Stocks: Tech Rally Sends Nasdaq Near Record Amid Dovish Fed Hints; Foreign Equities Falter On Tariff Fears As Asian Equities Lead, Import Levies Take Copper Prices To All-Time High.

Download Weekly Market Commentary | July 14 2025

What We’re Watching:

- Headline and Core Consumer Price Inflation (CPI) readings for June are released on Tuesday with consensus forecast calling for a 2.6% and 2.9% year over year advance, respectively. Both inflation gauges are expected to be higher than in the prior month, with market participants watching for any signs of tariff-related inflation.

- Producer Price Inflation (PPI) is due out on Wednesday with an expected decline to 2.7% from 3.0% in the prior month. A reading above the estimate could translate to upward pressure on the FOMC’s favored core PCE measure of inflation.

- The Retail Sales report is anticipated on Thursday with a survey expectation of 0.1% growth in the month over month headline number, after seeing a 0.9% decline in May.

Key Observations

- A flurry of tariff announcements out of the U.S. administration cast a shadow that pushed global equity markets lower on the week, leading stocks tied emerging economies to lag domestic indices with securities in Latin America seeing the largest decline.

- 10-Year treasury rates moved higher for the second consecutive week, as new country and sector tariff announcements fueled fears that trade policy could pressure inflation higher even as the FOMC minutes suggested effects could be temporary.

- The dollar strengthened as market participants were forced to contend with the idea that the U.S. economy and labor market may be more durable than anticipated, as tariffs aren’t impacting growth concerns to the degree they were in April.

What Happened Last Week:

Stocks: Tech Rally Sends Nasdaq Near Record Amid Dovish Fed Hints; Foreign Equities Falter On Tariff Fears As Asian Equities Lead, Import Levies Take Copper Prices To All-Time High.

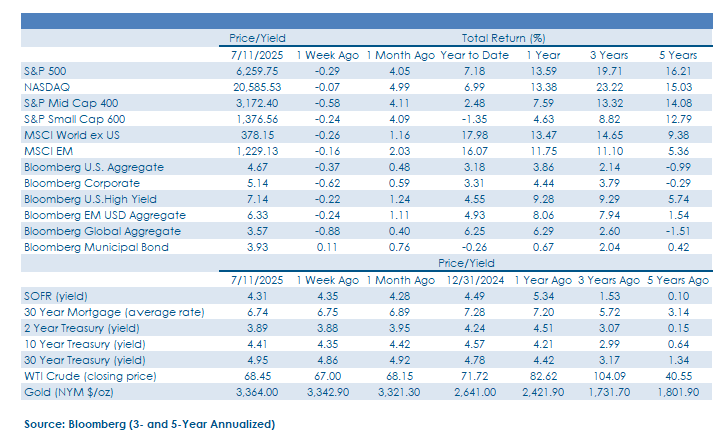

Tariff Escalation Sparks Early Week Sell-Off, Returns Flattened Into The Weekend. Equity markets stumbled to start the week after President Trump announced sweeping 25% tariffs on Japanese and South Korean imports, set to take effect August 1. Though the largest import levies of the week fell on Brazil and Canada, with tariffs of 50% and 35%, respectively. Canadian import taxes were mostly ignored by markets, as they exclude USMCA compliant goods, but the MSCI Brazil index shed 6.1% of its value last week. The S&P 500 and NASDAQ 100 each fell between 0.7% and 0.8% on Monday as investors grappled with the renewed threat of global trade fragmentation, but by the end of the week the indices were down 0.3% and 0.1% respectively. There were bright spots in select U.S. stocks, with Nvidia advancing 3.6% after briefly reaching a $4 trillion market capitalization, while mega-cap peers Amazon, Microsoft, and Alphabet also posted solid gains.

South Korea Outperforms Despite Trade Risks, Equities In Latin America Not So Lucky. While trade tensions weighed on international markets, emerging equities took the worst of the downturn with the MSCI Emerging Equity index declining by 0.9%, while the developed market MSCI EAFE index fell by 0.4%. Tariff announcements on Japanese and Korean imports, brought the former down by 3.0% with the latter negative by just 0.1%. The market reaction comes across broadly instructive as Japan’s manufacturing economy and modest political will to deal with the United States cast doubt on how a deal will play out. South Korea’s KOSPI rose more than 4% during the week, briefly hitting 3,200 during intraday trading Friday and notching a four-year high. Investors appeared to be betting on a favorable outcome to US trade negotiations ahead of the August tariff deadline. Domestic sentiment was also boosted by sweeping regulatory reforms unveiled by Korean financial authorities, including new penalties for insider trading and tighter listing standards. After drawing the ire of the administration and ensuring 50% tariff, the Brazilian equity market was one of the worst performers on the week. The U.S. holds a slight trade surplus with Brazil, similar to the United Kingdom, making meaningful concessions hard to come by.

Commodities Mixed as Supply and Trade Dynamics Shift. U.S. copper prices posted an all-time high during Tuesday’s trading session after President Trump indicated Washington would impose a 50% tariff on copper imports in an effort to boost domestic production of the critical metal. As a result, the iShares Copper and Metal Mining ETF experienced volatile trading on the week, ultimately falling by 1.7%. Crude oil prices were broadly unchanged midweek, with WTI down 0.1% to $68.28 per barrel after modest gains earlier supported by a tighter physical market and an OPEC+ production increase above expectations. The near-term outlook remains volatile as global demand prospects remain linked to the evolving tariff landscape. In precious metals, gold rose slightly by 0.6% to $3,364.00 per ounce while silver rose by 5.1% to $36.58 largely on trade concerns. The muted move in gold suggests investor positioning remains balanced between safe-haven demand and confidence in a soft landing supported by Fed accommodation.

Bonds: Payrolls Surprise And Tariffs Pressing Yields And Inflation Concerns Higher; Corporate Bonds Backtrack As Market Teases Out Dovish Tilt In FOMC Meeting Recap.

Fixed Income Trading Lower On Increasing Inflation Potential. Bond market benchmarks endured negative price action in each of the last two weeks as market participants are faced with the potential reality that the economy and labor market may be more durable than feared. One catalyst for this shift was the upside surprise in payrolls on the Thursday before the July 4th holiday weekend that pushed yields higher. To us, that number was fraught with seasonal adjustment noise and boasted a lackluster initial response rate but nonetheless comes as the second consecutive above consensus estimate reading. The fading concern in growth has investor attention tilting towards inflation, as new country tariffs crop up and sectoral tariffs wait in the wings. That rising angst around inflation was apparent in 2-year treasury break-evens, that have risen 20bps since the start of July and yields on 10-year nominal bonds that have also ticked higher with the 10-year closing the week at 4.40%. Improving sentiment around economic growth could be a tailwind for the U.S. dollar, which has risen alongside rates and appreciated to $97.08 since the start of July.

FOMC Meeting Minutes Depict Divided Policy Stance. The June FOMC meeting minutes released last Wednesday further detailed the growing rift between Chairman Powell and select committee members on how accommodative the central bank should be given the current risks facing the economy. Those differing views broadly still accepted the committee’s ability to wait as the labor market remains resilient, but the release led the futures market to increase the odds of a rate cut in September from 64% to 68% on Wednesday. However, the uptick in trade rhetoric upended those projections as higher country tariffs and the potential for elevated sectoral tariffs reignited inflationary concerns.

Demand For Corporate Debt Slowing At The Margin. Corporate bond buyers took a step back last week as valuations widened in both the investment grade and high yield indices. The Bloomberg Investment Grade Corporate index was down 88bps as yields on the long end of the curve moved higher, adding insult to injury, valuations widened to 80bps over comparable treasury securities. The downturn could have been worse with the treasury auctioning 10- and 30-year papers later in the week, but the drought in issuance made the new bonds highly sought after. In the short term, we could see buyers interested in replenishing their long bond exposures, but should inflationary pressures start to build, demand could fade as more supply comes to market.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.