grade counterparts on the week as the move higher in Treasury yields weighed on bonds with greater sensitivity to rates.

What Happened Last Week:

Stocks: Positive Trade Headlines Buoy U.S. Equity Indices; U.S./U.K. Come To Terms On A Trade Deal In Principle, But Heavy Lifting Lies Ahead; The S&P 500 Ends The Week In Technical ‘No Man’s Land;’ U.S. Dollar Perking Up A Constructive Development; Markets Abroad Remain A Country Selection Story.

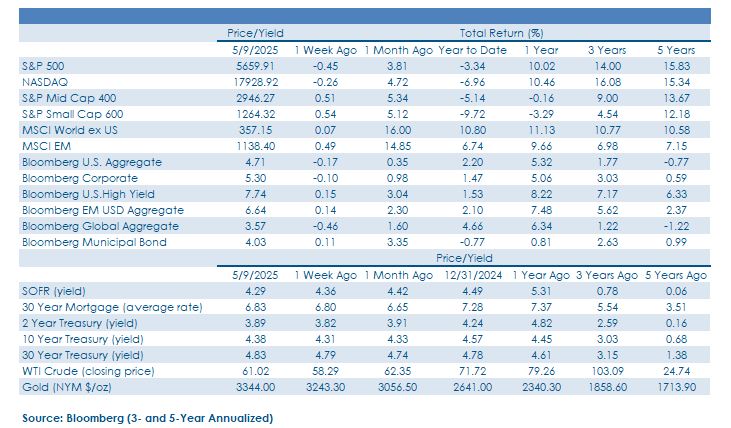

U.S./U.K. Trade Deal Boosts Animal Spirits, But The ‘Heavy Lifting’ Still Lies Ahead. Global stocks appeared to largely dismiss positive tariff headlines early last week as rumors the U.S. and China would meet in short order to discuss trade ‘asks’ made the rounds. News broke Wednesday afternoon that President Trump would not lower tariffs on imported Chinese goods in advance of the talks, which put downward pressure on stocks, albeit only briefly as headlines broke later that day that the President was removing semiconductor export curbs held over from the Biden administration. The removal of export curbs on AI-related semiconductors could be viewed as a non-tariff olive branch to China in advance of talks taking place. The two sides met this past weekend and said all the right things, i.e. that progress had been made, but there is no quick fix here, despite what the rally in stocks last week might indicate. A deal in principle with the U.K. was cheered by investors, and while we don’t want to dismiss its importance, this deal was the ‘lowest of low hanging fruit’ and subsequent deals are going to be harder to come by. Australia, India, Japan, and South Korea, among others, appear to be next up on the deal docket, and the market’s response to the details of any deals that materialize will be telling as these could be ‘sell the news’ events.

Technical Levels Worth Watching To Gauge Where The S&P 500 May Be Headed Next. The S&P 500 finds itself in no man’s land above its 50-day moving average around 5,555 and its 200-day moving average just below 5,750. Encouragingly, the index is now back above where it was trading in the lead-up to the April 2 “Liberation Day” tariff announcement, and after bottoming on April 7 has gained more than 16% since. A period of sideways price action or consolidation would be welcome after the S&P 500’s steep drop and equally impressive rebound, particularly with a broad swath of names now approaching overbought territory. Market ‘chop’ is a reasonable base case this month as the fortunes for U.S. indices become more beholden to details, not just optimistic headlines, surrounding trade deals.

U.S. Dollar Begins To Buy Into, Confirm The Bounce In Stocks. The U.S. Dollar Index, or DXY, moved sharply higher last Thursday and rose alongside U.S. Treasury yields on the news that the U.S. and U.K. had agreed to terms on a trade deal. The DXY closed the week at 100.33, just below 100.50, a level that acted as support for the index since last August/September. We view this as an area where the greenback could encounter resistance on any rally attempt, but a move above 100.50 could bring 102.0 into play. It’s notable that both the U.S. dollar and the S&P 500 closed out the week at the high-end of recent trading ranges and sit just below resistance levels, so we’ll be watching for signs of continuation of upside momentum in both in the coming weeks. A reversal of the recent uptrend is something we are watching closely should tariff/trade-related headlines turn less constructive.

Markets Abroad Close Little Changed, Remain A Country Selection Story. Both the MSCI EAFE developed markets index and the MSCI Emerging Markets index closed out the week lower by 0.1% and 0.2%, respectively. Within developed markets, Germany and Italy were standout performers, while Japan closed unchanged. The United Kingdom, perhaps surprisingly given the announced U.S./U.K. trade deal, closed lower by 0.8% on the week. Emerging markets, broadly speaking, held up well considering the rally in the U.S. dollar over the balance of the week. Strength out of Latin America continued with country indices tied to Brazil and Mexico ending the week with gains of 1.8% and 2.8%, respectively. In Asia, Taiwan was the big winner while China and South Korea closed little changed. India was a notable laggard as tensions flared with Pakistan, likely delaying the announcement of a trade deal between India and the U.S.

Bonds: Treasury Auctions, ‘Wait And See’ FOMC Initially Buoy Treasury Prices, But Yields Close Higher As Trade Deals Come Into Focus; Rate Cut Expectations Shift With The FOMC Less Likely To Cut Prior To The End Of July; Services Remained Strong In April, But Prices Pose Problems For The Fed.

Treasury Auctions Put Downward Pressure On Yields, With The Fed An Active Participant. Last week was a busy one for Treasury issuance with 3-, 10-, and 30-year tenors on the wall. On balance, demand was solid and served to put modest downward pressure on yields. Most notably, Tuesday the U.S. Treasury auctioned off $42B of 10-year notes with dealers taking down just 8.9% of the issue, the 3rd lowest percentage on record. On Thursday, $25B of 30-year bonds were auctioned off, and this issue wasn’t as well received by the market, but that could partially be a function of the upward pressure on global sovereign yields that materialized after the announcement of a U.S./U.K. trade deal earlier that same day. Some of the details underlying these auctions made headlines as the Fed was an active participant, buying $20B of Monday’s 3-year auction, $14.8b of the 10-year issue, and $8.8B of the 30-year for its own account. Some headlines misrepresented this buying as ‘shadow quantitative easing (QE),’ but these purchases were made in a ‘balance sheet neutral’ manner and were only to replace securities that matured and rolled off the Fed’s balance sheet during the month.

Market Participants Push Out Rate Cut Expectations As The FOMC Sees The Cost Of Doing Nothing As “Fairly Low.” The Federal Open Market Committee (FOMC) concluded its two-day meeting on Wednesday and as expected kept the Fed funds rate unchanged in a range of 4.25% to 4.50%. In the FOMC’s statement it noted that, “the risks of higher unemployment, higher inflation have risen,” in acknowledgement that stagflation is an increasingly likely outcome in the Committee’s eyes. Chair Jerome Powell, in his post-meeting press conference, remarked that the cost of doing nothing for the FOMC appears to be “fairly low”, and he noted numerous times that monetary policy is in a good place to respond as needed to incoming economic data. Fed funds futures were pricing in just a 17% chance of a quarter-point rate cut in June, around a 53% chance of a cut in July, and a 74% likelihood the FOMC cuts in September, all percentages fell sharply on the week.

Elevated Prices Paid For Services In April Another Problematic Datapoint For The Fed. The Institute for Supply Management (ISM) Services Index for April was released Monday and surprised to the upside at 51.6, ahead of the 50.2 estimate and the 50.8 reading from March. The Prices Paid component of the index jumped to a two-and-a-half year high at 65.1 from 60.9 in March and came in above the estimate of 61.4, while the New Orders component surprised to the upside as well coming in at 52.3, above the 50.4 March reading and the 50.3 expected. That uptick in prices paid temporarily pressured yields higher across the curve, pushing the Bloomberg Aggregate index lower by 0.1% over the course of the week. For context, a reading above 50 indicates the services sector of the U.S. economy is expanding, while a reading below 50 indicates contraction. The ‘hotter’ prices paid component is problematic for monetary policymakers as services prices have yet to show signs of cooling and acting as an offset to rising goods prices should tariffs remain in place.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.