Stocks: Good, Not Great Earnings Spurs Profit-Taking In Year-To-Date Winners, With Capital Rotating Into Underperforming Defensive Sectors; Emerging Markets Lag As The Dollar Strengthens.

Download Weekly Market Commentary | July 17 2023

What We’re Watching:

- The Conference Board’s July Consumer Confidence Survey is released Tuesday and is expected to rise to 110.5 from 109.7 in June.

- The Federal Open Market Committee (FOMC) concludes its two-day policy meeting on Wednesday. Fed funds futures are pricing in a 97% likelihood of a 25-basis point rate hike at this week’s meeting which would take the midpoint of the target range for Fed funds to 5.375%.

- The European Central Bank (ECB) meets on Thursday and is expected to raise key interest rates by 25-basis points. With some ECB ‘hawks’ sounding more dovish of late as the Eurozone economy has slowed, President Lagarde’s post-meeting remarks regarding potential moves at upcoming meetings may prove meaningful for the near-term direction of asset prices.

- Preliminary second quarter U.S. GDP is released Thursday with growth of 1.5% quarter over quarter and 2.0% year over year expected.

- June U.S. Personal Consumption Expenditure (PCE) Deflator, the FOMC’s preferred inflation gauge, is released Friday. Headline PCE is expected to rise 0.2% month over month and 3.0% year over year, while core PCE is expected to rise 0.2% month over month and 4.1% year over year. The FOMC will be closely watching the magnitude of the downshift in core PCE.

What Happened Last Week:

Equity

- Communication services and consumer discretionary, two of this year’s biggest winners, were last week’s biggest laggards as earnings releases failed to justify lofty valuations. Mega-cap information technology names slated to report quarterly results over the coming weeks could dictate whether stocks surge or experience a summer swoon.

- Capital rotated into some of this year’s underperforming sectors such as consumer staples, energy, health care, and even utilities, likely driven by investors seeking out a defensive posture leading into one of the weaker seasonal periods of the year for stocks from late July through September.

Stocks: Good, Not Great Earnings Spurs Profit-Taking In Year-To-Date Winners, With Capital Rotating Into Underperforming Defensive Sectors; Emerging Markets Lag As The Dollar Strengthens.

Was Last Week’s Sell Off In Some Of This Year’s Winners A One-Off, Or The Start Of A Growth-To-Value Rotation?

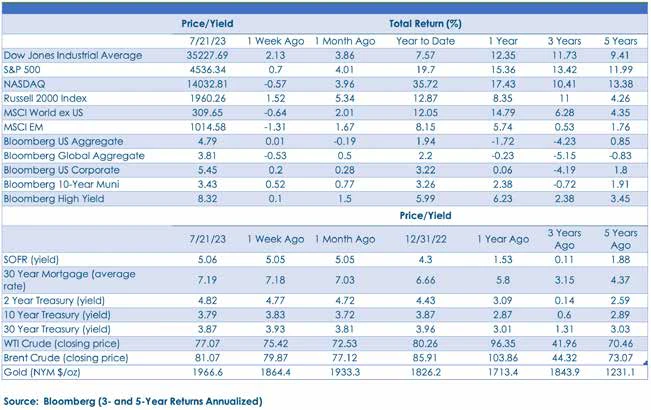

Tesla, after a 136% year-to-date rally through last Wednesday, is a member of the “Magnificent 7” club of stocks that has driven an outsized portion of the S&P 500’s gain, while Netflix had posted a more than respectable 62% year-to-date through last Wednesday leading up to its earnings release. With Netflix trading at 41 times projected next twelve months’ earnings, and Tesla a loftier 86 times after rallying sharply in May and June, it would have taken blowout earnings and shockingly strong guidance for these stocks to rally post-earnings last Wednesday. With great expectations comes the potential for great disappointment and Netflix lost 8.4% and Tesla traded down by 9.7% on Thursday as investors viewed quarterly results as good, but not good enough to support valuations. The S&P 500 did a good job of shrugging off weakness out of Netflix, Tesla, and some of the other “Magnificent 7” members over the balance of last week as it eked out a 0.7% weekly gain. Valuations could become a bigger focus for investors over coming months spurring sector rotation and potentially leading to volatility and weakness in the broader S&P 500 due to communication services, consumer discretionary, and information technology accounting for just shy of 50% of the index. Investors taking profits in this year’s winners and rotating capital into small-cap stocks and value-oriented sectors such as energy, financial services, health care, and materials, among others, would be encouraging and another sign the broader market is on stronger footing.

The Path Forward For The U.S. Dollar Looms Large For EM. The MSCI Emerging Markets (EM) index fell 1.3%, last week as it was pulled lower by weakness out of China, South Korea, and Taiwan, along with a strengthening of the U.S. Dollar. The U.S. Dollar Index, or DXY, had been mired in a downtrend since the end of May, with the DXY falling from 104.33 on 5/31 down to an intra-day low of 99.58 on July 13 – a sizable and notable move in a short period of time. However, after making a 16-month low on 7/13, the DXY has reversed course and rose 1.1% just last week, due in large part to inflation data out of the U.K. and euro area cooling month over month in June. Should the downshift in inflationary pressures abroad persist, the Bank of England (BoE) and European Central Bank (ECB) may be able to back away from additional rate hikes, which would have implications for the DXY given that the euro and British pound sterling make up 70% of that foreign currency basket. Both international developed and emerging market stocks have historically been negatively correlated with the U.S. dollar, meaning that as the dollar weakens these stocks tend to appreciate as many of these countries import crude oil and industrial metals, which are often priced in U.S. dollars. While we have no edge in calling the near-term direction of the U.S. dollar, or any other currency for that matter, the DXY may remain range-bound near-term between 100 and 102 as central banks meet over the coming weeks and the path forward for monetary policy becomes clearer. A break above 102 would be notable, and present a hurdle for stocks, while a move below the July 13 low of 99.58 would also be noteworthy and would likely provide a substantial tailwind for international developed and emerging market stocks, while also likely leading to concerns of inflation reaccelerating in the U.S. in the back-half of 2023.

Fixed Income

- Last week was a relatively quiet one in fixed income markets as the Bloomberg Aggregate Bond index ended the week flat, while corporate bonds eked out modest gains.

- The Federal Open Market Committee (FOMC), Bank of Japan (BoJ) and European Central Bank (ECB) all meet this week, and investors will be closely monitoring and dissecting comments made in post-meeting press conferences to gauge the path forward for monetary policy.

Bonds: Central Banks Take Center Stage With Guidance Out Of The Federal Open Market Committee (FOMC) And European Central Bank (ECB) Potentially Market Moving.

Investment-Grade Corporate Bonds A Beneficiary Of Range- Bound Rates. Economic data last week continued to point toward a resilient U.S. economy, with initial jobless claims falling week over week and the business outlook portion of the Philadelphia Fed’s Manufacturing survey for July spurring economic optimism and pushing yields on long-term Treasuries higher last Thursday. However, the 10-year yield ended the week unchanged at 3.83%, toward the lower end of its recent trading range between 3.75% and 4.05%. Investors are weighing the prospect of inflation remaining elevated or potentially reaccelerating in the back-half of this year due to a weaker U.S. dollar and a potential step-up in China’s stimulus efforts with the potential for central banks abroad to shift in a dovish direction as disinflationary forces build, putting downward pressure on sovereign bond yields in the U.K. and euro area. Interest rate volatility continuing to wane would boost the relative appeal of longer duration investment-grade corporate bonds, specifically, and we remain constructive on corporate credit, broadly, over the near-term.

Some ECB ‘Hawks’ Starting To Sound Dovish. The European Central Bank (ECB) meets this week and is widely expected to hike key interest rates by another 25-basis points. There was support for a 50-basis point hike at the ECB’s June meeting, but only a quarter-point hike was implemented. In the wake of its June meeting, the ECB strongly hinted at another 25-basis points in July, so it’s likely that the central bank follows through with a quarter-point. However, with economic growth slowing in the euro area and disinflationary forces building over the past three months, it’s possible that a July hike may be the last, as even some of the most vocal and ‘hawkish’ of ECB policymakers appear to be waning in their conviction surrounding the need for additional policy tightening.

U.K. Inflation Cools In June, But Will That Alter The Bank Of England’s Course Of Action? U.K. Consumer Price Index (CPI) for June was released last Wednesday with headline CPI rising 0.1% month over month, shy of the 0.3% estimate, and 7.9% year over year, a significant downshift from 8.7% in May. Core CPI rose 6.9% year over year, which was below the 7.0% consensus estimate and 7.1% reading from May but well above target for the Bank of England (BoE). The BoE has been talking tough on inflation and even after June’s cool CPI is still expected to hike key policy rates further when its Monetary Policy Committee meets August 3. However, with inflationary pressures subsiding while remaining far too high for comfort, market participants are questioning how aggressive the BoE will ultimately be, which led to a sharp move lower in yields on U.K. gilts and weakness in the British pound over the balance of last week.

Rising Core Inflation In Japan Keeping The Bank Of Japan On Guard. Japan’s Consumer Price Index (CPI) ticked higher in June, with the headline reading rising to 3.3% year over year from 3.2% in May. Core CPI rose 3.3% year over year, also up from 3.2% the prior month. The Japanese yen fell sharply over the balance of last week and has fallen 8% versus the greenback year-to-date, a trend that has been supportive of Japan’s export-reliant economy and Japanese equities. The Bank of Japan meets this week, and with inflation running hot the pressure on the BoJ to alter its yield curve control program is building. While we don’t expect action or an announcement this week, we expect the BoJ will raise the allowable cap on the 10-year Japanese Government Bond (JGB) yield at some point in the coming quarters, which should lead to a modest strengthening in the yen, and weakness in JGB’s and Japanese stocks.

The content and any portion of this newsletter is for personal use only and may not be reprinted, sold or redistributed without the written consent of Regions Bank. Regions, the Regions logo and other Regions marks are trademarks of Regions Bank. The names and marks of other companies or their services or products may be the trademarks of their owners and are used only to identify such companies or their services or products and not to indicate endorsement or sponsorship of Regions or its services or products. The information and material contained herein is provided solely for general information purposes.

Regions does not make any warranty or representation relating to the accuracy, completeness or timeliness of any information contained in the newsletter and shall not be liable for any damages of any kind relating to such information nor as to the legal, regulatory, financial or tax implications of the matters referred herein. This material is not intended to be investment advice nor is this information intended as an offer or solicitation for the purchase or sale of any security or other financial instrument. Any opinions expressed herein are given in good faith, are subject to change without notice, and are only current as of the stated date of their issue. Regions Asset Management is a business group within Regions Bank that provides investment management services to customers of Regions Bank. Employees of Regions Asset Management may have positions in securities or their derivatives that may be mentioned in this report or in their personal accounts. Additionally, affiliated companies may hold positions in the mentioned companies in their portfolios or strategies. The companies mentioned specifically are sample companies, noted for illustrative purposes only.

The mention of the companies should not be construed as a recommendation to buy, hold or sell positions in your investment portfolio. Neither Regions Bank nor Regions Asset Management (collectively, “Regions”) are registered municipal advisors nor provide advice to municipal entities or obligated persons with respect to municipal financial products or the issuance of municipal securities (including regarding the structure, timing, terms and similar matters concerning municipal financial products or municipal securities issuances) or engage in the solicitation of municipal entities or obligated persons for such services.

With respect to this presentation and any other information, materials or communications provided by Regions, (a) Regions is not recommending an action to any municipal entity or obligated person, (b) Regions is not acting as an advisor to any municipal entity or obligated person and does not owe a fiduciary duty pursuant to Section 15 B of the Securities Exchange Act of 1934 to any municipal entity or obligated person with respect to such presentation, information, materials or communications, (c) Regions is acting for its own interests, and (d) you should discuss this presentation and any such other information, materials or communications with any and all internal and external advisors and experts that you deem appropriate before acting on this presentation or any such other information, materials or communications. Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

The information provided herein is for informational purposes only and is intended to report on various investment views held by Multi-Asset Solutions (MAS) and Highland Associates. Opinions, estimates, forecasts, and statements of financial market trends are based on current market conditions that constitute the judgement of MAS and Highland Associates and are subject to change. The information is received from third parties, which is believed to be accurate, but no representation is made that the information provided is accurate and complete. The information is given as of the date indicated and believed to be reliable. While MAS and Highland have tried to provide accurate and timely information, there may be inadvertent technical or factual inaccuracies or typographical errors for which we apologize. The information provided herein does not constitute a solicitation or offer by Highland or its affiliates, to buy or sell any securities or other financial instrument, or to provide investment advice or service. Nothing contained herein should be construed as investment advice or a recommendation to purchase or sell a particular security. Investing involves a high degree of risk, and all investors should carefully consider their investment objective and the suitability of any investments.

Research services are provided through Multi-Asset Solutions, a department of the Regions Asset Management business group within Regions Bank. Highland is a wholly owned subsidiary of Regions Bank, which in turn is a wholly owned subsidiary of Regions Financial Corporation.

Past performance is not indicative of future results. Investments are subject to loss.