Stocks: Government Shutdown Proves To Be A ‘Sell The News’ Event As U.S. Indices Struggle Amid More Signs Of Sector Rotation; Eurozone Strength Broad-Based, With Banks Leading The Charge; Investors In Emerging Markets Could Find Opportunities To Diversify AI Exposure In Latin America.

Download Weekly Market Commentary | November 17 2025

What We’re Watching:

- Semiconductor behemoth and ‘Magnificent 7’ member Nvidia reports quarterly results on Wednesday after the market closes, and the company’s outlook could dictate the direction of travel into year-end for semiconductor stocks specifically and companies tied to the buildout of artificial intelligence (AI) more broadly.

- Minutes from the FOMC’s October meeting are released Wednesday and will likely be parsed and dissected to gauge the most likely path forward for monetary policy. Fed funds futures currently have a rate cut in December as a coin-flip, but as the government reopens and economic data begins to flow again that figure is likely to shift and we could see an uptick in interest rate volatility as a result.

- S&P Global releases its U.S. Purchasing Managers Index (PMI) for November on Friday. Services PMI is expected to rise to 55.0 from 54.8 in October, while Manufacturing PMI is expected to fall modestly to 52.0 from 52.5 the prior month. A reading above 50 indicates expansion/growth, below 50 contraction.

Key Observations

- The end of the U.S. government shutdown mid-week proved to be a ‘buy the rumor, sell the news’ event with stocks across the market capitalization spectrum rising Monday and Tuesday before giving ground into the weekend. There were further signs of rotation out of artificial intelligence (AI) beneficiaries with profits being redeployed into value-oriented sectors such as energy, health care, and materials. It’s worth monitoring to see if last week’s rotation out of AI names is a healthy, short-lived shakeout, or whether it proves to be the canary in the coalmine marking a durable shift in market leadership into 2026.

- Abroad, developed and developing market indices had a good week as the U.S. dollar weakened modestly. Strength out of Europe was broad based with France, Italy, Spain, and Switzerland standout performers, while Japanese stocks moved sideways digesting sizable year-to-date gains for the second consecutive week. Within emerging markets, Brazil and South Africa took the leadership baton while South Korea, a strong performer year-to-date, recovered sizable losses from early in the week to close with a respectable gain.

- It was a non-event week in the Treasury market with yields across the curve closing little changed. However, with the government shutdown ending last week and economic data likely to start flowing as usual by early December, we expect an uptick in volatility for the rates market into the FOMC’s December 9-10 meeting.

What Happened Last Week:

Stocks: Government Shutdown Proves To Be A ‘Sell The News’ Event As U.S. Indices Struggle Amid More Signs Of Sector Rotation; Eurozone Strength Broad-Based, With Banks Leading The Charge; Investors In Emerging Markets Could Find Opportunities To Diversify AI Exposure In Latin America.

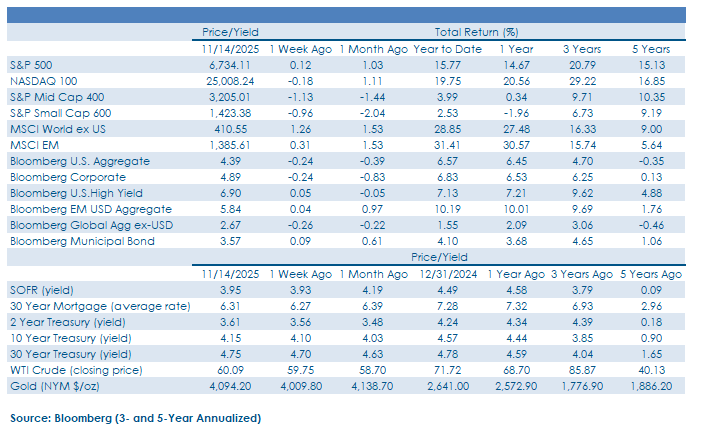

Just A Short-Lived Shakeout, Or Sign Of A Durable Leadership Shift As Value-Oriented Areas See Inflows. The S&P 500 eked out a 0.1% weekly gain even as a selloff took root in the back-half of the week as the U.S. government shutdown ended. There were again signs of sector rotation throughout the balance of the week as artificial intelligence (AI) beneficiaries associated with the industrials, information technology, and utilities sectors experienced profit taking while select value-oriented sectors such as energy, health care, and materials outperformed. Notably, the consumer staples, energy, and health care sectors are the only three S&P 500 sectors able to claim that over 50% of constituents are trading above their 20-day moving average. This provides evidence that there is indeed some short-term momentum behind the move into value that likely shouldn’t be ignored as this could be signs a leadership shift is afoot into the new year. Quietly, the energy sector has moved up the sector leadership ranks in recent weeks, and 100% of the sector’s constituents traded above their 20-day moving average as of last Friday. This improvement has taken place without a rally in West Texas Intermediate (WTI) crude oil which has continued to trade around $60 per barrel and has been unable to sustain gains but has coincided with a 30%+ rise in the price of Henry Hub natural gas since mid-October. Whether the bounce in the energy sector is a function of cheap valuations, rock-bottom expectations, an improving global growth outlook, or some combination of the three remains to be seen, but this could have implications for the inflation outlook and Treasury yields in the coming months should crude oil prices follow the sector’s lead and move higher.

Health Care Appears To Have The Wind At Its Sails. Health care has been the top performing S&P 500 sector month-to-date, rising 5.2% and far outpacing the S&P 500’s -1.4% drop. Encouragingly, strength out of the sector has been broad-based, but after a lost half-decade biotechnology and pharmaceutical stocks have finally started to garner investor interest and inflows. The health care sector broadly and biotech/pharma specifically may have multiple tailwinds in the coming year. First, investors believe that the timeline it will take for new drugs to be evaluated and potentially approved may be set to compress in the coming year(s) after the Food and Drug Administration (FDA) announced a new head of the Center for Drug Evaluation and Research, which is responsible for regulating most prescription drugs. Second, recent acquisitions have led to hopes that the coming year could be an active one on the mergers and acquisitions (M&A) front as Big Pharma moves to plug pipeline holes as some widely used and highly profitable drugs are set to lose patent exclusivity in the coming years. Lastly, in mid-term election years, the health care sector has historically performed quite well, and for investors seeking out more reasonable valuations, growth outside of AI, and earnings that will largely be independent of the economic backdrop, this sector could check a lot of boxes.

Strength Out Of Europe Stands Out As Banks Boost Developed Market Indices. European financials, specifically banks, led the charge within the MSCI EAFE index, as the Euro Stoxx Banks index registered a gain in excess of 4% on the week. That surge propelled country indices tied to France, Italy, and Spain to weekly gains, with each index returning over 2.5% in a week where most equity indices were flat to slightly higher. Price action out of European financials has been impressive this year as an improved outlook for earnings and more stable economic backdrop have boosted sentiment surrounding the sector, but it’s difficult to see how these heavily regulated institutions will unlock new profit engines necessary for this strength to persist. That said, momentum is a powerful force in markets, and we’d be hesitant to wager against a sector which has generated gains over the trailing 12-months that have outpaced even the S&P 500 information technology sector’s sizzling advance.

Emerging Market Investors Looking To Diversify AI Exposure Could Look To Latin America In The Coming Year. South Korea has been a strong performer year-to-date with the country’s KOSPI producing a gain of over 70% through last Friday, and even after pulling back sharply early last week, the KOSPI still gained 1.7%. South Korea’s positive momentum has been impressive, but, rightly or wrongly, the country is tech-heavy and viewed as a proxy for the health of the U.S. AI buildout. Further cracks in the AI armor stateside could lead to profit taking in some of South Korea’s national champions such as Samsung and SK Hynix, both of which have more than doubled this calendar year. While China, South Korea, and Taiwan have been strong performers this year as beneficiaries of the AI buildout, from a regional standpoint, Latin American equities could present an attractive opportunity for investors looking to diversify some of their AI exposure in the coming year. Brazil and Chile led the charge last week, with the former higher by 3.2% and the latter 1.8%, as prices of some commodity exports such as copper continue to rise and are supportive of additional foreign capital investment.

Bonds: Rate Volatility Could Ramp Up As Economic Data Starts To Roll In, Potentially Forcing Portfolio Repositioning; Investment Grade Spreads Still Elevated, Signaling Investor Caution; Emerging Market Debt Fares Well Despite Risk-Off Sentiment.

Lull In Interest Rate Volatility Could Be Near An End As Economic Data Begins To Flow Again. The U.S. government reopened last week, which means we are a few steps closer to receiving economic data. But will the state of the U.S. economy still match the bond market’s interpretation and positioning after over a month-plus in which we’ve been wandering in the economic data desert? Since the start of November, we’ve seen the Bloomberg Economic Surprise index point toward an improving economic backdrop, albeit on a blend of data obtained from private and limited public data sources, but intermediate-term rates are largely unchanged over that timeframe, thus opening the door for a sizable gap between what the economic data might start to show and how fixed income investors are positioned for what’s to come. That information gap likely played a role in keeping interest rates anchored last week, with the 10-year U.S. Treasury yield closing higher by 5-basis points at 4.15%, despite a risk-off narrative that permeated markets. Traders seemed hesitant to buy government bonds as a haven last week given uncertainty surrounding what fresh data might indicate on the inflation and labor market fronts in the coming month. In an environment such as this in which investors are biding their time waiting for data, the Bloomberg Aggregate bond is likely to fare well on a relative basis as investors balk at credit and duration sensitive instruments.

Investment Grade Credit Spreads At Multi-Month Highs Signal Investor Caution. Yields on high quality corporate bonds rose alongside Treasury yields at the end of October as FOMC Chair Jerome Powell called into question the market’s view that another cut to the Fed funds rate was all but guaranteed in December. Powell’s hawkish tone also spurred investors to reprice credit risk and forced the option adjusted spread (OAS), or credit spread on the Bloomberg U.S. Corporate index over comparable U.S. Treasuries higher to over 80-basis points for the first time since June. It’s been a challenging couple of months for corporate bonds as a couple of high-profile defaults forced credit spreads higher in early October as investors fearing a systemic credit event on the horizon required a higher yield to compensate them. But now investors appear to be more focused on the downside risks to the U.S. economy that could materialize should the FOMC pause in December, and the labor market continue to show signs of cooling.

Emerging Market Bonds A Bright Spot In A Risk-Off Market As EM Currencies Gain Ground On The Greenback. In a week where risk-appetite waned, emerging market debt marginally outperformed core U.S. fixed income, a counterintuitive move to some given the average credit quality differential, but we’ve long held the belief that EM debt is more than just a way for U.S.-based investors to benefit from taking on credit risk. Gains out of bonds tied to emerging economies was largely related to currency effects as the MSCI EM currency index notched its strongest weekly gain in over a month, leading the local currency bond index to a 0.5% return in a week in which many credit benchmarks were negative. Macro drivers, including currency movements, have buoyed emerging debt in recent weeks, but valuations in emerging bonds are far from attractive as the Bloomberg EM USD Aggregate spread ended last week at 1.8%, a fresh low unseen since 2007. This warrants a healthy level of caution.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.