Stocks: Bulls Push The S&P 500 Above 5,600 And Defend That Level In The Lead Up To Earnings Season; Rotation Evident As Cyclicals, Small Caps Rally As Information Technology Sells Off; Developed, Emerging Markets Abroad Outperform.

Download Weekly Market Commentary | July 15 2024

What We’re Watching:

- Quarterly earnings season ramps up in a big way with 40-plus S&P constituents scheduled to report.

- The European Central Bank’s (ECB) Governing Council meets on Thursday and is expected to leave rates unchanged after cutting key policy rates by 25-basis points when it met in June. Post-meeting remarks from ECB President Lagarde could provide some insights into how the central bank expects to proceed in the coming months/quarters given the outlook for inflation and economic growth in the euro area.

- The Conference Board will release its index of U.S. Leading Economic Indicators (LEIs) for June on Thursday, and is expected to fall 0.30% month over month, which could be a modest improvement versus the -0.50% reading in May.

Key Observations

- Economically and interest rate sensitive stocks, as well as small caps, took the leadership baton from communication services and information technology stocks. Earnings season and the path forward for interest rates could go a long way in deciding whether this change in leadership proves durable or is little more than a head fake.

- Small cap stocks benefitted from falling Treasury yields and offsides positioning which forced investors to cover shorts, or bets on falling share prices, but both tailwinds could prove short lived. Small cap indices skew more heavily toward economically sensitive stocks, which could come under pressure should economic growth fears remain or build in the coming months.

- Treasury yields fell and bond prices rose as tame inflation data for June boosted the prospect of rate cuts when the FOMC meets in September. With inflationary fears subsiding and economic growth concerns moving to the forefront, long dated Treasuries continue to hold appeal as a diversification tool within multi-asset portfolios, despite lower yields after the recent rally.

What Happened Last Week:

Stocks: Bulls Push The S&P 500 Above 5,600 And Defend That Level In The Lead Up To Earnings Season; Rotation Evident As Cyclicals, Small Caps Rally As Information Technology Sells Off; Developed, Emerging Markets Abroad Outperform.

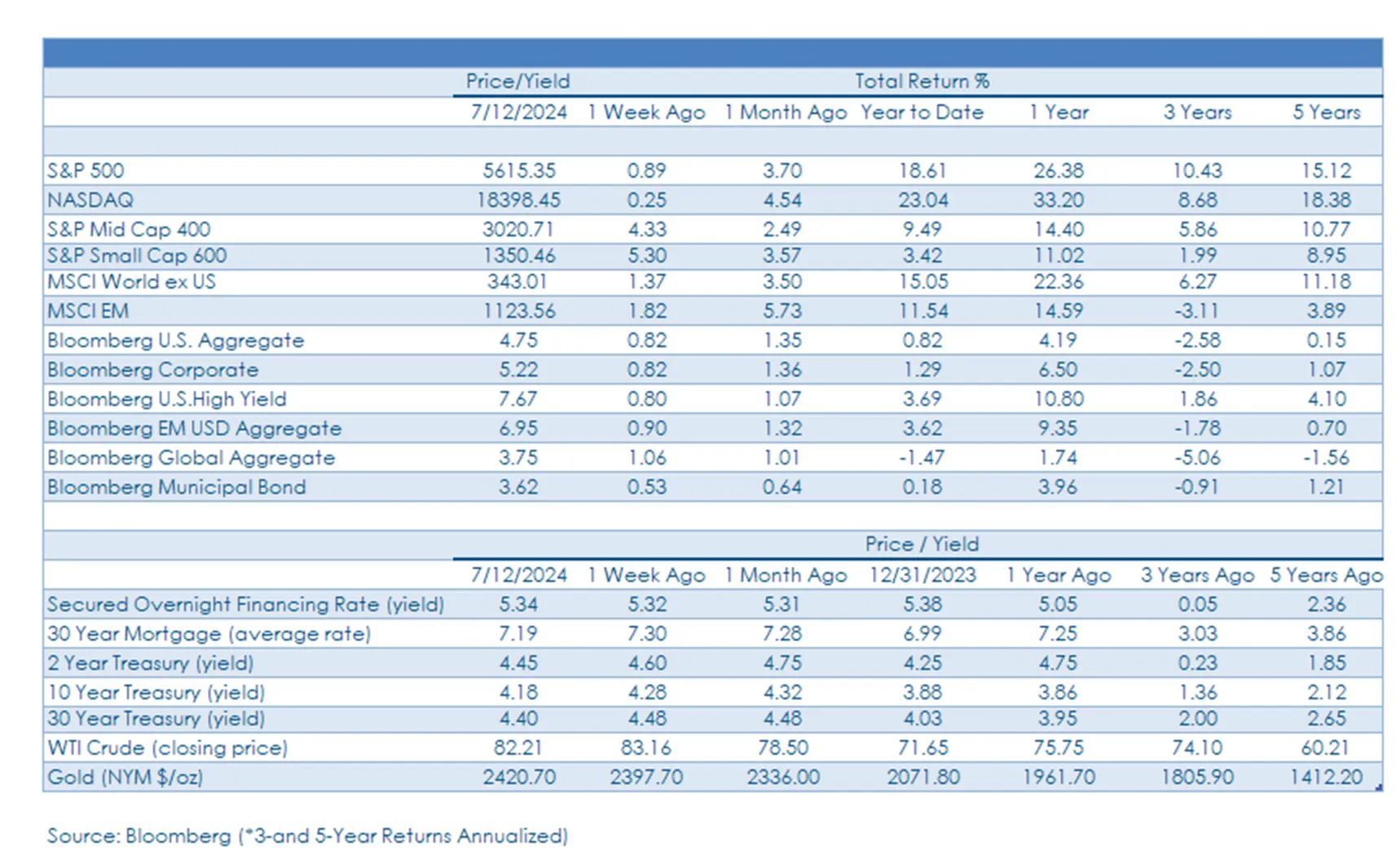

Rotation Favors Interest Rate, Economically Sensitive Sectors. Interest rate sensitive and cyclical sectors led the S&P 500 charge last week with financial services, health care, industrials, materials, real estate, and utilities each rallying 2% or more, outperforming the broader S&P 500’s 0.9% weekly gain. While the information technology sector lagged the broader index, it still returned 0.4% on the week, so even amid a bout of significant sector rotation, investors didn’t want to stray too far from the biggest and most well capitalized companies. Communication services appeared to be a better source of funds for investors as the sector fell 1.6% on the week but is still 0.7% higher month-to- date. Sector rotation was obvious on Thursday, but breadth was better on Friday, an encouraging development should it persist, particularly if economically sensitive areas can continue to rally without the Magnificent 7 selling off in a meaningful way.

Earnings Season Outlook. Last week was the unofficial start of quarterly reporting season as three of the largest U.S.-based banks, Citigroup, J.P. Morgan, and Wells Fargo, posted results and in the coming week more banks and capital markets-focused companies, along with bellwether names in the health care and industrials sectors, among others, slated to report. From a top-down view, the S&P 500 is expected to grow earnings by 8% from the 2nd quarter of 2023 to $62.71 this quarter. From a bottoms-up perspective, projecting individual company earnings, year over year earnings growth is expected to be a bit better than that and come in at 9%. The communication services, health care, information technology, and utilities sectors are all expected to grow earnings by more than 10% year over year, while the materials sector is expected to see earnings fall by 7.5%, and the consumer staples, industrials, and real estate sectors are each expected to grow earnings by 3% or less year over year.

Small Caps Surge On Tame CPI, Short Covering. Cooler June inflation data put downward pressure on Treasury yields and led to a meaningful repositioning across equity sub-asset classes last week, contributing in a major way to the 3.2% rally in the S&P 600 small-cap index last Thursday. The S&P 600 ultimately rallied 5.3% on the week as sector rotation boosted value-centric areas including financial services and real estate, among others. Financials, specifically, were a standout performer as the sector within the S&P 600 registered a 7.1% weekly gain, easily outpacing the S&P 500 financial services sector’s 2% return, and the sector accounts for a substantial 18.5% weight within the S&P 600, versus just 11.9% in the S&P 500. It’s worth noting that all S&P 600 sectors finished with positive performance on the week, with breadth improving as the percentage of stocks trading above their 200-day moving average jumped to 65% from 52% at the start of the week. Short covering was a big driver of last week’s rally in small cap stocks, and isn’t a sustainable driver of returns, but we would welcome continued breadth improvement in small cap indices which could indicate the move is more than an oversold bounce or trade.

Euro Area Stocks Rebound As Political Risk Subsides. After After experiencing a rough stretch throughout June due to rising political risk across the currency bloc, euro area stocks rebounded last week, with the Stoxx Europe 600 index rallying 1.4% in euro terms and an even better 2.2% when hedged back to the U.S. dollar. Breadth was encouraging with country indices tied to Germany, Italy, and Spain all turning out 1.5% or greater gains, while France, and the U.K. FTSE 100, while not included in the euro bloc, returned more modest 0.6% gains on the week. With closely watched elections in France and the U.K. now in the rearview mirror and with the status quo upheld, limiting the prospect of sweeping changes to agendas and policies, investors could turn their attention toward the potential for economic growth to improve across Europe in the coming quarters, which could generate additional inflows into euro area and U.K. stocks.

China, Taiwan Push Emerging Markets Indices Higher. The MSCI EM index turned out a 1.8% weekly gain, a continuation of the trend from last month but with better regional participation. The turnaround in Mexico’s equity market is a development worth noting with the MSCI Mexico index registering an 8.2% weekly advance as oversold conditions following last month’s election finally garnered investor attention. In the Far East, country indices tied to Taiwan and China each ended the week higher by 2% or more. China placed further restrictions on securities lending, effectively curbing short-selling and bets against the nation’s equities. Taiwan Semiconductor, by far the largest stock in the MSCI Taiwan index with a weighting of 25%, continues to attract investors due to its relative value advantage versus other popular AI stocks as it trades closer to 27 forward earnings while peers Nvidia and Broadcom trade at 30 and 44 times, respectively.

Bonds: Treasuries Well-Bid On Tame June CPI, But Near-Term Downside For Yields Likely Limited From Here; 10-Year Treasury Auction Attracts Buyers With Deep Pockets; A September Rate Cut Remains Our Base Case, But Isn’t A Slam Dunk.

Strong Auction Results, Tame CPI Put Downward Pressure On Long-Term Treasury Yields. Treasury yields remained anchored leading up to the release of the Consumer Price Index (CPI) for June last Thursday, but yields fell sharply across the curve as inflationary pressures appeared to ease more than expected last month. Yields on Treasury bonds maturing 6-months and farther out in future all experienced 5- to 12- basis point drops on the day, but the largest downward moves occurred in the 2- to 3-year portion of the yield curve. It is noteworthy, in our view, that the 10-year Treasury yield hit 4.15% intra-day last Thursday but failed to break below that level and bounced to end the day at 4.20%. From a technical perspective, the 4.15%/4.20% zone remains a key tell as the last time the 10-year yield closed below the upper bound of that range was in mid-March, and a break below the lower bound could point toward economic growth concerns dominating. Given our view that U.S. economic growth should still come in around 2% for the full year, and that the path down to 2% inflation is likely to be a slow and bumpy ride, we see little room for additional downside in long-term Treasury yields and believe risks are skewed to the upside with the next 25-basis point move likely higher, not lower, in our view.

Treasury Auctions Well Received. The U.S. Treasury floated a mix of short- and long-term debt last week, a useful pulse check on preferences for duration exposure out of investors with deeper pockets. Auction participation for 10-year notes mid-week piqued our interest as direct bidders, a category primarily made up of domestic pension plans and insurance companies, reached 20.9%, a feat last seen in October of last year. Subsequently, dealers took down just 11.5% relative to the 16% they had to stomach on average in the prior ten auctions. That trend continued in the 30-year auction on Thursday as direct bidders were awarded 23.4% of the issue, the highest mark in nearly a decade according to Bloomberg. Last week’s auctions were far from perfect as traditional metrics of demand including bid-to-cover ratios which act as a gauge of buyer interest, were the lowest since November. From our perspective, bid-to-cover ratios could improve as expectations around CPI improvement and how it translates to easing monetary policy renew institutional interest, but fiscal concerns are likely to keep a lid on demand and limit just how far yields on long-term Treasuries can fall over the short to intermediate-term.

June Consumer Price Index (CPI) Boosts Case For September Rate Cut. Consumer Price Index (CPI) for June was released last Thursday with the headline reading posting a drop of 0.1%, versus expectations of a 0.1% month over month rise. This is the first negative month over month CPI print since May of 2020. Year over year, headline CPI came in at 3.0%, below the 3.1% estimate and the 3.3% reading from May. Core CPI rose 0.1% month over month in June, below the 0.2% consensus estimate and the prior month’s reading, and year over year core rose 3.3%, modestly below the 3.4% consensus estimate. On the heels of the CPI release, market participants became more convicted in their belief that the Federal Open Market Committee (FOMC) would cut the Fed funds rate in September as Fed funds futures shifted to price in an 90% chance of a quarter-point cut at that meeting, up from a 73% likelihood the day before the CPI release.

Emerging Market Bonds Benefit From Lower U.S. Rates, Outperform U.S. Corporates. Emerging market bonds were one of the best performing fixed income sub-asset classes last week as the benchmark J.P. Morgan Emerging Market Bond Index (EMBI) was higher by 0.9%, outpacing U.S. investment grade and high yield corporate bond indices on the week. The lower June CPI reading and the subsequent decline in interest rates allowed emerging market debt, which tends to carry a slightly longer duration profile than core bonds, to capitalize on the upside move. The impact of macroeconomic forces was obvious when looking at the underlying country data as only 2 of 55 countries represented in the index, El Salvador and Sri Lanka, had negative returns last week.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.