Market Thoughts As Tensions In The Middle East Flare

Download Market Thoughts | March 3 2026

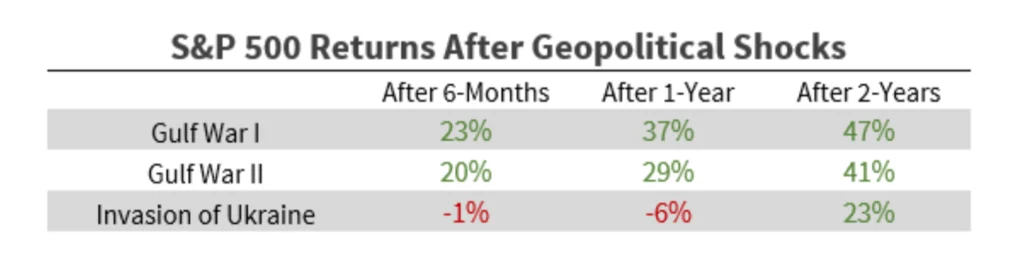

Over the weekend, tensions in the Middle East reached an apex as hostilities in Iran escalated, setting off a series of events that impacted commodity, currency, stock, bond, and volatility markets, albeit likely not in the ways the consensus believed or thought they would. Before we get into the details, it’s worth remembering that historically geopolitical shocks have short-term impacts but carry minimal impact on market fundamentals that drive assets higher long-term.

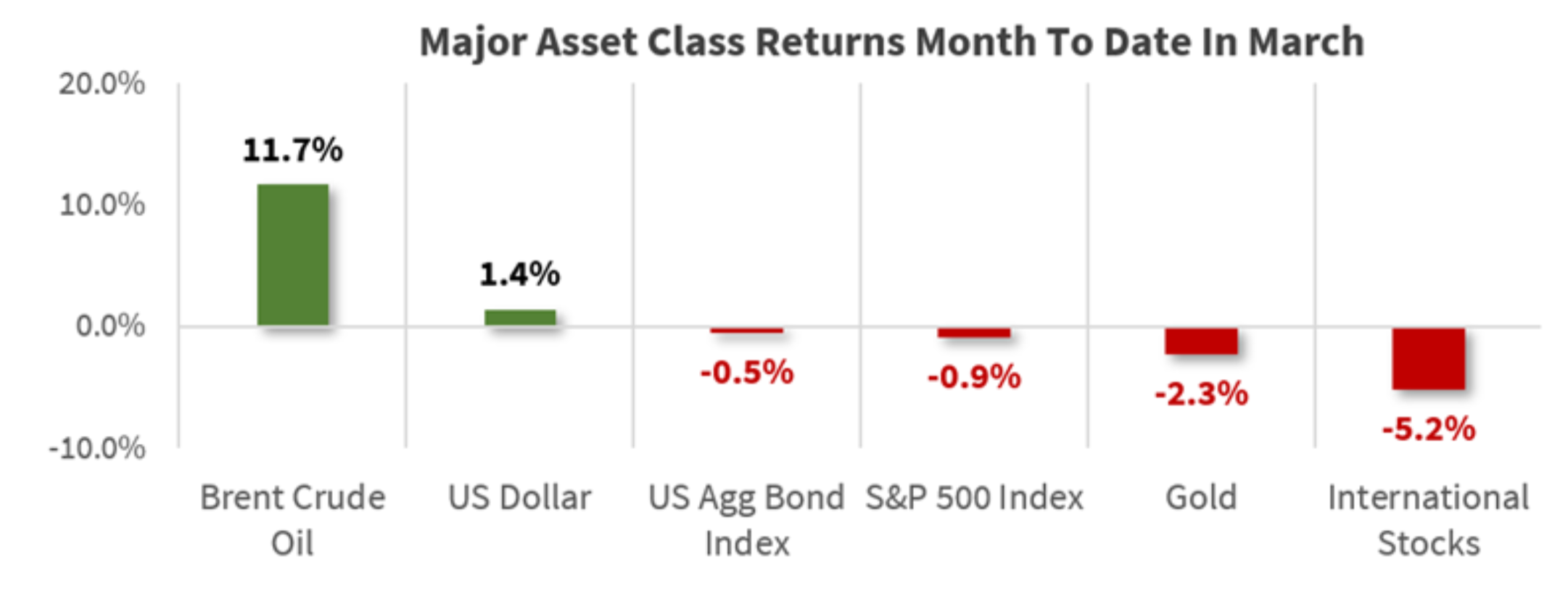

Source: Bloomberg; Data as of 3/3/26 unless otherwise indicated Past performance is not an indication of future results.

Energy Markets: Taking each of these one by one, the most notable and least surprising move was the sizable advance in energy-related commodities. West Texas Intermediate (WTI) crude oil rose from $67 per barrel on February 27 to $77 early on March 3, while Brent crude jumped from $72 to $83 in the same time frame as fears of a prolonged supply disruption put upward pressure on prices as Iran announced on Monday that the Strait of Hormuz, through which some 20% of global crude oil traffic was ‘closed.’ Rising crude prices is undoubtedly a big part of the story, but a spike in natural gas prices is also a variable worth watching, particularly for Europe.

The price of Henry Hub natural gas stateside jumped almost 10% on Monday, but at $3.13 per million British thermal units (BTUs), the U.S consumer can more easily manage this move than can the European consumer which has now seen the front-month (April) contract for Dutch natural gas spike from $31 last Friday to $55 per million BTUs on Tuesday. Luckily, warmer months lie ahead for Europe, which will ease demand requirements but the rise in natural gas and gasoline prices stemming from Middle East tensions will weigh on consumer spending, put upward pressure on inflation in the near-term and tamp down economic growth to some degree. The duration of the fighting along with how quickly traffic through the Strait of Hormuz normalizes is of the utmost importance as the longer this drags on, the more negative the ramifications for the Eurozone and U.K. economies.

Gold: Outside of energy markets, gold made a notable move higher on Monday, closing above $5,400 per troy ounce as safe haven flows and demand for inflation protection boosted precious metals. However, that move reversed sharply on Tuesday as the U.S. dollar appreciated and U.S. Treasury yields rose. Gold’s rise in 2025 and into 2026 was predicated largely on the view that the U.S. dollar would continue to weaken as capital flowed out of the U.S. in favor of foreign markets, and long positions in gold have consistently been stretched. The reversal lower in recent days is notable as gold was turned away around $5,400, falling short of $5,500, a level that provided resistance in late January, and a series of lower highs could signal profit taking and tougher sledding ahead.

Currencies: In the currency market, the U.S. Dollar Index, or DXY rose from 97.60 on Friday to 99.60 early Tuesday, making a year-to-date high as capital seeking a relative port in the storm sought safety stateside. The DXY is now above its mid-January high with November resistance at 100.20 in sight, a notable move given the dollar bearishness that dominated to start the year. A break above and weekly close above 100.20 on the DXY would mark a character change and could spur further repositioning in favor of U.S. stocks at the expense of foreign stocks that outperformed in ’25 and throughout the first two months of ’26.

Stocks: The dollar’s advance and the price jump in crude/natural gas have weighed heavily on foreign markets, with the MSCI EAFE developed markets index and the MSCI Emerging Markets (EM) index falling sharply to start the month. This stands in contrast to the S&P 500’s more measured decline, evidence that even amid heighted AI disruption concerns, U.S. large-cap stocks are still viewed as relatively defensive, garnering inflows as market participants jettison more economically sensitive exposures abroad. Weakness has been broad-based abroad and profit taking has appeared indiscriminate with Eurozone, Japanese, and U.K. markets each falling over 4.5% in the first two trading days of the month. These markets have provided leadership since the start of 2025 and rose largely unchecked since then, leading to larger pullbacks when they do materialize as the need to book profits dominates for those failing to do so along the way.

On the emerging markets front, there have been few places to hide with the MSCI Emerging Markets (EM) index falling over 5% in the first two days of trading in March, and leaders such as South Korea have seen larger drawdowns than the broader index as profit taking has been painful. The Middle East situation remains tenuous with uncertainty continuing to dominate, which could keep upward pressure on the U.S. dollar and energy prices, potentially weighing more on ‘growthier’ pockets of the developing world. However, the longer uncertainty persists, the more market participants could also become attracted to commodity-producing developing economies such as Brazil, which has also seen capital outflows as investors have chosen to sell first and ask questions later. Uncertainty breeds opportunity, and when volatility ramps up and market participants sell what they can, not necessarily what they should, that’s when tactical opportunities are presented, and in time we would expect that to be the case for developed and developing markets abroad.

Source: Bloomberg

Past performance is not an indication of future results.

Bonds: Long-term U.S. Treasuries garnered inflows last week as investors sought safety, forcing yields lower. But with energy prices rising, inflation concerns have dominated and market participants have removed interest rate cuts expected to materialize in the coming months from the equation. The longer energy prices remain elevated, the less likely it will be that the FOMC will have the comfort to cut the funds rate, which could put upward pressure on yields across the Treasury curve. Credit spreads could also continue to leak wider as uncertainty surrounding the economic growth outlook builds, which could present attractive opportunities for investors that have been balking at low yields/tight credit spreads in recent quarters.

Volatility: Lastly, the CBOE Volatility Index, or VIX, rose sharply in the wake of last weekend’s turmoil, reaching 28 briefly on Tuesday as demand for puts to hedge against a deeper market drawdown rose, but the VIX ultimately closed the day with a more benign 22 handle. Notably, the VIX at 28 was at its highest level since April of last year around the Liberation Day lows. All things considered, the move higher in the VIX has been somewhat subdued relative to our expectations, which is a function of investors ending last week well hedged in preparation of an eventual military conflict breaking out in Iran and potentially throughout the Middle East. Outside of the Liberation Day VIX spike that took the index briefly above 50, in the post-COVID world VIX moves higher have often peaked in the 30 to 35 zone, so further volatility could be in the cards. However, with the cost of protection (puts) rising sharply in recent days, it becomes harder for the VIX to sustain loftier levels and should tensions/fighting ease in the Middle East, market participants could be quick to remove hedges by selling their puts, leading to buying in equity indices, putting upward pressure on prices.

IMPORTANT DISCLOSURES: This publication has been prepared by the staff of Highland Associates, Inc. for distribution to, among others, Highland Associates, Inc. clients. Highland Associates is registered with the United States Security and Exchange Commission under the Investment Advisors Act of 1940. Highland Associates is a wholly owned subsidiary of Regions Bank, which in turn is a wholly owned subsidiary of Regions Financial Corporation. Research services are provided through Multi-Asset Solutions, a department of the Regions Asset Management business group within Regions Bank. The information and material contained herein is provided solely for general information purposes only. To the extent these materials reference Regions Bank data, such materials are not intended to be reflective or indicative of, and should not be relied upon as, the results of operations, financial conditions or performance of Regions Bank. Unless otherwise specifically stated, any views, opinions, analyses, estimates and strategies, as the case may be (“views”), expressed in this content are those of the respective authors and speakers named in those pieces and may differ from those of Regions Bank and/or other Regions Bank employees and affiliates. Views and estimates constitute our judgment as of the date of these materials, are often based on current market conditions, and are subject to change without notice. Any examples used are generic, hypothetical and for illustration purposes only. Any prices/quotes/statistics included have been obtained from sources believed to be reliable, but Highland Associates, Inc. does not warrant their completeness or accuracy. This information in no way constitutes research and should not be treated as such. The views expressed herein should not be construed as individual investment advice for any particular person or entity and are not intended as recommendations of particular securities, financial instruments, strategies or banking services for a particular person or entity. The names and marks of other companies or their services or products may be the trademarks of their owners and are used only to identify such companies or their services or products and not to indicate endorsement, sponsorship, or ownership by Regions or Highland Associates. Employees of Highland Associates, Inc., may have positions in securities or their derivatives that may be mentioned in this report. Additionally, Highland’s clients and companies affiliated with Highland Associates may hold positions in the mentioned companies in their portfolios or strategies. This material does not constitute an offer or an invitation by or on behalf of Highland Associates to any person or entity to buy or sell any security or financial instrument or engage in any banking service. Nothing in these materials constitutes investment, legal, accounting or tax advice. Non-deposit products including investments, securities, mutual funds, insurance products, crypto assets and annuities: Are Not FDIC-Insured I Are Not a Deposit I May Go Down in Value I Are Not Bank Guaranteed I Are Not Insured by Any Federal Government Agency I Are Not a Condition of Any Banking Activity.

Neither Regions Bank nor Regions Asset Management (collectively, “Regions”) are registered municipal advisors nor provide advice to municipal entities or obligated persons with respect to municipal financial products or the issuance of municipal securities (including regarding the structure, timing, terms and similar matters concerning municipal financial products or municipal securities issuances) or engage in the solicitation of municipal entities or obligated persons for such services. With respect to this presentation and any other information, materials or communications provided by Regions, (a) Regions is not recommending an action to any municipal entity or obligated person, (b) Regions is not acting as an advisor to any municipal entity or obligated person and does not owe a fiduciary duty pursuant to Section 15B of the Securities Exchange Act of 1934 to any municipal entity or obligated person with respect to such presentation, information, materials or communications, (c) Regions is acting for its own interests, and (d) you should discuss this presentation and any such other information, materials or communications with any and all internal and external advisors and experts that you deem appropriate before acting on this presentation or any such other information, materials or communications.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.