Stocks: Domestic Indices Gain Ground On The Week But Rising Treasury Yields Has The Potential To Curb Investor Enthusiasm.

Download Weekly Market Commentary | July 31 2023

Key Observations

- Growth stocks led the charge last week as earnings out of some of the biggest names in the communication services sector powered gains. This week will loom large as Amazon, Apple, and AMD, among others, are set to report and could set the tone for the next few weeks.

- Chinese equities rallied on hopes for stepped-up stimulus measures in the country, and with investors understandably under allocated to these stocks, a late summer rally driven by offside positioning could be in the cards, potentially spurring gains for the broader MSCI EM index.

- Central bank actions drove interest rate volatility over the balance of last week, with the FOMC leaning more hawkish, the European Central Bank sounding dovish, and the Bank of Japan surprising markets by tweaking yield curve control.

- A rapid rise in U.S. Treasury yields last Thursday was unsettling for equity and currency markets, and we continue to monitor 5.05% on the 2-year yield and 4.05% on the 10-year yield for signs yields may be preparing to break higher into a new trading range.

What We’re Watching:

- Eurozone Markit Manufacturing Purchasing Managers Index (PMI) for July is released Tuesday and a 42.7 reading is expected, in-line with June. An index reading above 50 signals an increase or growth in the manufacturing sector versus the prior month, while a reading below 50 indicates a decrease or contraction.

- The U.S. Manufacturing ISM (Institute for Supply Management) report for July is released Tuesday with a 46.9 reading expected, which would be a modest improvement over the 46.0 reading in June. An index reading above 50 percent indicates that economic activity is generally expanding; below 50 percent, that it is generally declining.

- The Nonfarm Payrolls report for July is released Friday, with 200k jobs expected to have been created during the month, down from 209k in June. Average hourly earnings are expected to have risen 0.3% month over month in July, below the 0.4% reading in June.

What Happened Last Week:

Stocks: Domestic Indices Gain Ground On The Week But Rising Treasury Yields Has The Potential To Curb Investor Enthusiasm.

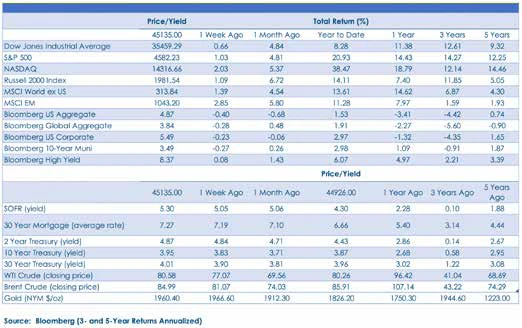

Small-Cap Summer Rolls On As A Soft Landing Becomes The Base Case. The small-cap Russell 2000 index turned out its third straight week of gains, rising 1% on the week, and is now higher by 4.9% month-to-date, outperforming the S&P 500 by 1.8% over that time frame. The Russell 2000 skews more toward cyclical sectors such as energy, financial services, industrials, and materials than does the S&P 500, which has much larger exposures to communication services and information technology. This tilt toward economically sensitive sectors was a headwind for small- caps earlier this year, but over the past month small-caps have benefited as capital has rotated out of growthier pockets of the market. Small-caps outperforming large- caps (S&P 500) is a positive indication of investor risk appetite, and this cohort of stocks does appear cheap relative to its history, but we maintain a neutral stance on small- and mid-cap (SMid) U.S. stocks as we see the risk/ reward as balanced at the present time given elevated interest rates, seasonal concerns and continued pressure on profit margins from higher labor costs.

Transports At A 52-Week High Isn’t Bearish But Pricing Power Returning Could Point Toward Inflation Reaccelerating Later This Year. Transportation stocks have performed well year-to-date, with the Dow Jones Transportation Average higher by 24.6% through last Friday. Last week brought earnings from some of the truckers and railroads, and while trailing results were, on balance, lackluster, the outlook provided by some was encouraging enough and led to a more constructive outlook than was expected. Some analysts covering these industries now appear to believe 2Q23 may have been the trough in earnings for these companies, further boosting sentiment surrounding the transports, another potential feather in the cap for market bulls. However, with demand for trucking, shipping, and railroads potentially bottoming, and pricing power possibly returning, along with oil and gas prices rising of late, inflationary pressures could reaccelerate over coming months, which may keep the Fed in play in September and beyond.

Emerging Markets Rebound As Chinese Stocks Rally On Plans For Stepped-Up Stimulus. Last week, the Chinese government announced additional policy steps it plans to take to spur consumption and drive economic growth, with a focus on adjusting policies to stabilize the beleaguered real estate market. The MSCI Emerging Market (EM) index turned out a 2.8% weekly gain, driven in large part by strength out of China as the MSCI China index rose 9%. China still faces a litany of problems over the intermediate to long-term, specifically, a 21% unemployment rate for prime working age individuals and an aging population, along with weakened consumer confidence on the heels of widespread COVID lockdowns. Despite these troubling roadblocks, fiscal stimulus and depressed valuations could increase demand for Chinese stocks over the near-term and boost the broader MSCI EM index in the process.

Commodity Rally Driven By Soft Landing Hopes, U.S. Dollar Weakness, And China Optimism. Commodity prices have risen across the board in recent weeks as expectations for an economic soft landing in the U.S., a weaker U.S. dollar, and optimism surrounding China’s economic recovery have forced speculators to cover short positions and/or get long. West Texas Intermediate (WTI) crude oil has jumped 14% in July to close at $80.48 per barrel last week, boosting the S&P 500 energy sector which has gained 5.7% over the same time frame. While precious metals such as gold and silver have participated in the commodity rally, industrial metals such as copper and nickel, along with agricultural commodities linked to geopolitical concerns such as wheat and soybeans have fared even better, boosting prospects for a broad swath of companies in the materials sector. Notably, the S&P 500 materials sector made a 52-week high last Friday, boosted by stocks tied to paper/packaging, precious metals, and chemicals, among other industries. Strength out of the materials sector, along with the industrials sector also making a 52-week high last week, provide support for the economic soft-landing narrative making the rounds.

Bonds: Developed Market Central Banks Press On With Rate Hikes; Sovereign Bond Yields Volatile As Investors Digest The Bank Of Japan’s Policy About-Face.

FOMC Hikes, Keeps Options Open For September And Beyond. The Federal Open Market Committee (FOMC) delivered a 25-basis point hike as expected last Wednesday, taking the midpoint of the Fed funds target range to 5.375%. In his post-meeting press conference, Chair Jerome Powell attempted to maintain flexibility for the Committee in upcoming meetings but did note that September could well be a “live” meeting. Chair Powell continued to champion the FOMC’s data- dependent and meeting by meeting approach, noting the Committee’s focus on inflation data between now and when the FOMC meets in September. Treasury yields initially fell and the U.S. dollar weakened after Chair Powell’s press conference as his remarks were viewed as perhaps leaning toward the dovish camp regarding future rate hikes, but after sleeping on it, market participants took his comments to be more hawkish, particularly when compared to the ECB’s stance, which forced Treasury yields higher and led to a strengthening U.S. dollar.

European Central Bank Delivers Rate Hike, Shifts To Data-Dependent Approach. The European Central Bank (ECB) met last Thursday and hiked its main policy rate by 25-basis points to 3.75%, as expected, but what wasn’t anticipated was the central bank’s newly adopted data-dependent approach. The ECB letting the data do the talking could imply a less hawkish path forward for rates in the euro area over coming months should inflationary pressures continue to subside and/or the outlook for economic growth in the Eurozone sour. While the FOMC is likely to ere on the side of tightening monetary policy too much to combat inflation, the ECB is more likely to ere on the side of doing too little to bring down inflation rather than risk over-tightening. On balance, the ECB is likely to be incrementally more dovish moving forward aiming to avoid a deep and potentially protracted economic downturn.

Bank Of Japan Surprises Markets, Tweaks Yield Curve Control Sooner Than Expected. The Bank of Japan (BoJ) met last Friday, and while the BoJ maintained its prior yield target of 0% with a +/- 0.50% range on 10-year Japanese Government Bonds (JGBs), it announced it would allow greater deviation from that range and raised the rate at which it would purchase bonds from the prior 0.50% to 1.0%. This tweak gives the BoJ some much needed flexibility to implement yield curve control and after an initial jolt higher in yields, bond and currency markets appeared to take the shift in stride. It will be interesting to see where yields on 10-year JGBs shake out over the coming weeks as, perhaps surprisingly, Japanese savers may find a yield above 0.5% too good to pass up and could step in and buy JGBs at last Friday’s close of 0.55% in short order, or they may wait patiently and see if yields rise further before doing so.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.