Stocks: Risk-Off Tone In The Lead-Up To Jackson Hole Shifts As Chair Powell Hints A September Rate Cut Is Likely; Breadth Better Than Feared With Weakness Centered Around The Technology Sector; European Equities Rally As Japan Consolidates; The Usual Suspects Continue To Lead As Capital Rotates In Emerging Markets.

Download Weekly Market Commentary | August 25 2025

What We’re Watching:

- The Conference Board will release its August Consumer Confidence Survey on Tuesday with the reading expected to fall month over month to 96.4 from 97.2 in July.

- Nvidia, the $4.5T semiconductor behemoth and largest constituent in the S&P 500 by market capitalization, is set to post quarterly results on Wednesday. Recent weakness in AI-related names could reverse course if Nvidia issues upbeat guidance.

- July Personal Consumption Expenditure (PCE), the FOMC’s preferred inflation gauge, is released Friday. Headline PCE is expected to rise 0.2% month over month and 2.6% year over year, compared to 0.3% and 2.6% in June. Core PCE, which is more closely monitored by policymakers, is expected to rise 0.3% month over month and 2.9% year over year versus 0.3% and 2.8% readings the prior month. Readings in line with consensus estimates would provide further evidence that inflationary pressures remain sticky with little progress toward returning to the FOMC’s stated 2% target having been made in recent months.

Key Observations

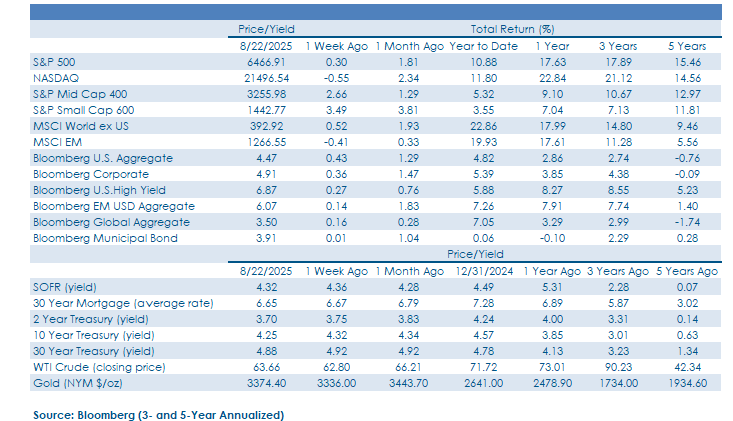

- Bulls regained control and pushed the S&P 500 to new intra-day and closing all-time highs on the heels of FOMC Chair Jerome Powell’s speech on Friday. Small- and mid-cap U.S. stocks would be bigger beneficiaries of lower interest rates and outperformed their larger capitalization peers into the weekend. The Fed cutting the funds rate in the coming months would provide a constructive backdrop for risk assets of all types, but the pendulum may have swung too far toward unbridled enthusiasm.

- Abroad, developed markets outperformed emerging markets due to strength out of Eurozone and U.K. equity indices while Japan took a breather. For emerging markets, strength out of China, India, and Mexico were offset by weakness out of Taiwan. Notably, there are signs that India has found a bottom, which would be welcomed by investors in developing markets. Weakness in the U.S. dollar into the weekend could also provide a persistent tailwind for improved relative performance abroad.

- Yields on U.S. Treasuries of all tenors fell on the week as hopes for a September rate cut dominated, offsetting upward pressure stemming from better-than-expected U.S. PMI’s and a continued lift in yields tied to developed markets abroad. Credit came under pressure throughout much of the week as market participants focused on the downside risks to the labor market and the U.S. economy. Those fears dissipated as Chair Powell struck a dovish tone, spurring a ‘buy everything’ mentality which contributed to a rally in investment-grade and high yield corporate bonds to close out the week.

What Happened Last Week:

Stocks: Risk-Off Tone In The Lead-Up To Jackson Hole Shifts As Chair Powell Hints A September Rate Cut Is Likely; Breadth Better Than Feared With Weakness Centered Around The Technology Sector; European Equities Rally As Japan Consolidates; The Usual Suspects Continue To Lead As Capital Rotates In Emerging Markets.

Profit Taking In AI-Related Names Before Nvidia’s Earnings Release Reverses Into The Weekend. Profit taking in some of this year’s biggest winners was evident again early last week as some of the highest-profile artificial intelligence (AI) beneficiaries lagged for the 3rd consecutive week as investors looked to de-risk portfolios in advance of Nvidia’s closely watched earnings release this Wednesday. Defensive sectors associated with lower volatility factors, specifically consumer staples and health care, outperformed early in the week as a risk-off tone took hold due to concerns that the Fed Chair would be more hawkish in his speech on Friday. But those concerns proved unwarranted and economically and interest rate-sensitive sectors such as consumer discretionary, energy, financial services, industrials, materials, and real estate rallied into the weekend as the FOMC Chair all but stated a rate cut was coming in September. On the AI front, many of the laggards early on in the week caught a bid on Friday as falling short-term interest rates would ease some of the valuation concerns surrounding this cohort of stocks. Active managers looking to play catch-up into year-end after lagging their benchmark will likely look at the AI cohort of stocks as a way to make up ground into year-end, and with rate cuts on the way, this could be a tailwind that materializes in the August/September timeframe. In the near-term. However, the path forward for AI plays likely hinges upon Nvidia’s guidance in the coming week.

European Equities Lead As Japan Takes A Well Deserved Breather. Lower beta stocks in developed markets abroad held up better than most with the MSCI EAFE index posting a respectable 0.8% weekly gain. Exposure to Italy, Spain, Switzerland, and the U.K. were leading contributors with a diverse blend of sector leadership that points to broader fundamental health in the continent’s equity markets, even as the dollar rose for most of the week. Promising strength out of the U.S. dollar reversed Friday after Fed Chair Powell suggested the U.S. labor market was in a “curious kind of balance” with downside risks to the labor market building, suggesting the U.S. economy may not be as resilient as it has appeared to be. Earnings growth out of developed nations abroad still has a long road ahead to rival U.S. companies, but it’s encouraging that European stocks were able to provide stability when called upon last week. The MSCI Japan index ended the week down just 0.3% as investors took profits after the Nikkei 225 closed at a new all-time high last Monday. Technically speaking, the Tokyo Stock Exchange (TOPIX) has been on a tear since its mid-July breakout, rising just over 10% in the last six weeks, which leads us to view last week’s consolidation as a healthy event.

The Usual Suspects Remain Leaders As Capital Rotates Between Emerging Markets. Reversals were a common theme across markets last week with emerging market equities following suit as recent leaders such as Brazil and Taiwan spent much of the week underwater while recent laggards such as India outperformed the MSCI EM index which fell by 0.4% on the week. The MSCI Taiwan index dropped 4.8% due to weakness in Taiwan Semiconductor as U.S. Trade Secretary Lutnick floated the idea that the administration was considering equity stakes in companies that received CHIPS Act subsidies. This announcement came after headlines broke that the U.S. government could take a 10% stake in Intel, a dynamic that feels akin to how China’s government integrates with large companies based there, but by the weekend the stance on owning foreign shares had been abandoned. Trade news on the U.S./India front hasn’t improved much, but with most investors already underweight, incrementally positive news on the country’s economic prospects could be enough to bring fundamental buyers back into the fold. Among the top performers, China and Mexico retained their leadership status with the pair generating gains of 1.6% and 2.2%, respectively, last week, with both now higher by over 29% or more on the year. The push higher in Chinese equities came from the technology sector as Nvidia’s call to halt H20 AI chip production was expected to benefit the country’s own chipmakers. The production pause in the H20 chip that was greenlighted specifically for China by the U.S. administration comes after policymakers in China started steering companies away from the chip due to national security concerns.

Bonds: Treasuries, Corporate Bonds Rally As Rate Cuts Are Priced Back In On FOMC Chair Powell’s Dovish About-Face; FOMC Minutes Are Stale But Still Worthy Of Discussion; Bets On A September Rate Cut Rise Sharply, But The Path Forward For The Fed Is Far From Certain.

Treasury Yields End The Week Lower As Rate Cuts Get Priced Back In. Despite the risk-off tone that forced U.S. equity indices lower on the week, there wasn’t much of a bid under Treasuries early last week, but FOMC Chair Powell’s Jackson Hole speech on Friday skewed more dovish than expected and generated a bid for bonds of all tenors into the weekend. Treasury yields bounced on Thursday after the release of the August preliminary Manufacturing PMI was expected to remain in contraction but topped the consensus forecast, coming in at 53.3 vs. the 49.7 estimate, while the Services PMI also surprised to the upside, coming in at 55.4 vs. the 54.2 estimate. The July PMI readings were supportive of the U.S. economic resiliency narrative, which along with the lift in sovereign bond yields abroad, served to put modest upward pressure on Treasury yields in the belly and long-end of the yield curve, But Chair Powell’s dovish comments Friday spurred buying, particularly in short-dated bonds, which led to a modest steepening of the yield curve. With the 10-year ending the week with a yield of 4.25%, we remain focused on the 4.20% area as a likely floor of support, which should limit total return potential for long-term U.S. Treasuries, broadly speaking, over the near-term.

Risk-Off Concerns Seeping Into Credit Quickly Subside. High yield corporate bonds got cheaper throughout the balance of last week in the lead-up to FOMC Chair Powell’s Friday speech, but he struck a more dovish tone than the market expected, and buyers quickly stepped in to bid up lower quality bonds. The Bloomberg U.S. Corporate High Yield index returned 0.2% on the week, falling short of the 0.4% rise in the Bloomberg Aggregate Bond index, but things could have been far worse for high yield. Before Chair Powell’s speech Friday buoyed sentiment, demand for below investment grade bonds appeared to be flagging as frothy valuations provided investors with little margin of safety should the Fed be unwilling to ease policy in the face of softening labor market conditions. We can track the price movement back to demand in part because there was no supply to speak off last week as both Jackson Hole and summer doldrums left the primary market frozen. The tide could turn in September as companies look to term out debt should all-in yields drift below the 7% threshold we saw earlier this month. At the end of the day, credit is certainly frothy but easier monetary policy justifies historically lofty valuations as the FOMC appears more focused on a softening labor market, reducing the risk of a recession or economic downturn in the offing.

FOMC Minutes Long On Tariffs, Inflation, And Labor Market Risks, But Already Stale. Last Wednesday, minutes from the FOMC’s July 29-30 meeting were released and we were most interested in whether more Committee members were close to joining the two known dissenters in favor of a rate cut. There were few signs that others were close to breaking rank and on balance the minutes appeared to take on a more hawkish tone than Chair Jerome Powell struck in his post-meeting press conference. On balance, while the minutes point to the Committee being more concerned with the upside risks to inflation stemming from tariffs as opposed to being focused on downside risks to the labor market, given perspectives and viewpoints likely would have been altered had the FOMC had access to the July employment report in advance, the minutes are stale and of little value in forecasting what the Committee is likely to do in September.

Upward Trend In Jobless Claims Back The Case For A September Rate Cut. Initial claims for unemployment insurance for the week ended August 16 were released Thursday and came in at 235k, above the 225k estimate. Continuing claims for the week ended August 9 were released the same day and rose from 1,953k the prior week to 1,972k, providing further evidence that those being laid off were finding it difficult to find new employment. While on the surface these readings don’t show that the labor market is collapsing, the upward trend in initial and continuing claims is worrisome and something the FOMC will be monitoring in the lead-up to its September 16-17 meeting. Minutes from the Committee’s July meeting showed the FOMC was more focused on potential upward pressure on inflation stemming from tariffs, but the weaker July employment report along with the upward trend in initial/continuing claims since mid-July may spur additional voters to back a rate cut next month to move the funds rate closer to ‘neutral.’ We continue to expect 50-basis points of cuts between now and year-end, and Fed funds futures are now pricing in an 81% likelihood of a cut in September after FOMC Chair Powell’s speech in Jackson Hole, up from 71% in the lead-up to his remarks.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.