Stocks: More Signs Of Rotation As Value, Small-Caps Continue To Outperform U.S. Large-Caps; ‘Mag 7’ Results Rattle Markets, But Could Shift From Market Headwind To Tailwind In The Coming Week; Japanese Stocks Falter As The Yen Strengthens.

Download Weekly Market Commentary | July 29 2024

What We’re Watching:

- The Eurozone Consumer Price Index (CPI) for July is released Wednesday with headline CPI expected to rise 2.5% year over year, in-line with the June reading, while core CPI is expected to rise 2.8% year over year during the month, which would be a modest deceleration from 2.9% in the prior month.

- The Federal Open Market Committee (FOMC) concludes its two-day July meeting on Wednesday. The Committee is expected leave the Fed funds rate unchanged while leaving the door wide open for a rate cut when it meets in mid- September.

- July Nonfarm Payrolls are released Friday with 177.5k jobs expected to have been created during the month. Average hourly earnings are expected to rise 0.3% month over month and 3.7% year over year, versus 0.3% and 3.9% readings from June. The unemployment rate is expected to remain static month over month at 4.1%.

Key Observations

- Investors continued to reposition portfolios last week by pulling capital out of the information technology and communication services sectors and increasing exposure to value-oriented sectors such as financial services, health care, industrials, and materials, as well as small cap stocks for the third consecutive week.

- Expense guidance provided by Alphabet and Tesla, both members of the anointed Magnificent 7, rattled markets mid- week as investors became more concerned that spending on artificial intelligence (AI) wouldn’t be generating a return anytime soon. However, investor fears could be eased in the coming week as Amazon, Apple, Meta Platforms, and Microsoft are all set to report quarterly results, and most should be able to communicate a more upbeat story.

- Yields on short-term U.S. Treasuries fell over the balance of the week as a 2-year Treasury auction was very well received and July inflation data (PCE) met expectations, doing little to alter the case for a rate cut out of the FOMC in the coming months. When the FOMC meets this week, it will likely prepare markets for a policy shift when it comes together again in mid-September, and Fed funds futures are pricing in a 100% probability of a 25-basis point rate cut at that time.

What Happened Last Week:

Stocks: More Signs Of Rotation As Value, Small-Caps Continue To Outperform U.S. Large-Caps; ‘Mag 7’ Results Rattle Markets, But Could Shift From Market Headwind To Tailwind In The Coming Week; Japanese Stocks Falter As The Yen Strengthens.

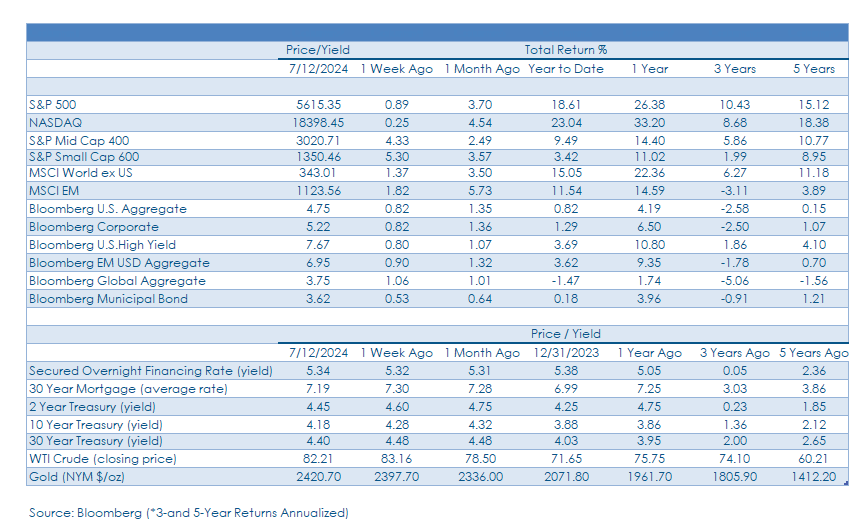

Still Reasons To Be Constructive After Another Tough Week For U.S. Large Cap Stocks. Stocks. The S&P 500 fell over the balance of last week as capital continued to rotate into value-oriented sectors and small cap stocks. While the headline S&P 500 index ended the week lower by 0.8%, the equally weighted S&P 500 rose by 0.8%, evidence that breadth remains more encouraging when looking under the surface. From a technical perspective, the S&P 500 closed below its 50-day moving average around 5,430 last Thursday, the first time since mid-April it has done so. In mid-April, the S&P 500 declined another 3% before finding a bottom and rallying, so while the S&P 500 traded back above the 50-day moving average on Friday, that potential level of support is well worth watching as a series of closes below 5,435 or thereabouts could usher in a continuation of the selloff as trend following strategies sell into weakness. As of Friday’s close, over 50% of S&P 500 and Nasdaq Composite constituents still were trading above their 10- day moving average and 2/3 of the S&P 500 still traded above their 50-day moving average, hardly evidence of a ‘sell everything and run for the hills’ mentality dominating. From a sector perspective, financial services, health care, industrials, and materials each ended the week with 1% or greater gains, while consumer staples and real estate closed with a more modest 0.5% rise. The communication services, consumer discretionary, and information technology sectors was noticeably weak, with each of the three sectors finishing the week lower by 1.5% or more. However, much of that weakness was driven by a relatively small number of names with Alphabet (communication services) and Tesla (consumer discretionary), along with the semiconductor industry (information technology) acting as significant detractors.

Expense Guidance Out Of ‘Mag 7’ Names Weighs, But Fears Could Be Eased In The Coming Week. The S&P 500 closed out the week lower by 0.8% as Alphabet (GOOG/GOOGL) and Tesla (TSLA), both members of the ‘Magnificent 7’ cohort of stocks, rattled markets mid-week. Both companies posted quarterly results that either met or exceeded expectations for sales and earnings, but both stocks sold off on higher- than-expected expense guidance tied to spending on artificial intelligence (AI) as investors are increasingly skeptical that companies can reap benefits and generate a positive near-term return on those sizable investments. Most notably, Alphabet’s CEO on the post-earnings call noted that the risk to underinvesting in AI is greater than the risk of overinvesting in the technology. Statements like this give us confidence that there will continue to be winners tied to the AI theme over the near-term, but stock picking – both within the ‘Mag 7’ and outside of that cohort of stocks, will likely matter more in the coming quarters, potentially setting up a better backdrop for active managers in the growth space to outperform their benchmark after a challenging stretch over the past year. The Microsoft, Meta Platforms, Amazon, and Apple management teams likely learned a thing or two from the Alphabet and Tesla calls and should do a better job when framing spending plans when they report this week, which could ease lingering investor concerns surrounding when capital invested into AI is going to boost returns.

Small Cap Summer’ Gets A Boost From Higher GDP Print. Last Thursday, 2nd quarter GDP was released, and at 2.8%, it doubled 1.4% GDP growth from the first quarter and came in well-above the consensus estimate calling for growth of around 2.0% for the U.S. economy. The upside surprise to quarterly growth was welcomed by investors in small cap stocks as the S&P Small Cap 600 advanced 2.3% on Thursday and ultimately 3.5% on the week, with the index now outperforming the S&P 500 for the third consecutive week. The GDP growth figure likely shouldn’t be taken at face value due to the incomplete nature of the data in the initial reading, but directionally the stars are aligning for cyclical companies farther down the market cap spectrum. From a sector standpoint, higher relative weights to healthcare and financial services did the heavy lifting with each sector outperforming the 600 by 1% or more on the week. The backdrop for small caps has improved in a short period of time and if revenue picks up as the consensus expects, momentum could continue to build, particularly as inflation fears and monetary policy uncertainty subside.

Yen Rally Weighing Heavily On Japanese Stocks. Shares of Japan-based exporters have come under pressure in recent weeks from a stronger yen and fears of waning demand for tech and tech-related products produced in the country. Japan’s Nikkei 225 Index fell 3.7% last week in U.S. dollar terms as the Japanese yen strengthened from 157.5¥ to $1 to 153.7¥ as yields on Japanese Government Bonds rose further and expectations built that the Bank of Japan (BoJ) might have to raise rates soon. Macro traders and trend followers took profits or outright closed longstanding short positions in the Japanese yen as the currency broke through its 100-day moving average at 155¥ to one U.S. dollar. Attention now turns toward the BoJ meeting this Wednesday with expectations that bond purchases will slow further after the odds of a rate hike rose to 68% from 42% at the start of last week. The BoJ will likely raise rates while downplaying expectations for two or more hikes over the balance of this year, which should serve to limit further strength in the yen and allow Japanese stocks to catch their breath after the recent slide.

Bonds: Economic Data Provides A Tailwind For Lower Quality Bonds; FOMC Set To Meet This Week And Lay The Groundwork For A September Rate Cut.

GDP, Inflation Data Provide A Boost For Shorter-Term And Lower Quality Bonds. Core Personal Consumer Expenditure (PCE), the FOMC’s preferred inflation measure, rose by 2.5% year-over-year in July, in-line with the consensus estimate and furthering the case for a cut to the Fed funds rate in the coming months. While the lower PCE reading didn’t exactly meet the consensus forecast of 2.4%, it was still received well by stock and bond investors and the Bloomberg Aggregate Bond index finished the week with a modest 0.2% gain. Riskier, higher yielding corporate bonds and emerging market debt also gained ground last week as recent U.S. economic data has removed some of the final hurdles to less restrictive monetary policy. The Bloomberg High Yield Index gained 0.3% and the Bloomberg Emerging Markets Bond index rose 0.2% on the week. Improvement to inflation and the recent upside surprise in GDP growth for Q2 leave the case for riskier fixed income in good standing as higher yields continue to attract capital especially as yields on cash appear poised to drift lower over the next 6-12 months.

FOMC Unlikely To Move This Week, But Should Pave The Way For A September Cut. On the heels of last week’s PCE release, the Federal Open Market Committee (FOMC) concludes its regularly scheduled two-day meeting on Wednesday. The Committee is expected to leave the Fed funds rate unchanged while leaving the door ajar for a rate cut in September. Fed funds futures place the likelihood of a rate cut this week at just 4.5% but view a cut in September as a slam dunk, with a 109% probability, implying there is some chance that any September cut will be greater than 25-basis points. Given the FOMC’s desire to avoid surprising markets, we suspect the Committee will telegraph that a rate cut is increasingly likely in September, while also restating that any shift in policy remains dependent upon upcoming inflation prints continuing to cool and moving in a sustainable fashion toward the FOMC’s 2% target.

2-Year Treasury Auction Results Point To Strong Demand For Short-Term Government Debt. The U.S. Treasury auctioned off $69B of 2-year notes last Tuesday and the issue was well received with especially strong demand out of foreign central banks which took down 76% of the issue vs. the ten-auction average of 63%. Demand from direct bidders (pension plans, insurance cos.) was a bit weaker at 14% vs. 21% average, but the dealer community only received 9% of the issue, well below the 16% average. Short-term U.S. Treasury yields fell throughout the balance of the week and the 2-year yield closed at 4.36%, down from 4.50%, and with the 10-year closing at 4.20%, down 5 basis points on the week, the yield spread between the two bonds closed at its lowest level since January. The narrowing spread between 2s and 10s leaves the Treasury market on the cusp of an upward sloping yield curve after one of the longest inversions on record. Historically, a dis-inversion of the yield curve is an ominous signal that could bring near-term volatility to both the stock and bond markets but with a resilient U.S. economy and the FOMC likely to begin easing monetary policy in the coming months, we don’t believe it has the same predictive power as it has historically.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.