Stocks: U.S. Large Cap Stocks Gain As Mega Cap Technology Earnings Spur Optimism; Small Caps Sell Off As Hopes For A Dovish FOMC Chair Are Dashed; Stretched Positioning Worth Watching In Emerging Market Stocks, The U.S. Dollar, And Precious Metals In The Near-Term.

Download Weekly Market Commentary | February 2 2026

What We’re Watching:

- The Institute for Supply Management’s (ISM) Services Index for January is released Wednesday and is expected to fall to 53.5 from 54.4 in December. A reading above 50 indicates expansion in the services sector of the U.S. economy, while a reading below 50 indicates contraction.

- The January Nonfarm Payrolls report is released Friday. The consensus estimate calls for 65k jobs to have been created during the month, with average hourly earnings rising 0.3% month over month and 3.6^ year over year, and the unemployment rate remaining steady at 4.4%.

- The University of Michigan releases its preliminary February consumer sentiment survey on Friday. The reading is expected to fall to 55.0 from 56.4 the prior month.

Key Observations

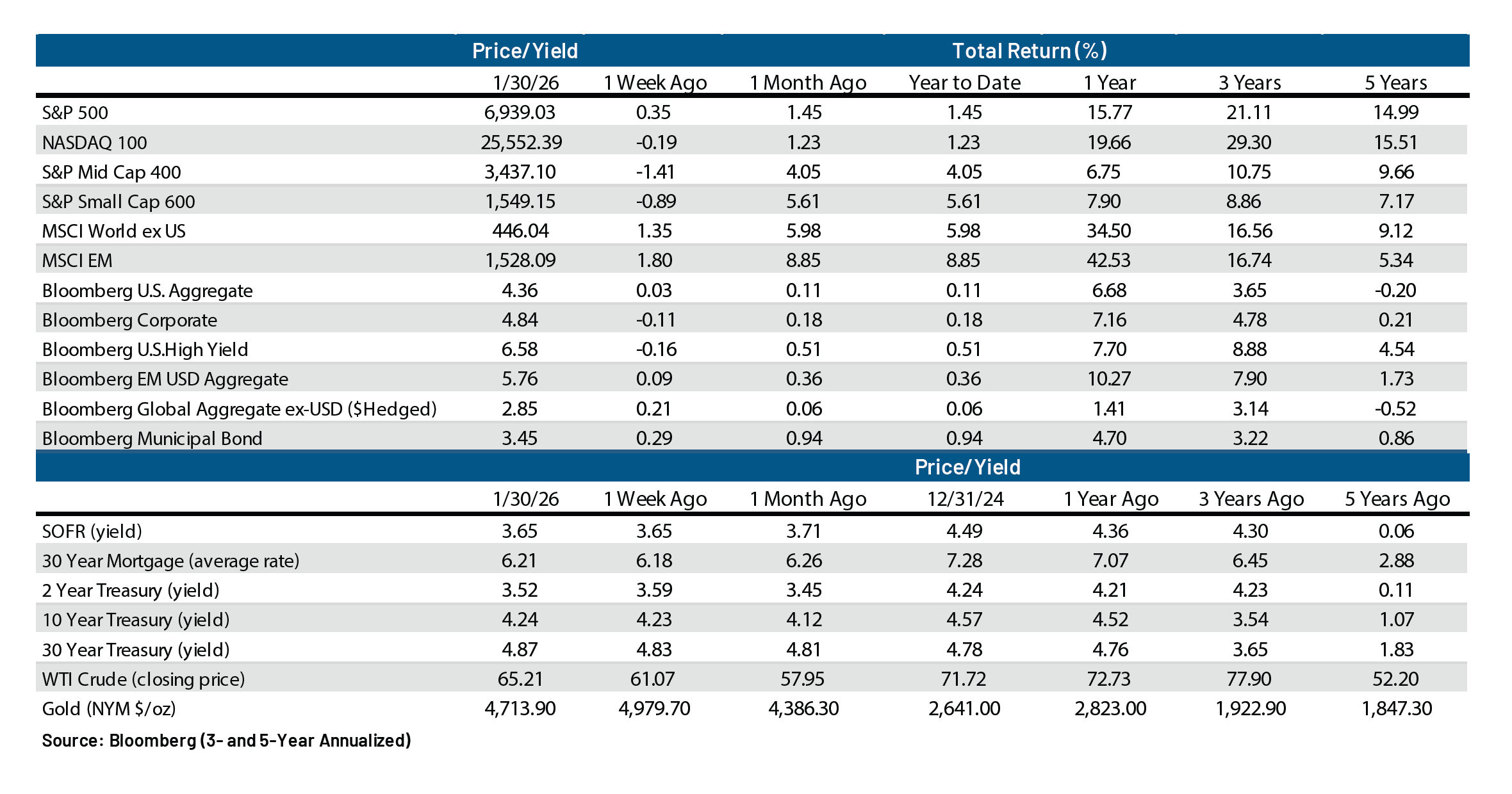

- U.S. equity indices posted mixed performance on the week with large caps gaining and small caps losing ground but all of the major indices we track closed out January in positive territory with small and mid-cap stocks outpacing their large-cap peers by a sizable margin. Historically, gains in January have, more times than not, heralded positive returns for the full year, so this is an encouraging start and feather in the cap for market bulls.

- ‘Weak dollar trades’ continued to perform well throughout much of the week as emerging market stocks and precious metals continued to rise, but gains proved fleeting as the dollar strengthened into the weekend as President Trump announced Kevin Warsh as his nominee to replace Jerome Powell as Chair of the FOMC.

What Happened Last Week:

Stocks: U.S. Large Cap Stocks Gain As Mega Cap Technology Earnings Spur Optimism; Small Caps Sell Off As Hopes For A Dovish FOMC Chair Are Dashed; Stretched Positioning Worth Watching In Emerging Market Stocks, The U.S. Dollar, And Precious Metals In The Near-Term.

The S&P 500 Is Turned Away At Round Number Resistance Of 7,000 With ‘Mag 7’ Earnings Taking A Back Seat To Moves In Precious Metals. The S&P 500 briefly eclipsed the 7,000 level for the first time ever last Wednesday before pulling back into the weekend, ultimately gaining 0.3% on the week. Volatility picked up into mid-week with investors and speculators fixing their gaze on a weaker U.S. dollar, bidding up prices of emerging market stocks and precious metals as some of the biggest beneficiaries of another bout of dollar devaluation. The move in commodities overshadowed the start of earnings season for the ‘Magnificent 7’ as Apple (AAPL), Meta Platforms (META), Microsoft (MSFT), and Tesla (TSLA) all posted quarterly results to less fanfare than they are accustomed to. After the close Wednesday, META topped estimates and saw its stock rally by 10% on the day following its release, while Microsoft, on the other hand, also surpassed the consensus estimate for earnings per share, but saw its stock price fall 10% in the immediate aftermath of the release. Microsoft’s release spurred continued selling in software names as investors view this industry as increasingly at risk of disruption from AI adoption, while capital continued to rotate into hardware names, specifically semiconductors, as a replacement. Apple rounded out the earnings deluge by topping iPhone sales estimates on Thursday and saw its share price respond by rising a more muted 0.4% on Friday. Alphabet (GOOG, GOOGL) and Amazon (AMZN) are set to post quarterly results this week, and investors will likely be focused on what each company says regarding spending forecasts for AI initiatives and to what degree sales/earnings have already seen a lift from adoption/ usage of AI.

Profit Taking Hits Small Caps As Capital Rotates Back Into Mega Cap Tech. After a strong start to the year domestic small cap stocks closed out the final week of January in the red as the Russell 2000 fell 2% with the bulk of that decline coming on Friday. Traders trimmed exposure to small caps and appeared to recycle profits into large cap tech names that have lagged early in the new year. It’s too early to call it quits on the recent bout of success for smaller cap companies which are still showing relative strength against large caps, but with Friday’s hotter producer price inflation (PPI) data, both the FOMC may and the small cap rally may be on an extended hold. Market participants quickly jettisoned small caps after the announcement that Kevin Warsh would be the nominee for Fed Chairman as they reconciled his more dovish recent remarks with his reputation as being more hawkish. Selling small caps on this announcement could prove to be the wrong move, particularly given our view that a cyclical U.S. economic recovery is now underway.

Relative Strength Puts The Emerging Markets Index In Overbought Territory. The MSCI EM index tacked on another 1.8% weekly gain and ended January higher by 8.8%. After such a sizable move in a short period of time, emerging market stocks may be due for a breather. Technically speaking, the index remains in fine shape well above its 50- and 200-day moving averages, and leadership has been broad-based with markets tied to Brazil, Mexico, South Africa, and South Korea – which together account for over 25% of the MSCI EM index, all higher by double-digits one month into the new year. But with a 14-day RSI (Relative Strength Index) reading of 85 last Friday, the index is now the most overbought it has been since January of 2018. Notably, after the 14-day RSI last eclipsed the 80 level on October 2, 2024, the MSCI EM index proceeded to drop 16% over the following six months as overbought conditions were worked off through a sizable price decline. We don’t expect a drop of that magnitude this time as EM tailwinds remain plentiful and powerful, but with stretched positioning and investor sentiment surrounding emerging markets at a fever pitch, a 5% pullback would likely be healthy. We maintain our preference for emerging markets over developed markets abroad but acknowledge that the MSCI EM rally may be stretched in the near term.

U.S. Dollar Drops On Tariff Threats, Fed Independence Fears Before Bouncing As FOMC Chair Nominee Is Announced. Last Tuesday, the U.S. Dollar Index, or DXY, fell to 96.21, its lowest level since March of 2022, as President Trump threatened to levy 25% tariffs on imports from South Korea in response to that country’s lack of follow through on a previously announced trade agreement. This announcement came on the heels of threats to levy 10% tariffs on a broad swath of European trading partners in response to saber rattling surrounding Greenland the prior week, but those tariffs were ultimately cancelled as a ‘framework’ was agreed upon. Recent weakness in the greenback has largely been driven by trade uncertainty stemming from tariff announcements, with some of the downside driven by expectations for a ‘dovish’ FOMC Chair come May, but Kevin Warsh’s nomination alleviates some of the market’s concerns surrounding Fed independence. It’s difficult to make a case for the greenback to strengthen materially from here as the Trump administration appears to welcome dollar weakness to make U.S. exports more attractive to foreign buyers. However, with the FOMC likely on hold into mid-year and U.S. economic growth likely to accelerate, downside for the dollar is also likely limited. Dollar stability could lead to profit taking in emerging market stocks and precious metals as those areas have benefitted greatly from the currency’s weakness to start the year.

Approach Precious Metals With Caution As They Work Off Parabolic Moves. Prices of gold and silver rose early last week, with the former trading above $5,500 per troy ounce and the latter breaching $120 per troy ounce on Thursday before pulling back sharply on Friday as President Trump announced his nominee for FOMC Chair. There has been substantial momentum and capital driving the move higher in gold and silver of late, but with the former up by 13.3% year-to-date and the latter higher by 18.8%, even after Friday’s steep drop, there’s likely still some froth that needs to be worked off. Fears surrounding the size of the U.S. budget deficit along with tariff threats have contributed to weakness in the U.S. dollar, providing a tailwind for stores of value such as precious metals. None of the above factors driving the recent rally in precious metals are likely to turn from tailwinds into headwinds over the near-term, but positioning in the metals market reached a bullish extreme that just needed a catalyst to produce a sizable drawdown, and with Kevin Warsh viewed as a less dovish alternative, a correction in the metals market may be underway. Calling tops in commodities is a fool’s errand as no one knows when the music will stop and prices will fall, but last week’s price action had some of the hallmarks of a blowoff top. Even after Friday’s selloff, we would expect elevated volatility to persist as speculators likely still need to unwind positions in precious metals and we would approach the space with caution as this processplays itself out and until prices find a floor and stabilize.

Bonds: Treasury Yields Close The Week Little Changed Despite A Flurry Of Potentially Market Moving Headlines; President Trump Nominates Kevin Warsh To Head The FOMC; FOMC In ‘Wait And See’ Mode For The Foreseeable Future.

Rate Volatility Rising As Long Yields Tick Higher, Benefitting Shorter Duration Segments. Rates were volatile last week as the curve continued to steepen with securities on the front end of the curve outperforming. The yield on 30-year Treasuries ended the week higher by 4 basis points even as sovereign yields abroad drifted lower as President Trump announced his nomination of Kevin Warsh to lead the Fed once Jerome Powell’s term ends in May. The selection of Warsh spurred a rally in the U.S. dollar and a coincident sell off in precious metals that spurred volatility and put pressure on prices of riskier assets, including high yield corporates and their equity counterpart, small cap stocks. One of the relative outperformers in the fixed income arena was securitized credit, a recent area of increased interest for us due to less interest rate sensitivity (lower duration risk) and competitive yields in a segment of the market with strong underlying credit quality metrics.

Initial Thoughts On The FOMC Chair Nominee. On Friday, President Trump announced he was nominating Kevin Warsh to initially replace Stephen Miran as a voting member of the FOMC, and to ultimately become the next FOMC Chair once current Chair Jerome Powell’s term ends in May. Mr. Warsh was on the Federal Reserve’s Board of Governors from 2006 to 2011 and was an advisor to former Fed Chair Ben Bernanke Warsh during the 2009 financial crisis. Warsh has been viewed by market participants as the most ‘hawkish’ of the four most oft mentioned candidates for the post and in recent papers has voiced his opinion that the Fed should concentrate on inflation while promoting his belief that Fed officials “overcommunicate.” Warsh’s nomination requires two Senate approvals, one for him to take Miran’s position and another to confirm him as FOMC Chair, but that process is likely just a formality. On balance, with Warsh viewed as more hawkish than the other 3 candidates up for the post, we expect a gradual steepening of the yield curve to persist, and for the U.S. dollar to find its footing and stabilize in the near-term.

FOMC In ‘Wait And See’ Mode For The Foreseeable Future. The Federal Open Market Committee (FOMC) concluded its January meeting last Wednesday and as expected, left the Fed funds rate unchanged. There was “broad support, including from non-voters” for standing pat on rates as 10 members voted to leave the funds rate unchanged, while 2 voted for a 25-basis point rate cut. With most of the Committee believing that monetary policy is currently in a good place, the bar to chin for near-term rate cuts is exceedingly high. In his post meeting remarks, Chair Powell noted that the outlook for economic growth has improved, the labor market has shown signs of stabilizing, and inflation has performed about as expected but remains somewhat elevated. Given these remarks, we expect the FOMC to be firmly in ‘wait and see’ mode and with Powell’s term ending in May, it’s increasingly likely that any additional rate cuts won’t materialize until the back-half of ’26.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.