Stocks: Trade Policy Shift Promoting Upside In Chipmakers And Chinese Equities; Bank Earnings And Domestic Retail Sales Signaling Healthy Consumer.

Download Weekly Market Commentary | July 21 2025

What We’re Watching:

- Alphabet and Tesla report earnings on Wednesday, the first of the Magnificent 7 stocks to report in, with onlookers watching to see if the former can continue their streak of beating street estimates and the latter turns around after consecutive misses in the two quarters prior.

- S&P US Manufacturing and US Services PMI data is due out on Thursday with consensus forecasting the services number to improve to 53.0 from 52.9 and a manufacturing step back to 52.5 from 52.9. Both are expected to stay above 50, signaling expansion.

- Initial Jobless Claims are reported on Thursday with consensus expecting an increase to 227K from 221K, after a consistent decline since the start of June. It is worth noting that without seasonal adjustments, initial claims have moved higher in each of the prior three weeks.

Key Observations

- Domestic technology and emerging market equities excelled last week, as the U.S. administration shifted its stance to allow select chip exports to China, opening the door to further improvement around trade between the world’s largest economies.

- Treasury yields experienced upward pressure from a hotter CPI reading on Tuesday before settling near where they started the week after uncertainty around the FOMC was dispelled and Fed Governor Waller reiterated the case for rate cuts.

- The changing factors influencing CPI and above consensus retail sales data along with strong bank earnings reaffirmed sentiment around consumer health and the direction of U.S. growth, even if inflation remains a going concern.

What Happened Last Week:

Stocks: Trade Policy Shift Promoting Upside In Chipmakers And Chinese Equities; Bank Earnings And Domestic Retail Sales Signaling Healthy Consumer.

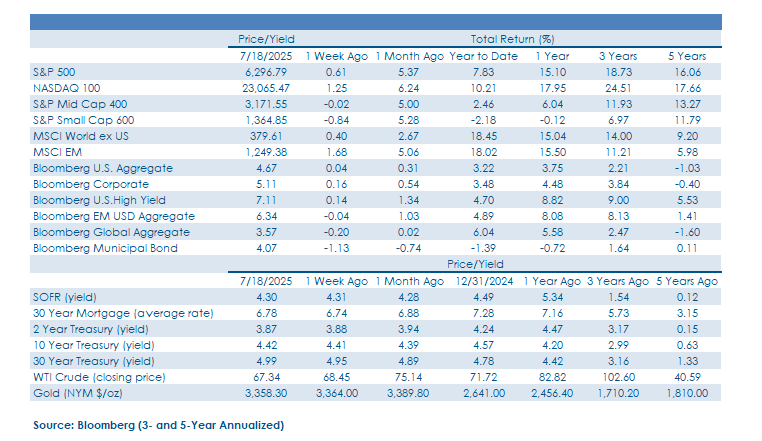

Turnaround In Chip Trading To China A Tailwind For Big Tech. Domestic technology stocks started the week on a high note as Nvidia CEO Jenson Huang announced the company would restart sales of select chips to China, with confirmation Advanced Micro Devices could also resume sales later in the week. The approval of these sales out of Washington marks another turning point for the administration, that is now focused on building international reliance on U.S. tech, instead of trying to block Chinese advancements. Shares of Nvidia were up over 4.5% last week alone on the news and the broader NASDAQ 100 advanced by 1.3%. Outside of chipmakers, Netflix was another positive driver in the NASDAQ as the streaming company bested earnings estimates and provided upbeat forward guidance that pushed the stock higher by 1.9% on the release.

Emerging Stocks Benefit From Bullish Trade Sentiment And Semiconductor Earnings. The softer stance on American chip exports was taken as a starting point for further improvement in the trade relationship between Washington and Beijing, leading the MSCI China index to rally 3.7% on the week. The success in semiconductor names wasn’t limited strictly to U.S. companies as Taiwan Semiconductor beat on earnings and provided above consensus sales guidance for next quarter. Tailwinds from the largest country and company in the MSCI Emerging Equity index pushed the broader benchmark higher by 1.7% over the course of the week. That gain is especially impressive as the dollar strengthened in the background, a signal the emerging equity story is less reliant on the greenback, while the developed MSCI EAFE index on the other hand declined by 0.3% last week.

Retail Sales And Bank Earnings Bode Well For Cautious Consumers. Outside of technology, financials were another stand out performer last week as earnings from top lenders including JPMorgan, Bank of America, and Citigroup all bested street estimates. Taking a broader view on the industry, 12 of the 13 banks in the S&P 500 index reported last week, with all but one bank surpassing earnings expectations. Most company executives gave encouraging perspectives on the consumer, with noted softening at the lower income levels but improved trading and investment banking revenues were strong drivers for the largest banks. Retail sales numbers last Thursday echoed the upbeat sentiment around the consumer as the headline number grew 0.6% month over month, well in advance of the 0.1% consensus forecast, with the retail sales control group and sales ex auto also outrunning the average estimate. As is often the case, there are seasonal adjustment impacts to consider in the retail sales numbers and temper our view on the consumer, but at the end of the day household financial conditions appear solid.

Bonds: Interest Rates Tick Higher Due To Inflation Before Backtracking On Dovish Fed Speak; International Treasury Demand Disputing Trade War Stories, And Noise Around Firing The Fed Chair Caused A Lull In Credit.

Fixed Income Markets Flatten Out As CPI Is Offset By Fed Speakers. Core bond benchmarks narrowly avoided a third consecutive weekly decline after headline CPI surprised to the upside on Tuesday, rising to 2.7% from 2.4% in the month prior. Base effects played a role in the higher headline number, as the Core CPI number matched consensus at 2.9%, but fixed income markets took concern with the report details as inflation shifted from services to goods. The two offset each other in June, but the concern is that we’re just starting to see tariff impact on inflation and that companies may pass through those added costs over the coming months to dull the sticker shock. Inflationary concerns pushed the 10-year yield to top out at 4.48% before sliding back to close the week just above its 50-day moving average at 4.42%. The decline in rates over the back half of the week came as the President reassured markets that he has no plans to fire Fed Chairman Powell and Fed Governor Waller delivered his case for a July rate cut.

Treasury Data Shows Foreign Buyers Still Interested In US Bonds. The May TIC data released on Thursday poked holes in the narrative that foreign countries are striking back on United States tariffs through bond market activity. In May foreign buyers took in $146B of treasuries, the most since August of 2022 according to data compiled by JPMorgan. Canada and the U.K. were the largest net buyers, with the former purchasing $65.8B, more than offsetting net sales in April of $57.7B despite ongoing trade tensions. Japan and China were also among the top purchasers of U.S. government bonds, pushing back on the de-dollarization narrative. To us the issue with using treasuries as a weapon remains that it likely causes the currency of the selling country to strengthen, a troubling impact for export-driven economies like Japan and China.

High Yield Credit Spreads Settled Lower After Midweek Markup. Volatile trading was a consistent theme across government bonds and corporate credit as below investment grade valuations shifted higher by 6bps to the high for the week at 288bps on noise that the President was again looking to fire Fed Chair Powell. The dispelling of that rumor by the White House led the Bloomberg Corporate High Yield index to be one of the better performing fixed income segments, gaining 0.1% on the week with valuations receding to 281bps. Better economic readings in retail sales were another feather in the cap of credit investors that had a part in CCC-rated bonds making their sixth straight weekly gain. From our vantage point, credit markets are indicating recent strength in risk assets can persist even with mild setbacks along the way.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.