Stocks: Earnings Take a Backseat To Tariff Headlines; Drop In Treasury Yields Briefly Boosts SMid; S&P 500’s 3-Month Consolidation Continues; Latin America, Especially Brazil, Is The Standout In Emerging Markets So Far In ’25.

Download Weekly Market Commentary | February 10 2025

What We’re Watching:

- The National Federation of Independent Business (NFIB) releases its small business optimism index for January on Tuesday with a 104.7 reading expected versus a better 105.1 in December.

- The U.S. Consumer Price Index (CPI) for January is released Wednesday. Headline CPI is expected to rise 0.3% month over month and 2.9% year over year versus 0.4% and 2.9% readings in December. Core CPI, which excludes food and energy, is expected to rise 0.3% month over month and 3.1% year over year versus 0.2% and 3.2% readings the prior month.

- U.S. Producer Price Index (PPI) for January is released Wednesday, PPI Final Demand is expected to rise 0.3% and 3.2% year over year, which compares to 0.2% and 3.3% in December. Wholesale prices impacting PPI flow through to consumer prices (CPI) with a lag, making this reading worth watching for the impact wholesale prices might have on core PCE, the FOMC’s preferred measures of inflation, as well as on core CPI in the coming months.

Key Observations

- Stocks largely shrugged off trade uncertainty to close the week little changed with foreign markets faring best as the U.S. dollar softened and investors appeared to take a ‘wait and see’ approach to the prospect of tariffs as the week progressed. Uncertainty tied to the outlook for trade/ tariffs could weigh on investor sentiment and positioning over the near-term with headline risk contributing to bouts of volatility along the way.

- Markets abroad have had a strong start to the year and continued to perform well on an absolute and relative basis despite trade rhetoric ramping up. Participation or breadth across the Eurozone and U.K. is encouraging as country indices tied to France, Germany, Italy, Spain, Switzerland, and the U.K. are all higher by 5% or more year- to-date.

- U.S. Treasury yields fell modestly on the week as tariff uncertainty led to concerns surrounding economic growth in the coming quarters. The move lower in yields early in the week was magnified by offsides positioning as traders were short Treasuries banking on yields moving higher and were forced to buy bonds to cover those positions, leading to an outsized move down in yields. The move lower in Treasury yields over the balance of the week is understandable, but appears overdone, and we still see minimal potential downside for Treasury yields/upside for bond prices over the near-term as growth concerns appear overblown.

What Happened Last Week:

Stocks: Earnings Take a Backseat To Tariff Headlines; Drop In Treasury Yields Briefly Boosts SMid; S&P 500’s 3-Month Consolidation Continues; Latin America, Especially Brazil, Is The Standout In Emerging Markets So Far In ’25.

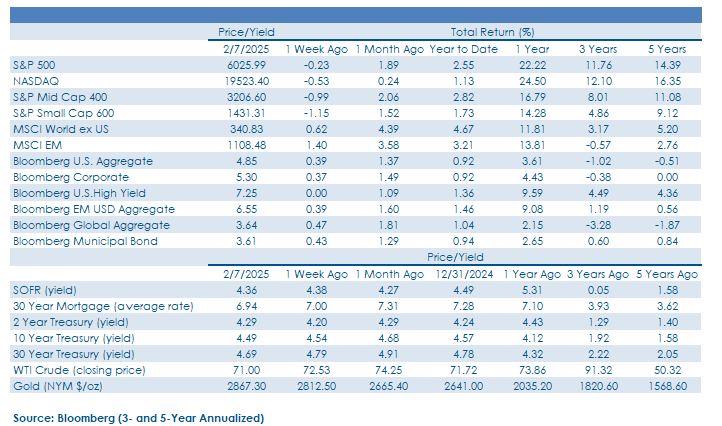

The S&P 500 Recoups Early Week Losses To Close Little Changed As Investors Take A ‘Wait And See’ Approach To Tariffs. U.S. stocks sold off early last week as tariff headlines led indices to open sharply lower on Monday, but after the U.S. announced tariffs on goods imported from Canada and Mexico would be delayed until March stocks appeared to find their footing, with the S&P 500 ending the week with a modest 0.2% loss. The move lower in U.S. stocks early in the week was relatively modest given the wide range of potential trade-related outcomes, most of which would see estimates for global economic growth falling and inflationary pressures building. The restraint shown by investors last week is evidence that market participants have largely taken a wait and see approach to tariffs as U.S. stocks and Treasury bonds ended the week little changed. The prevailing sentiment appears to be that the U.S. will come to agreements with its primary trading partners in the coming month(s) with minimal downside risk to global growth and corporate profits. While that would also be our base case, falling in-line with the consensus is an uncomfortable spot to be in, and we expect volatility in stocks and interest rates over the near-term as investor sentiment and risk appetite remains on shaky ground.

Domestically Focused Small Caps Hold Up Amid Tariff Uncertainty, Drop In Treasury Yields. The hot and cold trade situation last week had market participants take another look at areas that could prove to be relatively insulated from tariff uncertainty, and capital appeared to flow into U.S. small-caps early last week due to the domestic focus and reliance of this cohort of stocks. Some softer labor data in the JOLTS report and Jobless Claims numbers forced bond yields lower, boosting debt-laden small caps as well. Macro tailwinds capable of generating positive economic surprises and a sustained bid under small caps over the near-term are difficult to identify and this pocket of the market may remain under-owned as investors are likely to favor larger, better capitalized companies capable of weathering volatility tied to policy uncertainty.

The S&P 500 Still In Okay Shape, Technically Speaking, After A 3-Month Consolidation. The S&P 500 turned out a respectable 2.7% gain during January, starting the year off on a strong note. But very little has changed from a technical perspective over the past month as the broader index has continued to move sideways, consolidating last year’s gains. We view the 6,070/6,100 zone on the S&P 500 as a ceiling of significant resistance and a weekly close above the high end of that range would be most welcome and potentially provide a springboard for U.S. large-cap stocks to retest highs around 6,120. The S&P 500 bounced sharply off of Monday’s low at around 5,925, making this level worth watching as potential support, but if tariff rhetoric ramps up and trade deals don’t materialize later this month, a move down to 5,700/5,725 can’t be ruled out.

Latin America A Standout Amid Hopes For Tariff De- escalation, Central Bank Easing. Emerging market stocks found their footing last week with the MSCI EM Index rallying 1.4% as the U.S. announced a 30-day delay on potential tariffs to be levied on imported goods from Mexico. The decision to hold off on tariffs spurred optimism that a deal would get done and propelled the MSCI Mexico index higher by 3.2% on the week, more than making up for losses in the prior week as trade tensions escalated. Market participants appear optimistic the two sides can come to a mutually beneficial agreement by month-end, evidenced by the Mexican peso stabilizing relative to the U.S. Dollar Index (DXY) over the balance of last week despite the country’s central bank easing monetary policy. While trade uncertainty is the primary focus for investors in Mexico, additional tailwinds last week for the country included a 50-basis point rate cut out of the Central Bank of Mexico (Banxico) with dovish guidance justified by a 3.6% year over year inflation reading on Friday. Notably, Brazilian equities also advanced last week, returning 0.4% after generating a 5.5% gain in the prior week, and the MSCI Brazil Index has already turned out a 12.9% total return in 2025. Considering the U.S. has a trade surplus with Brazil, it is likely that the country will remain above the tariff/ trade fray and investors appear to be shifting exposures into countries most insulated from trade uncertainty.

Bonds: Treasury Rally Takes The 10-Year Yield Barely Back Below The Key Technical Level Of 4.50%; Duration-Sensitive Segments The Place To Be On The Week; Corporate Issuance Ramps Up As Companies Attempt To Take Advantage Of Lower Yields; Bank Of England Cuts Key Policy Rates To Spur Growth, Points To Further Easing Ahead.

Tariff Talk, Softer Economic Data Put Downward Pressure On Treasury Yields, But Offsides Positioning Played A Key Role In The Rate Drop. Tariff/trade rhetoric sparked concerns surrounding the outlook for global growth early last week and a series of softer U.S. economic data releases contributed to downward pressure on Treasury yields farther out on the curve. The 2-year Treasury yield rose 7-basis points on the week while the yield on the 10-year Treasury dropped 9-basis points, serving to substantially flatten the 2’s/10’s curve. For the 10-year yield, while the prospect of tariffs and cooler economic data contributed to the decline, market participants carrying short positions in long-term Treasuries banking on yields moving higher also played a role as these positions needed to be unwound with traders buying bonds once the 10-year yield broke below the key technical level of 4.50%. However, the 10- year yield ended the week at 4.494% in the wake of the January nonfarm payrolls report, and it’s notable that after the initial ‘woosh’ lower in yields that buyers were noticeably absent as the week progressed. The 4.50% level is worth watching into month-end as bond investors await clarity on tariffs.

On Balance, Economic Data Softer Than Expected, With Signs Inflation Isn’t Coming Down Anytime Soon. The January JOLTS (Job Openings and Labor Turnover Survey) report showed that openings fell to 7.6 million in January from almost 8.1 million in December, while layoffs came in a bit above the consensus estimate and the December reading, showing signs of a cooling labor market that takes some of the upward pressure off inflation expectations. Also of note, the ISM Services index for January came in at 52.8, short of the 54.0 estimate and the 54.1 reading in December, evidence of some modest weakening in the services sector of the U.S. economy. On Friday, the January Nonfarm Payrolls report provided a mixed picture on the current state of the labor market. It showed 143k jobs were created during the month, below the 175k estimate, but the unemployment rate ticked lower to 4.0% from 4.1% the prior month and payrolls growth for November and December was revised higher by 100k jobs. Lastly, average hourly earnings rose 0.5% month over month and 4.1% year over year, above expectations of 0.3% and 3.8%, respectively. On balance, the payrolls report continues to point toward inflationary pressures remaining sticky over the near-to-intermediate term.

High Grade Corporates Holding Up Well Despite Elevated Issuance. The Bloomberg Corporate Bond Index gained 0.3% on the week as the drop in Treasury yields offset a modest move wider for credit spreads. Cheaper valuations were the byproduct of higher issuance, with borrowers happy to accept higher investor concessions on newly issued paper to lock in the sharp move lower in yields. A flurry of deals last week amounted to roughly $40B, shattering top-end dealer estimates of $35B while building on the 4% year over year rise in issuance thus far in 2024. From a credit worthiness standpoint, upgrades are still outpacing downgrades at the major rating agencies, an encouraging trend as valuations still appear rich with credit spreads only a handful of basis points shy of record tight levels at present. At the sector level, the earnings backdrop has so far been mixed for corporate borrowers with financials posting a double-digit positive earnings surprise, while industrials are one of the few sectors that have fallen short of expectations thus far into earnings season.

Bank of England Cuts Key Policy Rate, With Some Dovish Dissention In The Ranks. As expected, the Bank of England (BoE) lowered its key policy rate by 25-basis points to 4.50% and hinted at additional policy easing coming down the pike in the coming months. While the BoE delivered a cut as expected, there were some surprising aspects to the meeting worth noting. The BoE lowered its outlook for economic growth in the U.K. in 2025 from 1.5% to 0.75%, while noting that it expects inflation to peak at 3.7% in the 3rd quarter of this year, well above the prior forecast of 2.8%. Notably, two of the nine voting members were in favor of a larger 50-basis point rate cut in response to a challenging growth outlook in the U.K., with one of the two dissenters viewed as an “uber-hawk,” evidence of how dire the country’s growth outlook has become. Yields on U.K. gilts and the British pound sterling fell only modestly on the heels of the BoE’s dovish monetary policy outlook.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.