Stocks: Another Record-Setting Week for U.S. Indices, Though Breadth Remains Narrow; Investors Bid Up Small Caps As The FOMC Delivers; Intel-Nvidia Partnership, Biotech Breakthroughs Dominate Headlines, Fuel Sector Rotation; Emerging Markets Outshine Europe.

Download Weekly Market Commentary | September 22 2025

What We’re Watching:

- S&P Global releases its preliminary September U.S. Purchasing Managers Index (PMI) Tuesday. Services PMI is projected to fall to 54.0 from 54.5 and Manufacturing PMI is expected to fall to 52.0 from 53.0 last month. A reading above 50 indicates expansion or growth, while a reading below 50 is indicative of contraction.

- Initial jobless claims for the week ended September 20 and continuing jobless claims for the week ended September 13 are released Thursday and are worth monitoring to see if both readings fall for the 2nd consecutive week.

- August Personal Consumption Expenditure (PCE), the FOMC’s preferred inflation gauge, is released Friday. Headline PCE is expected to have risen 0.3% month over month and 2.7% year over year during the month, while Core PCE, which is more closely watched by policymakers, is projected to rise 0.2% month over month and 2.9% year over year compared to 0.3% and 2.9% readings last month.

Key Observations

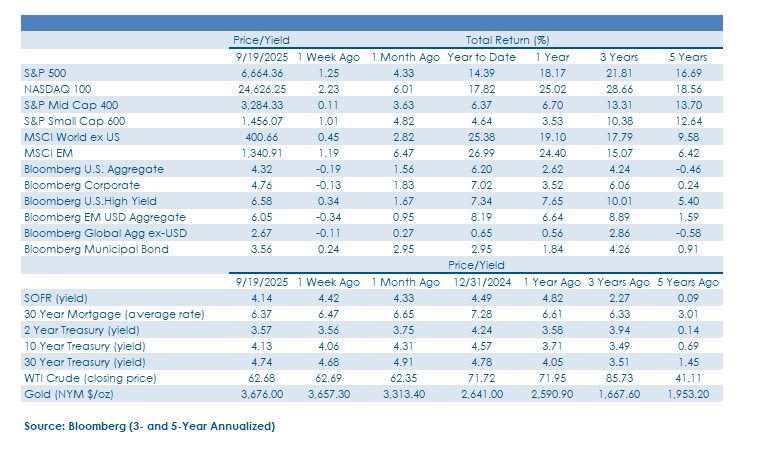

- U.S. stock indices continue to melt-up with small caps outperforming large caps on the week as the FOMC delivered on a rate cut and its closely watched dot plot pointed toward two more quarter-point cuts before year-end. Despite the rate cut and modest upward revision to economic growth in ’26 out of the FOMC, economically sensitive sectors such as financials, industrials, and materials failed to outpace the broader S&P 500 on the week. Communication services, consumer discretionary, and information technology outperformed due to exposures to ‘Magnificent 7’ names where stock-specific news garnered attention and capital.

- Emerging markets outpaced both U.S. and developed markets abroad on the week behind strength out of Brazil, India, and South Korea. Broadly speaking, emerging market currencies strengthened and credit spreads on emerging market debt narrowed on the week, further evidence of capital flowing into developing economies. This provides a constructive backdrop for EM stocks and bonds, and we expect both areas to perform well into year-end.

- Treasury yields moved higher after the FOMC’s decision to cut the Fed funds rate by 25-basis points on Wednesday as the Committee’s dot plot pointed toward expectations for upside to both economic growth and inflation next year. The 10-year yield bounced off 3.99% mid-week and ended the week higher, and with the FOMC’s dot plot pointing toward potential upside for economic growth and inflation next year, downside for yields in the belly of the U.S. Treasury curve appears limited.

What Happened Last Week:

Stocks: Another Record-Setting Week for U.S. Indices, Though Breadth Remains Narrow; Investors Bid Up Small Caps As The FOMC Delivers; Intel-Nvidia Partnership, Biotech Breakthroughs Dominate Headlines, Fuel Sector Rotation; Emerging Markets Outshine Europe.

Mega-Caps Keep Pushing Higher, But Cracks In Breadth Remain. U.S. large cap stocks notched another week of gains, though leadership remained concentrated in the largest technology and consumer discretionary names. ‘Magnificent 7’ member Alphabet became the 4th company to cross the $3 trillion market cap threshold, while Tesla advanced after Elon Musk increased his stake in the company, providing a lift to the communication services and consumer discretionary sectors. However, breadth narrowed meaningfully yet again, with the S&P 500 Equal Weight index closing the week higher by 0.1% compared to a 1.2% advance in the market cap-weighted S&P 500, reflecting the heavy reliance on mega cap leadership. Conversely, consumer staples, real estate, and utilities all lagged, highlighting some rotation out of defensive sectors after the mid-week rate cut as investors looked to sectors best positioned to benefit from a backdrop characterized by a modest improvement in the outlook for U.S. economic growth and inflation remaining elevated above the FOMC’s target for a prolonged period of time.

Small Caps Again Lead The Charge With Rate Cut Help On The Way. The Federal Open Market Committee (FOMC) delivered its first cut to the Fed funds rate since last September, trimming the target to 4.00%–4.25% from the prior 4.25% to 4.50%. FOMC Chair Powell emphasized the unusual combination of softer labor market dynamics and persistent inflation, noting “downside risks to employment” alongside “upside risks to inflation”. The response out of U.S. equities to the FOMC’s dot plot and outlook was initially mixed as the Dow 30 gained while the Nasdaq 100 slipped, financials outperformed, and information technology stocks pulled back. But what stood out most to us on the heels of the FOMC’s decision was the continued strength out of U.S. small cap stocks, with the S&P Small Cap 600 rising 1% on the week after profit-taking took hold into the weekend. The move higher in small caps reflects confidence on the part of investors that policy easing will boost U.S. economic growth while also lowering borrowing costs and improving free cash flow metrics for this cohort of stocks.

Company-Specific News Behind Sector Swings, Rotation. Semiconductor laggard Intel soared nearly 30% after Nvidia, the behemoth in the sector, announced a $5 billion strategic investment, signaling collaboration in custom data center products. Workday, a provider of enterprise cloud-based applications focused on financial and human capital management, rallied after the company authorized a $4 billion buyback and an activist investor pushing for change at the company noted “substantial progress” was being made in improving the company’s performance. The wind remained at the sails of biotechnology stocks as Moderna posted strong antibody trial results and Novo Nordisk reported positive updates across both oral and injectable diabetes drugs. On the downside, Warner Bros. Discovery slid on a downgrade and ongoing litigation concerns, while Uber dropped after Lyft deepened its Waymo partnership, providing a headwind to Uber’s expansion plans in autonomous driving. While the broader market largely remains beholden to moves in the mega cap names, last week’s price action shows that there are still plenty of company and stock-specific catalysts for skilled active managers to identify and profit from in an effort to deliver returns above their benchmark.

EM Rally Rolls On Behind Impressive Breadth, But U.K. Weakness Offsets Modest Gains Elsewhere. European equities were volatile last week as the MSCI Europe index fell sharply early in the week on bank weakness before stabilizing as euro area inflation held steady at 2.0%. The MSCI EAFE index closed the week lower by 0.1% as weakness out of the U.K. offset modest gains out of broader euro area indices. Emerging markets, by contrast, exhibited broad strength, evidenced by the MSCI EM index advancing 1.1%, led by gains out of Brazil, India, and South Korea. India slightly outperformed the broader MSCI EM index on the week amid continued signs of stabilization, and the potential for a U.S. trade deal is a potential catalyst for catch-up in the coming months. Additionally, capital inflows supported EM currencies, signaling greater investor confidence amid lower U.S. yields and tight credit spreads.

Bonds: Treasury Rally Stalls, Reverses Course On The Heels Of The FOMC Decision; High Yield Outperforms High Grade Corporate Bonds On The Week; The FOMC Delivers Dovish Dots While Raising Its Growth, Inflation Projections; France A Cautionary Tale And The BoE Stands Pat.

10-Year Yield Bounces As Investors Ratchet Up Growth, Inflation Expectations Alongside The FOMC’s New Dot Plot. There was a modest lift in the back end of the U.S. Treasury yield curve on the heels of the FOMC’s mid-week rate cut and the release of the Committee’s updated dot plot. That dot plot pointed toward another 50-basis points of rate cuts before year-end, a more aggressive path for the funds rate than we, and many others anticipated. The Committee’s updated projections also show that the median FOMC member expects U.S. economic growth and inflation in 2026 to be above where they thought it would be when the prior dot plot was released in June. These are notable shifts and likely contributed to the bounce in the 10-year Treasury yield which fell to 3.99% on Wednesday before closing just shy of 4.13%, ending the week 7 basis points above where it began. We see minimal downside for Treasury yields in the belly of the curve due to persistent inflationary pressures and the prospect of improved economic growth on the back of further cuts to the Fed funds rate. We are looking at the 3.99% level as support until further notice, while the 4.15%/4.20% zone could cap the upside move for the 10-year yield in the near term. However, a break above that zone could bring about a return to the days of the 4.20% to 4.50% trading range we grew accustomed to earlier this year.

High Yield Outperforms High Grade On The Week. Rising Treasury yields in the belly of the yield curve presented a headwind for higher quality and longer duration corporate bonds last week, contributing to a 0.1% weekly drop out of the Bloomberg U.S. Corporate Bond index. However, credit spreads remained contained with the option adjusted spread (OAS) for the Bloomberg Corporate index over the Treasury curve plumbing year-to-date lows around 71-basis points, the tightest level seen since 1998. On the other end of the spectrum, lower quality, shorter duration corporate bonds fared better as Treasury yields on shorter-term bonds closed experienced more modest moves on the week and the FOMC cutting the Fed funds rate spurred hopes of a more supportive economic growth backdrop and lower borrowing costs for this cohort of issuers.

Dovish Dots, But FOMC Chair’s Press Conference Was More Non-Committal. The Federal Open Market Committee (FOMC) wrapped up its two-day meeting last Wednesday and, as expected, announced a 25-basis point cut to the Fed funds rate. With the rate cut widely expected and priced in, investors focused on what the Committee’s updated Summary of Economic Projections, or dot plot, might portend for the path forward for rates. The Committee’s median dot pointed toward a total of 75-basis points of rate cuts in 2025, so another 50-bps between now and year-end, in essence a pull forward of one rate cut from early ‘26 versus what was previously expected. Perhaps most interestingly, the median dot showed that the Committee ratcheted higher expectations for both economic growth and inflation next year, while lowering its expectation for where the unemployment rate would be. Market participants took as further evidence the FOMC was intent on supporting the labor market and was increasingly less focused on the prospect of inflation expectations becoming unanchored or untethered.

On the surface, the updated dot plot appeared to meet the market’s dovish expectations, but in his post-meeting press conference Chair Jerome Powell was decidedly less dovish as he noted that the move could be considered a “risk management cut,” and kept the Committee’s options open moving forward. This is a divergence that market participants will have to square between now and the FOMC’s pre-Halloween meeting. Fed funds futures are aligned with the dot plot, pricing in an additional 45-basis points of cuts over the balance of this year, which leaves some room for the Fed to move at a more modest pace should labor market data improve or inflation readings surprise to the upside in the coming months, but the futures market also projects 50-bps of cuts next year, a quarter-point above the dots.

Investors Need To Pick Their Spots Abroad With France A Cautionary Tale. Yields on French OATs have risen materially over the past month, driven by a multitude of factors. First, the French government collapsed for the fourth time in 12 months after Prime Minister Francois Bayrou and his party lost in a no-confidence vote. Bayrou, a centrist, was attempting to slash government spending and gambled that he would receive support from either the left or the right wing. However, with the failure of the vote, both wings of the party have placed increased pressure on president Macron and new prime minister Sebastien Lecornu. Following the government dissolution, credit rating agency Fitch downgraded French debt from AA- to A+, citing the deteriorating fiscal position of the state and political instability as rationale.

Likely influenced by these factors, French 10-year borrowing costs rose above that of Italy, a country that has historically been known for facing funding challenges itself. Mr. Lecornu, a centrist, faces several challenges in his new, potentially short-lived role, including a debt to GDP of 113%, a budget deficit of 5.8%, and a need to spend to expand the French military to counteract increased Russian activity. Plans to address this situation by the previous administration involved eliminating two holidays, implementing a wealth tax for those worth over €100 million, and freezing government spending, all while maintaining balance with the wings of the party growing in influence. As such, French borrowing rates may be more closely linked to Italian rates rather than German bund yields going forward. Active management remains preferable when investing in developed market sovereign bonds as an in-the-weeds focus can help investors side-step policy pitfalls at the country level, allowing them to clip relatively attractive yields.

Bank Of England Stands Pat On Rates, Citing Potential Inflationary Pressures. On Thursday, the Bank of England voted to maintain current short-term interest rates at 4% on a 7-2 vote in a much less contentious meeting compared to last month when a secondary vote was required. The two dissenting members favored a 25-bps cut, while the majority noted upside risks to intermediate term inflation from the current 3.8% as the main reason to delay further cuts at this time. The decision to stand pat was already priced in with the British pound steady versus the U.S. dollar after the decision amid minimal volatility in rates markets.

What caught our attention out of the BoE’s announcement was the central bank’s balance sheet intentions and its potential impact on Gilt (U.K. debt) issuance. The BoE announced it would slow the pace of quantitative tightening or balance sheet runoff to £70 billion per year from £100 previously and will aim to sell fewer long maturity Gilts. That decision is to keep borrowing costs under wraps and avoid a spike in yields should the U.K. look to issue more debt farther out on the curve in the coming quarters. The trend of central banks abroad running off fewer long maturity bonds has been influenced to some degree by muted appetite for long-term sovereign debt by professional investors due to concerns surrounding fiscal policies and political turmoil, a dynamic likely to remain in place.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.