Stocks: The S&P 500 Remains Range Bound In Holiday Shortened Week; Earnings Season Supportive Of A Constructive Outlook On U.S. Stocks; Eurozone Breadth Positive, While Japanese Stocks Finally Cool Off After A Hot Start To The Year.

Download Weekly Market Commentary | February 23 2026

What We’re Watching:

- The Conference Board releases its February Consumer Confidence survey on Tuesday, with the reading expected to improve to 88.0 from 84.5 in January.

- Semiconductor behemoth Nvidia (NVDA) is set to post quarterly results on Wednesday, and with the $4.6 trillion company accounting for 7.6% of the S&P 500, we would expect results to prove market moving.

- The U.S. Producer Price Index (PPI) for January is released on Friday, with Final Demand PPI expected to have risen 0.3% during the month, which would be a deceleration from the 0.5% print the prior month.

Key Observations

- U.S. equity indices posted gains during the holiday-shortened week as economically sensitive sectors continued to lead across the market capitalization spectrum. Within the S&P 500, the communication services, energy, financials, and industrials sectors outperformed the broader index, while classically defensive sectors such as consumer staples and health care lagged.

- Abroad, Japanese stocks were noticeably weak, giving back a small portion of their sizable year-to-date gains as investors finally took profits. The MSCI EAFE developed markets index still gained 0.8% on the week as Japan’s weakness was more than offset by strength out of Eurozone and U.K. indices. On the emerging markets front, Brazil, South Africa, South Korea and Taiwan propelled the MSCI Emerging Markets (EM) index to an impressive weekly gain.

- U.S. Treasury yields closed the week modestly higher across the curve as economic data, U.S./Iran tensions, and the Supreme Court’s decision to strike down the bulk of U.S. tariffs currently in place served to keep both buyers and sellers on their toes. U.S. corporate high yield performed relatively well despite news out of one high profile fund sponsor in the private credit space that they would be putting up gates and limiting redemptions. This is evidence of robust risk appetite and a continued willingness by investors to reach for higher yields in lower quality bonds.

What Happened Last Week:

Stocks: The S&P 500 Remains Range Bound In Holiday Shortened Week; Earnings Season Supportive Of A Constructive Outlook On U.S. Stocks; Eurozone Breadth Positive, While Japanese Stocks Finally Cool Off After A Hot Start To The Year.

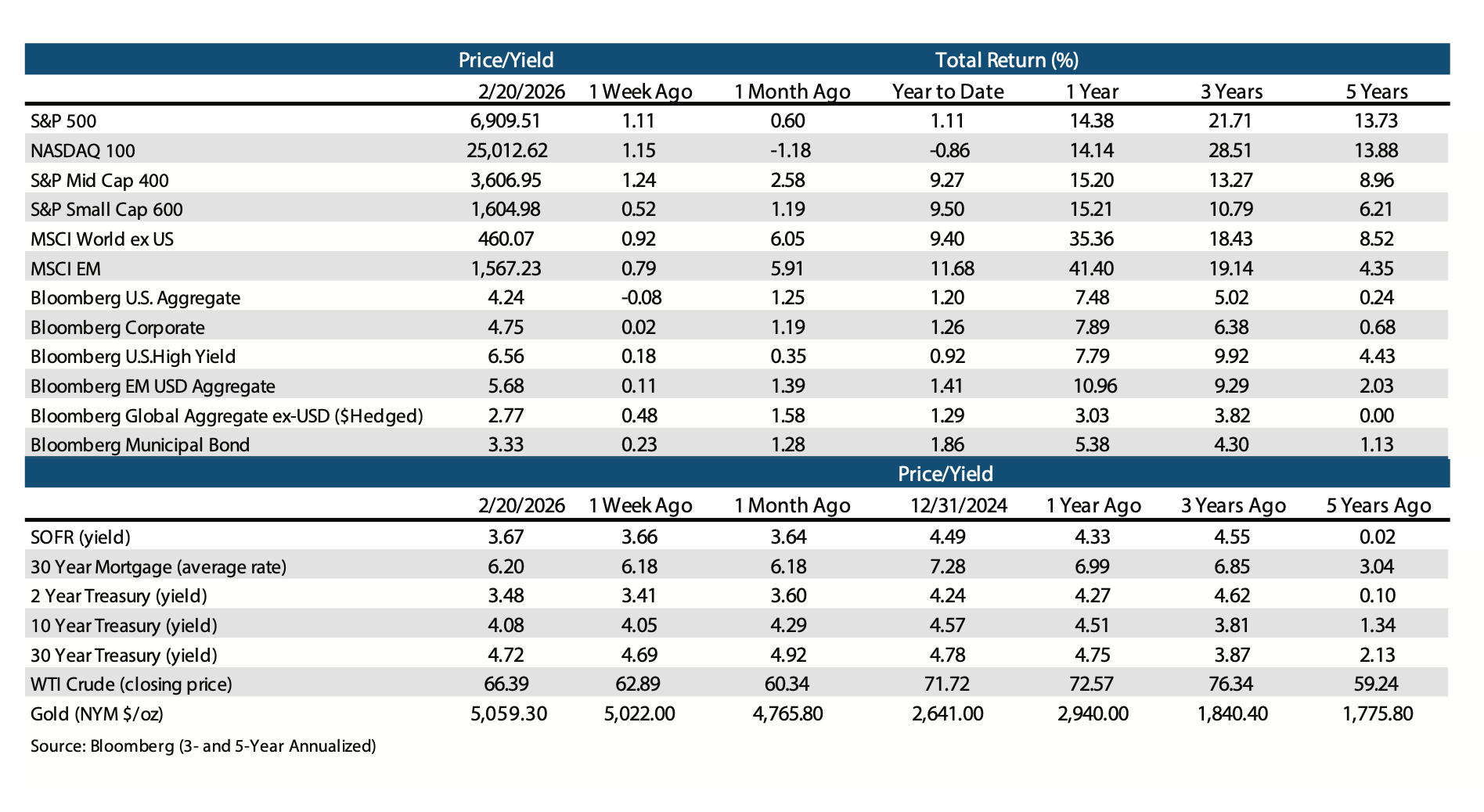

Narrow Trading Range For The S&P 500 Holds As February Lives Up To Its Billing As A Challenging Month. The S&P 500 continued to trade in a narrow range moored around the 6,900 level over the balance of last week, briefly eclipsing that mark on Wednesday before geopolitical tensions put upward pressure on commodity prices and weighed on risk appetite. The index gained 1.1% on the week but remains lower by 0.3% month-to-date. From a sector leadership perspective, energy rose again by another 1% on the week as West Texas Intermediate (WTI) crude oil rallied on escalating tensions between the U.S. and Iran as Iran moved to block part of the Strait of Hormuz, a critical shipping channel in the Middle East. The industrials sector also performed well, rising 1.7% as John Deere (DE) and GE Aerospace (GE) rallied following quarterly earnings releases. On the other side of the coin, the consumer staples sector fell 1.8%, weighed down by General Mills (GIS), Mondelez (MDLZ) and Walmart (WMT), among others, with each falling by 5% or more on the week. Notably, the information technology sector closed out the week with a 0.9% gain, a welcome sight after the software industry has had a February to forget and has acted a drag on the tech sector. While one week doesn’t make a trend, it’s encouraging that the technology sector at large and the software industry, specifically, appeared to stabilize.

Checking In On Earnings Season. 85% of the companies in the S&P 500 has reported quarterly results through last Friday, with the average company posting sales growth of 8.9% and earnings growth of 12.3%, which compares favorably to the 2.1% and 6.3% figures from 3Q25 reporting season. The average positive earnings surprise has been 7.7%, with the industrials and materials sectors stand-out performers, posting average upside surprises to the consensus earnings estimate of 23.5% and 20%, respectively. From an earnings growth perspective, the financials, industrials, information technology, and materials sectors have each seen their earnings growth by 16.5% or more year over year, while the consumer staples, consumer discretionary, health care, real estate, and utilities sectors have each seen their earnings grow by less than 3% year over year, with the consumer discretionary sector actually reporting a 0.6% earnings drop.

Japanese Stocks Take A Well-Deserved Rest While Eurozone Indices Post Gains. The MSCI developed market index rose 0.8% last week even with the MSCI Japan index falling 2.1% on the week. It’s worth noting that even after last week’s drop, the MSCI Japan is still higher by 12.7% so far this year, and 87% of Nikkei 225 constituents are still trading above their 200-day moving average, implying impressive participation in the rally. Some weakness/profit taking in Japanese stocks should have been expected after such a sizable move in a short period of time. While painful in the near-term, last week’s drawdown eases overbought conditions and will put the MSCI Japan on firmer footing. In contrast to Japanese stocks, most Eurozone country indices turned out modest gains on the week, and we are encouraged by how broad-based participation has been so far this year with two-thirds of the Euro Stoxx 600 index trading above their key 200-day moving average, while the UK FTSE 100, IBEX 35 in Italy, German DAX and FTSE MIB in Spain boast an even higher percentage of stocks above this key moving average. The MSCI EAFE developed markets index carries just a 9.5% weight to the information technology sector, so investors seeking diversification with far less exposure to areas believed to be most at risk of displacement from AI could find what they are looking for in developed markets abroad.

Bonds: Geopolitical Tensions Spur Buying In Treasuries Despite Mostly Upbeat Economic Data; Currency-Hedged Foreign Bonds Fare Relatively Well; Private Credit Stress Contained For Now As High Yield Spreads Narrow On The Week.

Treasury Yields Little Changed As Mostly Upbeat Economic Data, Geopolitical Tensions Offset One Another. The 10-year U.S. Treasury yield closed the holiday-shortened week higher by 3-basis points as mostly upbeat U.S. economic data and escalating U.S./Iran tensions largely offset one another. The 10-year yield rose early in the week following a series of upbeat economic data releases on the heels of the February Empire Manufacturing survey, the preliminary reading on durable goods orders from December, and January industrial production which all surprised to the upside. The 10-year caught a bid mid-week and the yield fell as tensions flared between the U.S. and Iran, leading to a flight to quality/safety as investors sought a port in the geopolitical storm.

To close out the week, U.S. Personal Consumption Expenditure (PCE), the FOMC’s preferred inflation gauge, from December was released on Friday, with core PCE rising 0.4% month over month and 3.0% year over year, a bit hotter than the consensus estimates of 0.3% and 2.9%, respectively. But the 10-year yield barely budged as investors appeared to take their cue from the 4Q GDP report which showed the U.S. economy grew by just 1.4% year over year during the quarter, half of the 2.8% estimate. While growth to close out the year was indeed lackluster, the shortfall appears to be almost entirely due to the government shutdown in October and November. Our view remains that fiscal stimulus is likely to spur a U.S. economic upswing in the coming months/quarters, and with inflationary pressures sticky, we see minimal near-term downside for U.S. Treasury yields.

Hedged Foreign Bonds A Relative Bright Spot As The U.S. Dollar Carves Out A Base. Satellite exposures within fixed income outperformed traditional core bonds last week, in part due to the diversification benefits from these exposures derived from the relationship between the U.S. dollar and interest rates. The modest drift higher in U.S. Treasury yields was driven largely by better economic data, including stronger U.S. industrial production and durable goods orders midweek, datapoints that also pushed the U.S. Dollar Index (DXY) higher to 97.78 a relatively sizable move given its prior week close of 96.92. The advance in the greenback allowed dollar-hedged global sovereign bonds to rise by 0.4% on the week, while the Bloomberg U.S. Aggregate Bond index fell by 0.08%. From a technical perspective, the DXY has been making a series of higher lows, potentially a sign that the dollar is trying to carve out a base of support and find a near-term bottom off its January lows. The next test for the U.S. dollar stands at the 50-day moving average around 98, and that level has the potential to become a support level if the dollar can close above it in the coming weeks. Broadly, we still see appealing value in international sovereign debt markets, particularly with lofty valuations in both emerging markets and high yield bonds.

High Yield Corporates Shrug Off Private Credit Concerns, But Worthy Of Watching For Signs Of Contagion. Valuations in higher yielding bond sectors, including debt from emerging market countries and riskier U.S. corporates, improved last week as market participants struck a more cautious tone as equity market volatility picked up. The Bloomberg High Yield index finished the week with a 0.1% gain but lagged the Bloomberg Agg and higher quality Bloomberg U.S. Corporate index as the drop in U.S. Treasury yields buoyed longer duration areas. The Bloomberg USD Emerging Bond index returned 0.2% on the week as it carries a duration profile roughly double that of the U.S. junk bond benchmark. This is just one of the reasons we see emerging market bonds as a strategic exposure as there are very few assets that can provide a duration profile over 6 years with a yield-to-worst of 5.8%, as the investment grade corporate bond index carries an 8-year duration with just a 4.8% yield. From our perspective, neither emerging market debt nor corporate credit appears close to cheap, but both still hold appeal for now if sized appropriately as a component to a broadly diversified fixed income portfolio.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.