Stocks: Headline Indices End The Week Lower As Tariff Talk Ramps Up, With Rotation Evident Under The Surface; Response To ‘Magnificent 7’ Earnings Mostly Positive; The Search For ‘Value’ Driving Flows In Emerging Markets To Start The Year.

Download Weekly Market Commentary | February 3 2025

What We’re Watching:

- The Institute for Supply Management (ISM) Services Index for January is released on Wednesday and is expected to come in at 54.1, in-line with the December reading. Above 50 is indicative of growth in the services sector of the U.S. economy, while below 50 indicates contraction.

- The University of Michigan is set to release its monthly Consumer Sentiment Index for February on Friday.

- The January Nonfarm Payrolls report is released Friday with the consensus estimate calling for 170k jobs to have been created during the month versus 256k in December. The unemployment rate is expected to be unchanged month over month at 4.1% with average hourly earnings expected to rise 0.3% month over month and 3.8% year over year.

Key Observations

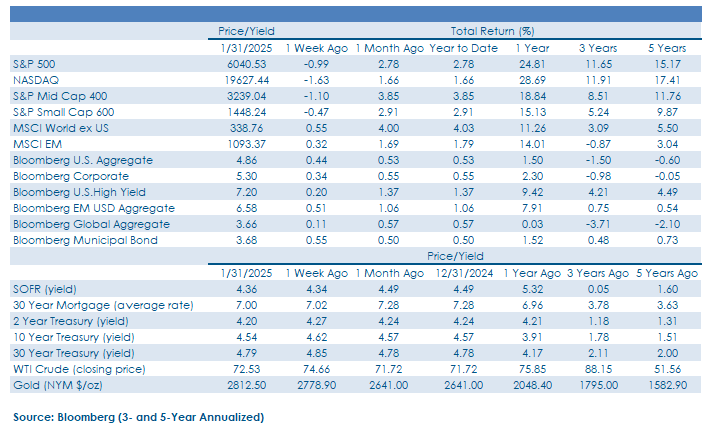

- U.S. stock indices closed lower on the week as talk of tariffs being implemented over the weekend on goods imported from Canada, China, and Mexico forced investors to the sidelines. Capital appeared to rotate out of technology stocks tied to the buildout of artificial intelligence infrastructure early in the week but found its way into communication services, consumer staples, financial services, and health care, among others, leading to improved market breadth.

- Foreign stocks fared a bit better on the week with developed market indices buoyed by strength out of Europe and emerging market indices receiving a tailwind from exposure to China and India, offsetting weakness out of South Korea and Taiwan.

- U.S. Treasury yields ended the week lower as the prospect of broader and faster artificial intelligence (AI) adoption spurred disinflationary calls, and the FOMC delivered a ‘hawkish pause’ mid-week which put additional downward pressure on rates. The 4.50% level for the 10- year U.S. Treasury yield remains well worth watching for stock and bond investors alike as a break below could bring the 4.25%/4.30% range into play in short order, potentially driving upside in longer duration information technology stocks and riskier bonds along the way.

What Happened Last Week:

Stocks: Headline Indices End The Week Lower As Tariff Talk Ramps Up, With Rotation Evident Under The Surface; Response To ‘Magnificent 7’ Earnings Mostly Positive; The Search For ‘Value’ Driving Flows In Emerging Markets To Start The Year.

Rotation The Name Of The Game As Headline Indices End The Week Lower. The financial services and health care sectors were two of the most obvious beneficiaries as capital rotated out of hardware and utility stocks tied to the buildout of AI infrastructure last Monday, with the former rising 1.1% and the latter jumping 2.2% on the day as the information technology sector pulled back by 4.9%. Financials gained 1.2% on the week while health care did a bit better, rising 1.7%. Information technology recouped some of its early week losses to end the week lower by 3.5%. Communication services and consumer discretionary stocks also had a good week, turning out gains of 1.9% and 0.9%, respectively, as Amazon and Meta Platforms delivered. Notably, while semiconductors and other hardware names associated with AI in the information technology sector were sources of funds early last week, software stocks expected to cheaply and quickly leverage AI technology were beneficiaries, highlighting ongoing rotation both between sectors and within sectors throughout the balance of the week.

Market’s Response To ‘Mag 7’ Earnings Encouraging. Four of the anointed ‘Magnificent 7’ posted quarterly results last week. Meta Platforms (Facebook), Microsoft, and Tesla kicked things off for the group as each reported after the market close Wednesday. Investors rewarded Meta with a higher share price as the company continued to highlight benefits from its investment in artificial intelligence (AI), one of the few such companies able to do so, while reaffirming capital expenditure guidance of $60-$65B this year on AI initiatives. Tesla also traded higher Thursday despite falling short of the consensus estimate for earnings and sales in the trailing quarter as investors chose to latch on to enthusiasm surrounding a broader launch of self-driving or autonomous cars in the coming years as Tesla noted it would begin testing robotaxis in additional markets within the next two quarters, pulling forward the expected launch timeline in the eyes of investors. Microsoft was the lone name of the three reporting Wednesday to selloff after its release as growth in the company’s cloud computing platform, Azure, fell a touch below the street’s forecast. Microsoft was by far the weakest performer out of the Magnificent 7 names last year, but last week’s selloff highlights how lofty expectations continue to be for some of these names, making them susceptible to pullbacks should results fail to wow investors. Apple rounded out the week by reporting after the bell Thursday and shares initially rose Friday as revenue guidance and the outlook for iPhone sales in China weren’t as dire as market participants feared, but the stock ultimately ended the day lower as talk of tariffs dominated. All told, Meta and Apple were the big winners on the week, rising 6.4% and 5.9%, respectively, while Tesla closed the week lower by 0.5% and Microsoft fared the worst, declining 6.5%.

AI-Driven Volatility Generates More Diverse Outcomes Within The Emerging Markets. The selloff in artificial intelligence (AI) related names early last week wasn’t limited to domestic markets as some of the largest stocks in the MSCI Emerging Market Index, specifically Samsung, SK Hynix, and Taiwan Semiconductor sold off in sympathy with Nvidia and other U.S. domiciled semiconductor names. Investors didn’t appear eager to flee emerging markets entirely, evidenced by the MSCI EM index advancing by 0.3% on the week. Strength out of Chinese equities was notable as the MSCI China index rallied 2.1% even as the country’s markets were closed for Lunar New Year and talk of the U.S. levying additional tariffs on Chinese imports made the rounds. Alibaba and some of China’s other ‘national champions’ appear to be working on their own AI models that could rival US counterparts and could spur additional capital inflows over the near-term. While not AI-related, the year-to-date rebound in some of the more embattled value-oriented pockets of the developing world such as Latin America is also worthy of attention and highlights the January effect in full swing as investors appear to be willing to increase exposures to last year’s laggards in areas that may have been unduly punished. Recent outperformance out of value-oriented exposures must persist for longer than a few weeks to convince investors it’s a trend reversal with staying power but is a step in the right direction. Markets have shown restraint when it comes to pricing in the prospect of of tariffs up to this point, but with the U.S. entering into potential tit for tat tariff battles with Canada and Mexico over the weekend, volatility in emerging market stocks is likely to remain elevated due to headline risk until common ground can be found and rhetoric is toned down.

Bonds: Treasury Yields End The Week Lower Amid FOMC’s ‘Hawkish Pause,’ AI Disinflation Hopes; Credit Spreads Shrug Off Technology Weakness; No Surprises In The January Inflation Data.

10-Year U.S. Treasury Yield Ends The Week Lower As The FOMC Delivers A ‘Hawkish Pause’ While Broader, Quicker AI Adoption Is Expected To Drive Disinflation. Hopes for a broader and faster adoption of artificial intelligence (AI) technology put downward pressure on U.S. Treasury yields early last week. A Chinese hedge fund rolled out its DeepSeek model in December, but investors failed to take notice until last week when more information was released surrounding the amount of money spent ($6 million, allegedly) to build and train the model. This dollar figure led to hopes for broader and faster adoption of the technology, as well as the prospect of reduced investment on the part of hyperscalers (Alphabet, Amazon, Meta Platforms, Microsoft, etc.) attempting to leverage AI to boost earnings growth. Fixed income investors appeared to view DeepSeek as disinflationary due to these shifting expectations. The inflation rate implied by Treasury Inflation Protected Securities (TIPS) fell across most tenors over the balance of the week and fell across the Treasury curve on all but the 1-year note, which ended the week flat. The move lower in yields on AI hopes appeared to initially be overdone, particularly given lofty guidance out of Meta Platforms and Microsoft related to spending on AI infrastructure was reaffirmed last week. The 4.50% level on the 10-year Treasury yield held yet again with that bond ending the week with a yield of 4.58% on Friday, but this remains the level worth watching as a break below could potentially bring 4.25% into play in short order. How long- dated Treasuries respond to tariff saber rattling remains to be seen but will be well worth watching in the coming week(s).

Credit Spreads Barely Flinch Despite The Early Week Tech Takedown. Amid the unsettling drop U.S. large-cap stocks early last week, high yield credit was largely unphased and the Bloomberg US High Yield Index returned 0.2% to notch its third consecutive weekly gain. Credit spreads ticked higher by 6-basis points off month-to-date lows as equity volatility ramped up early last week, but high yield valuations barely budged with higher yields more than making up for price declines. Below investment grade credit trades more in lockstep with small cap stocks as the two asset classes share similarities in sector exposure, both carrying higher exposures to cyclicals and defensives and less exposure to technology. These exposures leave the high yield index more insulated from AI-related volatility, but correlations between equities and high yield bonds will likely remain elevated as both are riskier portfolio allocations. Beyond the headline returns, CCC-rated bonds were the worst performers on the week, evidence market participants were more risk averse at the margin. CCC’s had been a relative success story this year before losing ground to B- and BB-rated credits last week, a reminder of the tail risk present and potential downside in the riskiest corporate bonds should investor risk appetite shift even modestly.

FOMC In ‘Wait And See Mode’ As Other Central Banks Ease. In a unanimous vote last Wednesday, Federal Open Market Committee members chose to leave the Fed funds rate unchanged at their first meeting of 2025 within a range of 4.25% to 4.50%. The post-meeting statement and press conference proved to be non-events for markets, with minor revisions a result of “cleaning up the language” per Chairman Powell, and the “not in a hurry” mantra we heard for much of last year was revived in his remarks to the press. A similar tone was struck when he addressed how the Committee is factoring in potential policy shifts out of Washington D.C. as Powell suggested they would be patient as policy plays out. The Bank of Canada, on the other hand, cut its key policy rate by 25-basis points to 3% and lowered guidance based on the potential threat of tariffs being levied on U.S. imports of Canadian goods. The European Central Bank (ECB) also voted to cut its deposit rate by a quarter-point to 2.75% while hinting at additional policy easing in the coming months, despite inflation rising last month for the euro-area as the ECB’s attention has shifted firmly toward spurring economic growth after GDP rose a paltry 0.1% in 4Q24 and just 0.7% year over year in 2024. The FOMC remains in an enviable position relative to many other central banks around the world after 4Q GDP rose 2.3% year over year and the Committee’s preferred inflation gauge, core PCE, rose 0.2% month over month and 2.8% year over year in January, in-line with expectations. This combination of continued strong economic growth and sticky inflation should allow the Fed to stand pat and in ‘wait and see mode’ into mid-year, and the market views June as the most likely meeting for another rate cut.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.