Stocks: U.S. Large Cap Stocks Attempt To Rally, But Bottoming Is A Process And Will Take Time; Small Caps Selloff Despite Earnings Surprises; Japan’s Stock Market, Currency Likely To Remain On Shaky Ground.

Download Weekly Market Commentary | August 12 2024

What We’re Watching:

- The July Producer Price Index (PPI) is released Tuesday. Headline PPI is expected to rise 0.2% month over month, in- line with the June reading, and 2.2% year over year, which would be a significant deceleration from 2.6% year over year growth in June. PPI is a gauge on wholesale prices and is worth watching as PPI flows through into prices of finished goods and will impact Consumer Price Index (CPI) and Personal Consumption Expenditure (PCE) in future months.

- The July Consumer Price Index (CPI) is released Wednesday. Headline CPI is expected to rise 0.2% month over month, above the -0.1% reading from June, and 3.0% year over year, in-line with the June figure. Core CPI, which excludes volatile food and energy prices, is expected to rise 0.2% month over month versus 0.1% last month, and 3.2% year over year, below the 3.3% June reading. While not the FOMC’s preferred inflation gauge, CPI will likely be closely watched by market participants as a potential indication of what to expect when PCE is released at the end of August.

- The University of Michigan Consumer Sentiment Index for August is released Friday and is expected to rise/improve to 68.5 from 66.4 the prior month. Given economic growth concerns centered around a cooling labor market, this reading is worth watching as a gauge on how the U.S. consumer is currently feeling about the availability of jobs, inflation, and other measures.

Key Observations

- U.S. large cap stocks remained volatile but ended the week little changed as a sharp selloff early in the week reversed course as buyers began to step in to pick up shares of recent laggards in the energy, financial services, industrials, and information technology sectors, among others. Defensive sectors that had garnered inflows in recent weeks as investor risk appetite waned, specifically, health care and utilities, were notable underperformers.

- Japanese stocks swung wildly over the balance of the week as volatility in the Japanese yen persisted, and with Bank of Japan (BoJ) Governors forfeiting credibility by sending mixed messages to markets, sentiment surrounding Japan’s economy and Japanese stocks could persist for some time.

- Poorly received 10- and 30-year Treasury auctions on Wednesday and Thursday put upward pressure on bond yields, and if economic growth fears continue to subside on better than feared initial jobless claims in the coming weeks, prices of Treasury bonds could fall further. Notably, riskier higher yielding corporate bonds outperformed higher quality investment grade issues on the week, despite what was a general risk-off tone to the market. Corporate bonds, both investment grade and below investment grade, remain relatively appealing versus Treasuries at present, and can provide valuable income and diversification benefits.

What Happened Last Week:

Stocks: U.S. Large Cap Stocks Attempt To Rally, But Bottoming Is A Process And Will Take Time; Small Caps Selloff Despite Earnings Surprises; Japan’s Stock Market, Currency Likely To Remain On Shaky Ground.

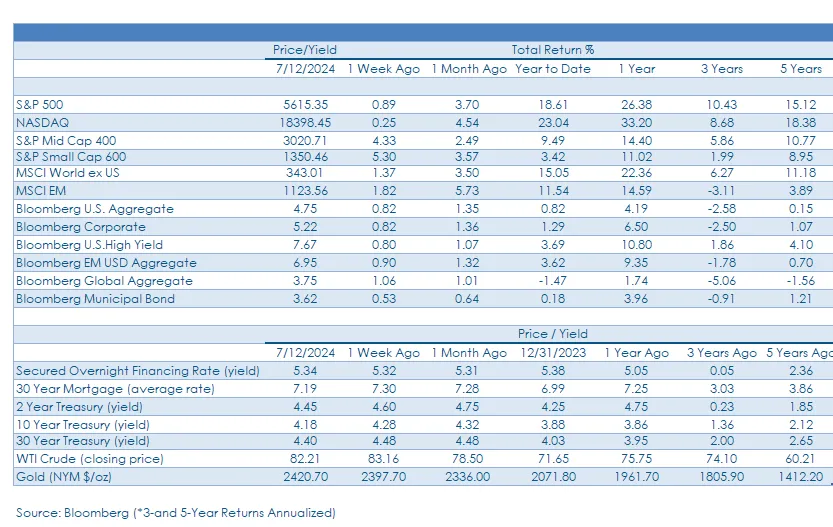

U.S. Large Caps Tread Water After A Tough Three Week Stretch, But The Bottoming Process Will Take Time. After three consecutive weeks of negative returns over which time the S&P 500 lost 4.7%, the index continued to chop around in a wide trading range last week before ending little changed. The communication services, energy, financial services, industrials, and information technology sectors outperformed while recent leaders such as consumer staples, health care, real estate, and utilities all lagged. The price action of the last week is a step toward repairing some of the technical damage done of late, but investor risk appetite is unlikely to return in a big way in the next few weeks, leaving the S&P 500 in no man’s land at present. When the market opened sharply lower last Monday the S&P 500 was 9% below its mid-July all-time high, but after trending higher over the balance of the week, the index closed 6% below that level. This is notable as historically the S&P 500 has experienced two 10%-plus corrections per year and, while painful, the most recent pullback has still fallen short of that threshold. Our suspicion is that bears won’t give up easily and may try to make another run at a true correction in the coming month(s) as the August through October stretch in presidential election years has been historically weak for stocks. They tend to peak or top because of events such as the unwind of the Japanese yen carry trade, while bottoming is a process that takes time, sometimes weeks, perhaps longer. Pullbacks often follow a similar path or pattern with an initial ‘whoosh’ or sharp drop on high trading volume over two to three trading days, followed by an oversold bounce with selling into strength, then a period of backing and filling to find a durable floor of support. We could be early in stage three as Thursday’s 2.3% S&P 500 bounce held into the weekend, and with little in the way of potential market moving data in the next two weeks, this would be a logical spot for backing and filling to take place. The S&P 500 could mark time trading between its 50-day (5,446) and 200-day (5,032) moving average leading up to the Kansas City Fed’s Jackson Hole Symposium on August 24-26 and Nvidia’s quarterly report on August 28, and both events could prove market moving.

Small Caps Slip Further Despite Positive Earnings Surprises.

U.S. small cap stocks saw profit taking in the first full week of August as risk appetite waned and the S&P 600 broke below its 50-day moving average, which may now become a ceiling of resistance. Recent momentum in smaller company stocks faded for the second consecutive week with the S&P Small Cap 600 down 1%, with a 3.1% decline Monday putting the index behind the 8-ball for the remainder of the week. The recent weakness in small caps flies in the face of fundamentals as roughly 90% of the S&P 600 has now reported quarterly results with an 11.0% upside earnings surprise, indicating small companies have been judiciously managing costs as sales growth remains challenging. Earnings breadth has also been healthy with nine out of the eleven sectors topping the consensus earnings estimate. This leads us to conclude that small caps could be primed and ready to benefit should investor sentiment and risk appetite improve, as is often the case following a market correction and/or economic reacceleration.

Rollercoaster Ride For Japanese Stocks Is Likely To Continue. Japan’s Nikkei 225 opened last Monday down 10.7% from Friday’s close as the unwind of the carry trade (borrowing in the lower yielding Japanese yen, converting it into U.S. dollars and investing in riskier assets such as stocks and cryptocurrencies) continued to rattle markets. However, after beginning the week on a sour note, the Nikkei staged a comeback, rebounding 9.2% on Tuesday and Wednesday as a Deputy Governor from the Bank of Japan (BoJ) calmed markets by stating that so long as markets remain unstable and volatile the BoJ would not raise rates. These remarks served to weaken the Japanese yen and the Nikkei 225 fell a modest 2.3% on the week. The BoJ will likely need to raise rates in the coming quarters, but to what degree remains uncertain as the central bank will likely need to closely monitor the U.S. economy. A soft-landing scenario in the U.S. would benefit central bankers here and in Japan as rate cuts out of the FOMC would be more gradual and provide the BoJ with some breathing room. Conversely, signs of a more pronounced economic slowdown here would lead to calls for more drastic policy action with more rate cuts priced in between now and year-end, which would likely weaken the U.S. dollar versus the yen, complicating matters for the BoJ as they would need to tighten policy but by doing so would risk the yen appreciating in a material way, weighing on Japan’s export-heavy economy. The BoJ is in a tough spot and market participants will likely put pressure on them to do more in the coming months, with volatility in the yen and Japanese equities likely to persist as a result.

Bonds: Treasury Yields Bounce Amid Weak Auction Results, Fading Economic Growth Fears; 10-, 30-Year Treasury Auctions Poorly Received As Buyers Balk At Lower Yields; Higher Yielding Corporate Bonds Outperform Higher Quality Issues On The Week.

Buyers Balk At Lower Yields Leading To Weak 10- And 30- Year Auction Results. The U.S. Treasury came to market with $42B of 10-Year notes on Wednesday and found lackluster demand. The bid-to-cover was just 2.32 times, the lowest reading since December of 2022 and the dealer community was forced to take down 17.8% of the issue, the highest percentage since April. The 10-year auction was followed by $25B of 30-Year bonds on Thursday, and the results were no better for bond bulls. The bid-to-cover on the 30-year auction was 2.31, or the 2nd lowest since November of 2023, and dealers took down 19% of the issue, the highest percentage since November of 2023 and the 2nd highest percentage dating back to December of 2021. With Treasury yields falling sharply in recent weeks, we were closely monitoring these auctions for signs of waning demand on the part of pensions and insurance companies, and that appears to have been the case. With economic slowdown fears easing as initial jobless claims from the prior week came in below the consensus estimate, a 4%-plus 10-year yield may be necessary to draw deep pocketed buyers back in the coming months.

Treasury Yields Bounce As Initial Jobless Claims Fall, Easing Economic Growth Concerns. In recent weeks, a series of data points appeared to show signs of a rapidly cooling, if not cracking labor market, which is why we viewed last Thursday’s release of initial jobless claims for the week ended August 3rd as potentially market moving for stocks and bonds. Initial claims for unemployment insurance for the week came in at 233k, below the 240k estimate and the 250k reading from the prior week, calling into question the narrative that the labor market was rapidly cooling, and that U.S. economic growth was set to slow materially in the coming months. Initial and continuing jobless claims will be closely monitored by investors for signs of deterioration in the labor market and potentially the U.S. economy, but we continue to see signs the labor market is normalizing, not cracking, and continue to expect 1.5% to 2% GDP growth in 2024.

Higher Quality Corporate Bonds Lag As Treasury Yields Move Higher. Investment-grade (IG) corporate bonds, which closed out July on a high note, came under pressure last week as better than feared jobless claims and weak Treasury auctions forced yields on longer duration bonds higher. Investment grade corporate bonds felt that sting more than most, the Bloomberg U.S. Corporate index falling by 0.7% on the week, giving back around one- third of the prior week’s gain despite credit spreads narrowing over that period. Higher quality corporate bond valuations, broadly speaking, may be unappealing relative to historical norms, but the index yields 60-basis points above the Bloomberg Aggregate while carrying a duration of just over 7 years, versus the Agg at just above 6 years. Investors can clip a higher coupon from IG corporates while still benefiting from a modest drop in Treasury yields, assuming yields don’t drop sharply on rising recession fears.

High Yield Bond Spreads Widen, Then Narrow As Cheaper Valuations Attract Buyers. A sharp jump in volatility last Monday put downward pressure on prices of riskier- assets and high yield corporate bonds were no exception as the index’s option-adjusted spread (OAS), or credit spread, rose by 22-basis points to 381-basis points over like maturity U.S. Treasury bonds. Investors who blinked likely missed Monday’s selloff in high yield as buyers stepped in and valuations tightened over the balance of the week with the OAS closing out the week at 339-basis points and the High Yield index eked out a 0.2% gain. Monday’s brief spread widening in high yield resulted in a shuttered primary market as no new paper priced until Wednesday before issuance rebounded to $5.7B over the back-half of the week as issuers rushed to take advantage of the pause in volatility and fall in Treasury yields. Corporate borrowers that front loaded new issuance ahead of the FOMC meeting were left to ponder if they should have waited until after the fact to issue debt at even lower yields, but delaying coming to market by even a week would have been perilous given the lack of liquidity early last week. Limited supply and borrowing restraint by lower-quality issuers increases the appeal of high yield corporate bonds and improves the fundamental outlook and given our view that the U.S. economy remains on sound footing, we remain neutral on this segment of the fixed income market.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.