Stocks: Investors Adopt A Defensive Posture As Geopolitical Risk, Economic Slowdown Fears Dominate; A Mixed Week For The Magnificent 7; Small Cap Rally Reverses Amid Signs Of Labor Market Weakness; Worst Day For Japanese Stocks Since 1987 Shouldn’t Be Ignored.

Download Weekly Market Commentary | August 5 2024

What We’re Watching:

- The U.S. Treasury is set to auction $42B of 10-year notes on Wednesday, followed by $25B of 30-year bonds on Thursday. With yields on long-term Treasuries falling over the past month, we will be monitoring appetite from direct bidders, primarily insurance companies and pensions, after strong demand from this cohort at recent auctions for long-dated U.S. Treasury paper when yields were higher.

- Initial jobless claims for the week ended August 3rd are released Thursday and will be closely watched after jobless claims, manufacturing employment, and the July nonfarm payrolls report pointed toward a rapidly cooling labor market last week and contributed to economic slowdown fears.

- Earnings season continues to roll along with approximately 15% of S&P 500 constituents set to post results in the coming week. Excluding Nvidia, which is scheduled to report on August 28, Magnificent 7 earnings are in the rearview mirror and the S&P 500 may now be able to catch its breathe after a volatile and challenging two-week stretch.

Key Observations

- Fears of a U.S. economic slowdown built last week as a series of readings pointed toward the labor market cooling at a more rapid pace in July, calling into question the outlook for U.S. economic growth in the coming quarters. These concerns led to a flight to safety into U.S. Treasuries and defensive, dividend paying stocks, and outflows from small cap stocks.

- The FOMC met last week and held rates steady while leaving the door open for a cut in September. Bond yields fell sharply over the balance of the week as market participants appear to believe the Committee should have already cut and is behind the curve when it comes to easing monetary policy to support the labor market. Market participants now believe a 50-basis point cut in September is more likely than a 25-basis point cut and are pricing in over 1% of rate cuts between now and year-end, leading us to believe the pendulum may have swung too quickly and too drastically toward a rapid pace of policy easing.

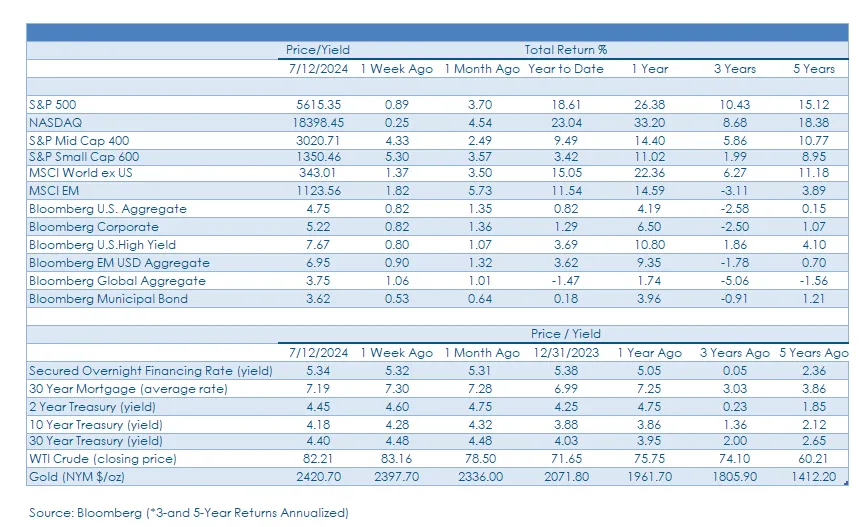

- U.S. large cap stocks outperformed small caps on the week with defensive sectors (health care, consumer staples, real estate, utilities) leading while the rotation into economically sensitive sectors (financial services, industrials, materials) in recent weeks reversed course.

What Happened Last Week:

Stocks: Investors Adopt A Defensive Posture As Geopolitical Risk, Economic Slowdown Fears Dominate; A Mixed Week For The Magnificent 7; Small Cap Rally Reverses Amid Signs Of Labor Market Weakness; Worst Day For Japanese Stocks Since 1987 Shouldn’t Be Ignored.

Defensive Sectors Fare Well In An Otherwise Tough Week For U.S. Large Caps. There was a decidedly defensive tone to U.S. large cap leadership last week with the consumer staples, health care, real estate, and utilities sectors performing best, with communication services also staging a comeback after Meta Platforms posted solid quarterly results.

Continued Profit Taking In The Magnificent 7 As Investors Turn Cautiously Optimistic On The Group Post-Earnings. On the heels of lofty expense guidance out of Alphabet (Google) and Tesla the prior week, investors were justifiably concerned and cautious leading into earnings releases out of Microsoft, Meta Platforms, Amazon, and Apple last week. On balance quarterly results were solid, but forward guidance did little to ease investor concerns surrounding how long it would take for these companies to begin to monetize or see a return on investment from sizable capital expenditures on artificial intelligence (AI) infrastructure. Microsoft results surpassed expectations on most key metrics, but investors sold the stock as growth in Azure, Microsoft’s cloud computing platform, fell modestly short of expectations. The stock recovered sizable early losses but still closed the week lower by 3.9% once investors digested the release and took note that the Azure shortfall was driven by limited supply, not demand concerns. Meta Platforms reported Wednesday, and while the company raised the lower bound for expenses in the coming quarters, it also guided sales expectations higher as the company is already seeing a return on its AI investments via higher advertising revenue. Meta finished the week higher by 4.8%. Amazon and Apple posted results after market close on Thursday, with the former falling over 9% on Friday, contributing to weakness in the S&P 500 into the weekend. For its part, Apple posted impressive all-around results and the stock responded by rising 3% on the day and 0.8% on the week but was a case of sometimes it matters when you report more than what you report.

Small Caps Give Back Recent Gains As Labor Market Data Softens, Economic Growth Concerns Build. The S&P Small Cap 600 index fell 5.5% over the balance of last week as a series of data points strongly hinted at a cooling labor market, stoking fears of an economic slowdown with the FOMC potentially behind the curve when it comes to easing monetary policy.

Japanese Stocks Have Their Worst Day Since Black Monday In 1987. Japan’s Nikkei 225 index fell 5.8% last Friday and is now down by 15% just since July 11. Much of the drop in Japanese stocks is attributable to the country’s currency, the yen, strengthening in recent weeks as the Bank of Japan (BoJ) raised rates and began selling Japanese Government Bonds in an effort to prop up the currency after seeing it plummet to 160¥ per U.S. dollar in early July, an unsustainable level despite the positive impact a weaker yen would have on Japanese exports. The yen stabilizing may be required for Japanese stocks to regain their footing, but after the recent pullback active managers will likely find attractive opportunities amongst the rubble.

Escalating Middle East Tensions Fail To Buoy Energy Stocks As Economic Growth Fears Dominate. In response to an attack early last week that killed some of its citizens, Israel retaliated by assassinating a Hezbollah commander last Tuesday in Lebanon, and a senior Hamas official in Iran on Wednesday. These moves sparked fears that the Israel/ Hamas conflict was all but certain to spill over and spread throughout the Middle East, curbing crude oil supply coming out of the region in the coming months. Interestingly, despite escalating tensions both West Texas Intermediate (WTI) and Brent crude oil finished the week lower, and the S&P 500 energy sector closed the week with a 4% loss as investors appeared to increasingly buy in to the economic slowdown narrative.

Bonds: Weak Labor Market Data, Geopolitical Concerns Put Downward Pressure On Treasury Yields; Some Signs Of Fear As Credit Spreads Widen On The Week.

10-Yr. Treasury Yield Sinks Below 4% As A Cooling Labor Market, Geopolitical Fears Spur A Flight To Safety. Last Thursday, for the first time since early February, the yield on the 10-year U.S. Treasury closed below 4% as signs of a cooling labor market combined with fears of a broader conflict breaking out in the Middle East to spur a flight to safety and increase demand for long-term U.S. Treasury debt. The 10-year Treasury yield experienced the largest downward move, falling by 40-basis points on the week to close at 3.80% as the FOMC’s mid-week message, while dovish, wasn’t dovish enough and investors began to fear an economic slowdown amid continued signs of cooling in the labor market. Directionally, the move lower in Treasury yields over the balance of last week makes sense with the escalation in the Middle East. However, while the labor market is cooling, payrolls rising by 114k during July is far from a sign the U.S. economy is on the brink of recession, and we still see 1.5% to 2% GDP growth over the balance of 2024. Last week’s move lower in yields may prove to be overdone, and we will find out just how overdone it may be mid-week when the Treasury auctions off 10-year notes and 30-year Treasury bonds. Much of the move lower in Treasury yields last week could reverse in the coming week(s) if investors begin to balk at buying 10-year Treasuries at a yield below 4%.

Probability Of A Half-Point Rate Cut In September Rises Post-FOMC, July Payrolls. The published statement from the FOMC referenced the two sides of its dual mandate – full employment and price stability – coming more into balance and the Committee altered its inflation outlook from “modest progress” to “further progress,” two tweaks taken by the market as the FOMC moving closer to cutting rates. Chair Powell’s post-meeting remarks noted that a discussion on easing policy at last week’s meeting had taken place but that most Committee members believed leaving rates unchanged and waiting for more inflation data was the proper path to take. At the start of last week, Fed funds futures were pricing in three 25-basis point cuts by January, but by the weekend that number had climbed to between four and five quarter-point cuts by year-end. The weaker July payrolls report on Friday threw fuel on the fire and at the end of the week Fed funds futures viewed a 50-basis point cut in September as the most likely outcome. The weaker payrolls report is likely causing some angst within the FOMC, and the likelihood of a half- point cut in mid-September is higher than it was prior to the release, but the Committee isn’t going to panic and risk losing credibility, thus, we believe over 1% of rate cuts between now and year-end is an overreaction to recent data and unlikely to come to fruition.

Debt Issuance Heats Up In The Lead-Up To The FOMC Meeting. Corporate borrowers front-loaded debt sales last week with over $32B in corporate bonds issued on Monday and Tuesday, perhaps surprisingly, coming to market ahead of the mid-week FOMC meeting. The flurry of borrowing before Federal Reserve announcement on rates has become routine in recent quarters as corporations have attempted to side-step volatility that can ramp up on the heels of FOMC announcements and ratchet rates higher. Netflix and Citigroup, both investment grade names, were among the biggest issuers tapping the market, floating nearly $6B of new paper. The Netflix issue, specifically, saw strong demand as the deal was 4 times oversubscribed with spreads tightening on the new bonds by as much as 30-basis points. Buyers haven’t been shy about their interest in adding to their exposure to higher quality corporate bonds, especially on the intermediate and long end of the yield curve where pensions and institutions have been big buyers of Treasuries of late as they seek to lock in higher rates which could drift lower should rates decline as anticipated when the FOMC begins easing monetary policy.

July Nonfarm Payrolls Fall Well Short Of Expectations, But The Devil Is In The Details. The Nonfarm Payrolls report for July was released Friday and showed 114k jobs were created during the month, below the consensus estimate of 175k, and the unemployment rate rose to 4.3% from 4.1% the prior month as the labor force participation rate ticked higher by 0.1%. While the weaker headline reading and rising unemployment rate garnered headlines, there are reasons this release may be more noise than signal. Specifically, the response rate to the July survey remained exceedingly low by historical standards; Hurricane Beryl making landfall during the month could have delayed hiring; and, lastly, unseasonably warm temperatures during the month were a drag on average hours worked which fell to 34.2 from 34.3 the prior month. The labor market is still cooling, not cracking, in our view, and we see little rea- son to alter our view that the U.S. economy remains on track to grow between 1.5% and 2% this year on the heels of this release and the sharp move lower in Treasury yields is overdone if one ascribes to this view.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.