Download Asset Allocation | August 2025

Running on Empty

Economic Update

Data Weakens the Outlook

By Regions Economic Division

August arrives like a closing curtain – summer’s final act. Vacations wind down, and heat loses its grip, as the long days shorten. As children shoulder backpacks and return to school, tariffs return, and uncertainty lingers on who will bear the higher cost of imports. The air may be cooling, but geopolitical tensions burn hotter. Israeli Prime Minister Netanyahu has declared intentions to takeover Gaza, and the casualties continue to mount in the Russo-Ukrainian War. As Jackson Browne once sang, “Try not to confuse it with what you do to survive.”

As U.S. equity markets climb to new altitudes, the air shows signs of thinning. Sector leadership has narrowed, and momentum is slowing. Announced policy shifts to allowable investments in 401(k)s and other defined contribution plans add another layer of uncertainty around long-term capital flows into public equity markets. Equity performance, investor sentiment, and earnings continue to surpass expectations. People need some reason to believe, and for now, markets are singing the tune they want to hear. Will the positive data continue to outweigh the negative? Or will the optimism driving markets run out, as portfolios are ultimately forced to pay the price of tariffs, inflation, and a slowing economy?

The initial estimate from the Bureau of Economic Analysis (BEA) pegs Q2 real GDP growth at an annual rate of 3.0%, while real private domestic demand – combined business and household spending – grew at an annual rate of 1.2 percent. For the most part, the Q2 data flipped the script from Q1 when real GDP contracted at a 0.5% rate and real private domestic demand grew at a 1.9% rate. Still, rather than telling us much about the state of the U.S. economy, we see the GDP data for the first half of 2025 as pretty much of a wash, with the Q1 data materially impacted by businesses and households acting to preempt anticipated increases in tariffs and the Q2 data largely reflecting payback.

This leaves the question of where the economy goes from here. What we and others are trying to determine at present is whether what we’re seeing in the data is the slowdown in growth that was widely anticipated at the start of this year happening much less smoothly than anticipated, or whether the economy is genuinely starting to sag under the weight of higher tariffs, shortages of labor, persistent price pressures, and a heightened degree of uncertainty. Answering this question, at least correctly, is made more challenging by the higher frequency data remaining somewhat volatile and many of the data series sending conflicting signals. That may not change soon.

In any given quarter, the BEA’s initial estimate of GDP is based on highly incomplete source data and prone to sizable revision as holes in the data are filled in and prior estimates of source data are revised. As the data now stands, real imports of goods fell at an annual rate of 35.3% in Q2 after having risen to an annual rate of 51.6% in Q1. With imports treated as a deduction under GDP accounting conventions, these sharp swings in imports of goods wreaked havoc with the GDP data over the first two quarters of 2025, knocking off 4.84 percentage points off real GDP growth in Q1 and adding 5.02 percentage points in Q2.

The sharp swings in goods imports over this year’s first two quarters were largely driven by efforts to stockpile inventories ahead of anticipated tariff increases (Q1) which brought payback in subsequent months (Q2), as is reflected in the GDP data on business inventories. For instance, the much faster rate of inventory accumulation in Q1 added 2.59 percentage points to real GDP growth. During Q2, however, businesses began to pare down those inventories, to a degree that knocked 3.17 percentage points off Q2 real GDP growth.

While these swings in goods imports and business inventories had significant, but opposite, effects on top-line real GDP growth over the first two quarters of 2025, neither told us much about underlying economic conditions. This is an illustration of why we repeatedly stress real private domestic demand as a better indicator of the underlying health of the U.S. economy than is top-line real GDP. That said, real private domestic demand was not immune to the swings seen in real GDP over the first two quarters of the year, reflecting businesses and households acting to avoid higher tariffs and subsequent payback in the data.

After having grown at an annual rate of 1.9% in Q1, real private domestic demand grew at an annual rate of 1.2% in Q2. To be sure, assessing how much of the slowdown in growth of real private domestic demand in Q2 reflected payback and how much reflected the broader economy having lost momentum is not neatly spelled out in the data, and there is room for debate as to the relative weights. Moreover, in several instances the monthly patterns of activity haven’t strictly conformed to calendar quarters, meaning that the Q3 data could also reflect payback from earlier activity. As such, the prints on real GDP and real private domestic demand may not bring as much clarity as we’d like.

When it comes to the recent labor market data, any clarity would be welcomed. Total nonfarm payrolls rose by just 73,000 jobs in July, less than the expected increase. That headline job growth was on the light side of expectations, however, was not the biggest surprise in the July employment report. That distinction goes to the magnitude of the revisions to prior estimates of job growth in May and June, with a net downward revision of 258,000 jobs over the two-month period. To say that market participants reacted badly to that surprise would be an understatement, as equity prices and yields on U.S. Treasury securities plummeted after the release of the report while many analysts rushed to downgrade their outlooks for the labor market and the broader economy. That the July employment report came just two days after the FOMC left the Fed funds rate unchanged at their July meeting led many to argue that the Committee, save for Governors Bowman and Waller, who voted for a funds rate cut at the July meeting, was behind the curve. Very few of those making that argument on August 1, however, were making that argument when the FOMC meeting concluded on July 30.

We were just as surprised by the July employment report as anyone else, but nonetheless did what we always do, which was to work through the details of the data. The details of the July employment report show the downward revision to May job growth was far more a function of revised seasonal adjustment factors than revisions to actual job growth. Specifically, the estimate of seasonally adjusted May job growth was revised down by 120,000 jobs between the first and third estimates (the latter was incorporated into the July employment report), almost one-half of the net downward revision of 258,000 jobs for the May-June period. Based on the not seasonally adjusted data, the estimate of May job growth was revised down by only 23,000 jobs between the first and third estimates, a negligible revision to actual May growth.

We do not yet have the third estimate of June job growth, which will be incorporated into the August employment report to be released on September 5. For now, recall that the initial estimate of June job growth showed private sector payrolls rising by 74,000 jobs and public sector payrolls rising by 73,000 jobs. As we noted at the time, the reported increase in public sector payrolls was little more than seasonal adjustment noise around the education segment of state and local governments. Most of that reported increase went away upon the initial revision to the June data, as the estimate of the increase in public sector payrolls in June was cut by 62,000 jobs.

So, the bulk of the net downward revision to May-June job growth amounted to no more than noise in the data. To be sure, that still leaves a large downward revision to private sector job growth in June, now pegged at only 3,000 jobs, but we’ll reserve judgment until the August employment report is in hand. That said, those who rushed to judgment – on the state of the labor market, the state of the broader economy, the stance of monetary policy – in the wake of the July employment report basically did so on the basis of noise in the data. To us, the question isn’t whether or not there are concerns over labor market conditions but instead just how deep those concerns should be.

We do know that the trend rate of job growth has slowed, which thus far has been a function of a slowing pace of hiring as opposed to a faster pace of layoffs. We know that job growth has become meaningfully less broadly based across private sector industry groups over recent months. We also know that the foreign-born labor force has declined by 1.653 million persons over the past four months, which we believe to be a material drag on overall job growth. Finally, we know that the duration of unemployment has been increasing, meaning that while the pace of layoffs has not increased, those who do lose a job are having an increasingly difficult time finding a new job.

Our view is that, though having clearly cooled, the labor market is not as weak as implied by the July employment report. It is, however, hard to have much confidence in any take on the labor market given the issues with some of the data in the monthly employment reports. Those issues are unlikely to be resolved soon, thus leaving as many questions as answers.

Sources: Bureau of Economic Analysis; Bureau of Labor Statistics

Investment Strategy Update

Regions Multi-Asset Solutions & Highland Associates

While developed international continues to outperform the S&P 500 on a year-to-date basis, EAFE countries have had yet another month of relative underperformance. Developed international stocks were volatile last month. The MSCI EAFE developed markets index hit a new all-time high, with Japan the biggest contributor, before closing the month 1.4% lower, below its 50-day moving average, leaving the index in a precarious technical position. Some resolution on the trade front initially boosted foreign stocks but the rally was offset by the U.S. dollar rising by 3.2%, its largest monthly gain since April of 2022. Japanese equities were the victim of outsized currency moves as U.S. investors in the MSCI Japan Index saw prices decline by 1.7% in July, while dollar-hedged investors stateside experienced a 2.7% advance due to the fluctuation in the yen versus the U.S. dollar.

U.S. dollar weakness has helped drive performance for international developed in the first half of August. Valuations for stocks in the Eurozone and Japan were trading near parity as recently as June, but Japan has seen valuations get richer with a forward P/E ratio of 15.2 relative to a 14.0 P/E ratio for the MSCI Europe index. Investors seeking exposure to secular growth areas such as AI and data center buildout could find quite a bit to like in the MSCI Japan index, which has close to 40% of its exposure in the industrials and information technology sectors. The MSCI Europe, on the other hand, has less than 28% in those two sectors while carrying higher exposures to consumer staples and health care, two sectors that have been out of favor of late.

U.S. equity momentum is fading into a seasonally difficult period. Equity indices across the market capitalization spectrum turned out gains in July, with mid-caps outpacing large-cap and small-cap stocks, but under the surface breadth left something to be desired for bulls. While information technology stocks and artificial intelligence (AI) adjacent plays in the industrials and utilities sectors led the charge, energy was the only other S&P 500 sector to outperform the index on the month. The narrowness of S&P 500 leadership in July and at the start of August is notable after almost 90% of index constituents posted quarterly results with earnings per share thus far besting the consensus estimate by over 8.5%.

Earnings estimates have moved higher on the heels of strong earnings beats and improving investor sentiment, leading to a continuation of the rally that began in mid-April and pushing the S&P 500 higher by 28% on a closing basis off the April 8th low. The consensus estimate now calls for the S&P 500 to earn $66.82 in the 2nd quarter, up from $63.25 at the end of June, and full-year 2025 and 2026 estimates have moved higher in concert. Earnings estimates being revised higher by a few bucks in this operating environment is a byproduct of corporate America being more agile and adapting in a challenging and constantly evolving policy backdrop. It remains difficult for bears to make the case for being negative on U.S. stocks – particularly large-caps – without relying on historically lofty valuations as the reason for taking such a position. Even that argument holds little water when one remembers the current valuation for the S&P 500 is little changed from where it was five years ago. With earnings season winding down, and with ‘good news’ such as a U.S./EU trade deal and earnings beats failing to push the S&P 500 much higher, digestion or a modest pullback could lead to a healthy reset of expectations and act as a springboard into 4Q25 and beyond.

S&P 500 Price Has Nearly Doubled In The Last 5-Years – But Earnings Have Beat That

Source: Bloomberg

August has historically been a middling month for returns, with the S&P 500 generating an average return of 0.6% dating back to 1928. September, on the other hand, has historically been the worst month for the S&P 500 with the index declining by 1.1%, on average, during the month. September is the only calendar month in which the S&P 500 has declined more times than it has risen dating back to 1928. Should the bull run need to pause, this would be a logical spot in the calendar for it to do so, Contrarians take note, however, as the consensus appears to be aligned behind the idea that a pullback during this two-month period should be the base case Investors will shift their focus to 2026 in the coming months and optimism will likely dominate due to hopes of deregulation, favorable tax treatment for capital expenditures, the prospect of easier monetary policy, and potential productivity/profitability gains from AI.

S&P 500’s Valuation Is Little Changed After Delivering +15% Annualized

Source: Bloomberg

Emerging markets have also outperformed U.S. indices year to date, but unlike developed international, much of this has come strong performance came in recent months.Emerging market currencies generally fared better than their developed counterparts in July, which contributed to the MSCI Emerging Markets Equity index outpacing the MSCI EAFE by 3.4% on a total return basis. Trade agreements created a divide between the ‘haves’ and ‘have nots’ in July as countries who struck a deal or sidestepped the worst-case scenario on tariffs, including China, South Korea, and Taiwan, were among the top performers while tariff troubled nations such as Brazil and India lagged the broader MSCI EM index.

India’s weakness is notable as the country had provided consistent leadership post-COVID, but the MSCI India is below key moving averages and may remain challenged unless a trade deal with the U.S. can be struck., But, with the U.S. announcing it would levy 50% tariffs on imported goods from India at the end of August without a trade deal in place, further downside/weakness could be in the cards. From an asset allocation standpoint, we maintain a preference for emerging market stocks over developed markets abroad as developing markets are more levered to U.S. dollar weakness should the countertrend rally fade, and the signing of trade deals between the U.S. and Brazil, India, and/or Mexico could generate additional upside.

Duration drove positive performance on weak economic data last month, but further downside in bond yields is likely limited.A weak July nonfarm employment report put downward pressure on Treasury yields in early August as buyers bought bonds of all maturities hand over fist on heightened expectations of labor market weakness spurring the Federal Open Market Committee (FOMC) to cut the Fed funds rate at its September meeting. Fed funds futures rapidly repriced a September rate cut, from just a 40% probability to almost 90% on the heels of the employment report and projected a total of over 60- basis points of rate cuts prior to year-end at the time of this writing. For the bond market, the question appears to no longer be whether the FOMC will cut in September, but by how much. However, the expectations pendulum may have swung too far toward a more aggressive pace of monetary policy easing and the rally in higher quality, longer duration segments of the bond market at the start of this month is likely overdone as a result.

While the momentum behind the drop in Treasury yields in early August certainly got our attention, we question how much lower yields are likely to fall in the coming months for a few reasons. First, the inflation outlook remains clouded by tariff rhetoric and overall policy uncertainty which is unlikely to subside in the near-term, and if the FOMC does cut the funds rate in September, economic growth and inflation expectations could rise, putting upward pressure on yields. Second, from a technical perspective, it’s notable that the Treasury rally stalled out with the 10-year trading hands with a yield around 4.20%. The 10-year yield spiked to 4.80% in mid-January and bottomed out at 4% on “Liberation Day” in early April, but excluding those outlier events, each of which lasted less than two weeks, the 10-year yield has remained range-bound between 4.15% and 4.60% this year. 4.15% marked the bottom for the 10-year yield in early March and again at the end of April, and it would take a multi-week close below that level for us to view the early August rally as a character change and cause us to upgrade our outlook for core fixed income.

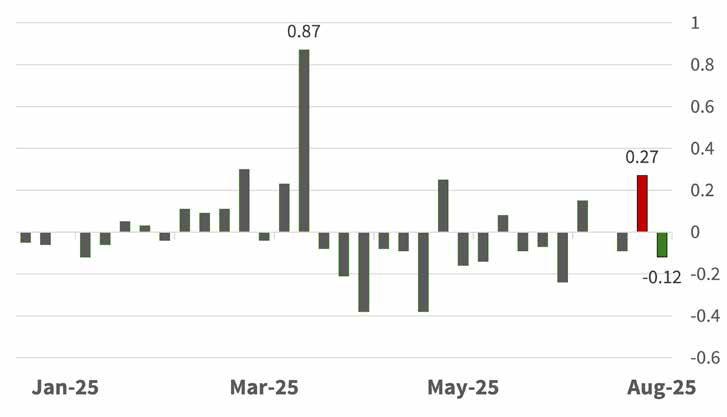

Corporate credit valuations experienced their largest one-day move since early April on August 1st as the July employment report showed sizable downward revisions to prior estimates of job growth in May and June. The weaker than expected report prompted the credit spread on the Bloomberg Corporate High Yield index to jump above 300- basis points over the Treasury curve from 281-bps the prior day. The abrupt early August spike in spreads proved to be short-lived as market participants quickly extrapolated the weak employment report to imply an increased likelihood of monetary policy easing coming sooner than previously expected. We still expect below investment grade credit to underperform relative value hedge fund strategies at these levels.

A few days later, high yield credit was again trading below 300-bps wide of Treasuries, and at around 289-bps spreads were just 20-basis points above the tightest level seen this year at the time of this writing. The speed at which credit regained its footing captures just how robust risk appetite remains, as credit spreads have tightened in each of the prior three months, but spreads could be poised to drift slightly higher in the near term. Rich valuations and impending seasonal factors are likely to limit gains in the coming months. The carry component measured by the yield-to-worst on the Bloomberg High Yield index is nearing a 12-month low at roughly 7%. For those that prefer liquid strategies over hedge funds, this still offers a relatively attractive value proposition in a benign environment.

High Yield Bonds Cheapened On Payrolls But Risk Appetite, Demand Quickly Returned (change in basis points)

Source: Bloomberg

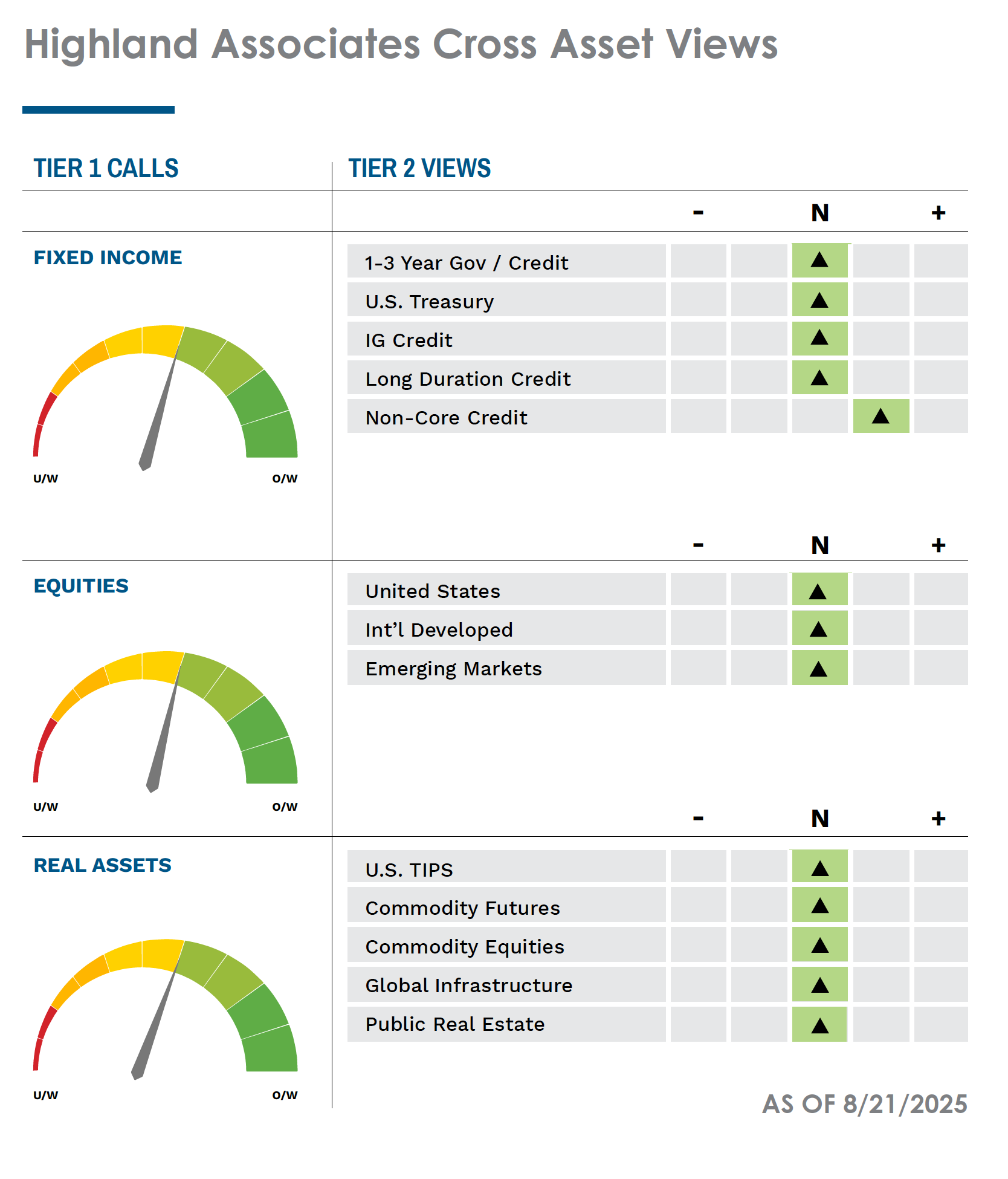

Portfolio Positioning

Highland Associates

We have remained in a neutral risk-position throughout the year. Within fixed income portfolios, many managers have been allocating capital away from investment grade corporates and into mortgage-backed securities, which offer more spread and better risk adjusted returns. As corporate credit spreads hover near all-time tights, the risk-reward of these positions has become less attractive, and we believe better entry opportunities will arise later in the year. Duration positioning has become less of a concern throughout the year, although we remain cautious of the long end of the curve. Despite the near-term performance, widening budget deficits and persistent inflation could drive long rates higher. The 5% yield level has demonstrated strong resistance for 30-year Treasuries throughout the year and is likely to continue to act as a ceiling. As the Fed looks to cut short-term rates, we expect the 3-month yield to fall faster than the belly of the curve and eventually un-invert versus the 5-year yield. Thus, we prefer the short- to intermediate- portion of the curve over the long-end. Equity portfolios remain neutrally positioned across geographies as international equities continue to outperform domestic equities. As the S&P 500 is hovering around all-time highs, momentum has faded, and we would not be surprised with more of an oscillating equity market in the 3rd quarter. With the massive investments flowing into Artificial Intelligence, we believe utilities could continue to benefit from a structural shift in demand for electricity. When looking across asset classes, inflation-sensitive portfolios should continue to provide attractive risk adjusted returns. We are currently in a rising growth/rising inflation environment, which tends to support equities and commodities. Hedge fund strategies should also benefit from oscillating markets, and we believe relative-value strategies can provide better downside protection for portfolios than higher equity beta assets like high yield.

We’ve heard throughout the year that investors have been happy with the yield on cash, but few seem to be factoring in inflation expectations. Because of persistently higher-than-target inflation, we would caution investors to focus more on inflation-adjusted yields rather than nominal yields. While a 1-Year Treasury is yielding 3.85% nominally, a year-over-year CPI reading of 3.1% equates to a real yield of only 0.75%. When factoring in breakeven inflation expectations, the 5-year Treasury real yield has continued to fall from its peak of 2% in January to currently around ~1.4%. The risk of losing purchasing power, combined with credit spreads near all-time tights, decreases the attractiveness of fixed income returns and we would look to alternative strategies with higher risk premiums to preserve purchasing power. Higher quality areas of the market such as AAA-rated CLOs and high quality CMBS may provide some additional returns to compensate for risks.

IMPORTANT DISCLOSURES: This publication has been prepared by the staff of Highland Associates, Inc. for distribution to, among others, Highland Associates, Inc. clients. Highland Associates is registered with the United States Security and Exchange Commission under the Investment Advisors Act of 1940. Highland Associates is a wholly owned subsidiary of Regions Bank, which in turn is a wholly owned subsidiary of Regions Financial Corporation. Research services are provided through Multi-Asset Solutions, a department of the Regions Asset Management business group within Regions Bank. The information and material contained herein is provided solely for general information purposes only. To the extent these materials reference Regions Bank data, such materials are not intended to be reflective or indicative of, and should not be relied upon as, the results of operations, financial conditions or performance of Regions Bank. Unless otherwise specifically stated, any views, opinions, analyses, estimates and strategies, as the case may be (“views”), expressed in this content are those of the respective authors and speakers named in those pieces and may differ from those of Regions Bank and/or other Regions Bank employees and affiliates. Views and estimates constitute our judgment as of the date of these materials, are often based on current market conditions, and are subject to change without notice. Any examples used are generic, hypothetical and for illustration purposes only. Any prices/quotes/statistics included have been obtained from sources believed to be reliable, but Highland Associates, Inc. does not warrant their completeness or accuracy. This information in no way constitutes research and should not be treated as such. The views expressed herein should not be construed as individual investment advice for any particular person or entity and are not intended as recommendations of particular securities, financial instruments, strategies or banking services for a particular person or entity. The names and marks of other companies or their services or products may be the trademarks of their owners and are used only to identify such companies or their services or products and not to indicate endorsement, sponsorship, or ownership by Regions or Highland Associates. Employees of Highland Associates, Inc., may have positions in securities or their derivatives that may be mentioned in this report. Additionally, Highland’s clients and companies affiliated with Highland Associates may hold positions in the mentioned companies in their portfolios or strategies. This material does not constitute an offer or an invitation by or on behalf of Highland Associates to any person or entity to buy or sell any security or financial instrument or engage in any banking service. Nothing in these materials constitutes investment, legal, accounting or tax advice. Non-deposit products including investments, securities, mutual funds, insurance products, crypto assets and annuities: Are Not FDIC-Insured I Are Not a Deposit I May Go Down in Value I Are Not Bank Guaranteed I Are Not Insured by Any Federal Government Agency I Are Not a Condition of Any Banking Activity.

Neither Regions Bank nor Regions Asset Management (collectively, “Regions”) are registered municipal advisors nor provide advice to municipal entities or obligated persons with respect to municipal financial products or the issuance of municipal securities (including regarding the structure, timing, terms and similar matters concerning municipal financial products or municipal securities issuances) or engage in the solicitation of municipal entities or obligated persons for such services. With respect to this presentation and any other information, materials or communications provided by Regions, (a) Regions is not recommending an action to any municipal entity or obligated person, (b) Regions is not acting as an advisor to any municipal entity or obligated person and does not owe a fiduciary duty pursuant to Section 15B of the Securities Exchange Act of 1934 to any municipal entity or obligated person with respect to such presentation, information, materials or communications, (c) Regions is acting for its own interests, and (d) you should discuss this presentation and any such other information, materials or communications with any and all internal and external advisors and experts that you deem appropriate before acting on this presentation or any such other information, materials or communications.

Source: Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.