Stocks: Bulls Firmly In Control, Push The S&P 500 To A Series Of All-Time High Closes; Small Caps Surge As Rate Cut Bets Rise; Japan Rally Rolls On, Boosting Foreign Developed Indices; China Boosts Emerging Market Index And Brazil’s Bounce Helps.

Download Weekly Market Commentary | August 18 2025

What We’re Watching:

- Minutes from the FOMC’s July 29-30 meeting will be released Wednesday. While we know that two FOMC voters dissented, the minutes will likely be parsed to gauge whether there were any other Committee members that were close to breaking rank and voting for a cut last month.

- S&P will release its preliminary August Manufacturing and Services Purchasing Managers Index (PMI) on Thursday. A reading of 49.8 is expected for the U.S. Manufacturing PMI which would be unchanged from July, while U.S. Services PMI is expected to fall to 54.2 from 55.7 the prior month. A reading above 50 indicates expansion/growth, while a reading below 50 indicates contraction.

- Initial jobless claims for the week ended August 16 and continuing jobless claims for the week ended August 9 are released Thursday and are worth watching for signs of further cooling in the labor market. The continuing claims data is of particular interest given the pattern in recent months for those that have been laid off to remain jobless for longer than we have grown accustomed to in recent years, a sign that companies are dragging their feet and are less eager to hire.

Key Observations

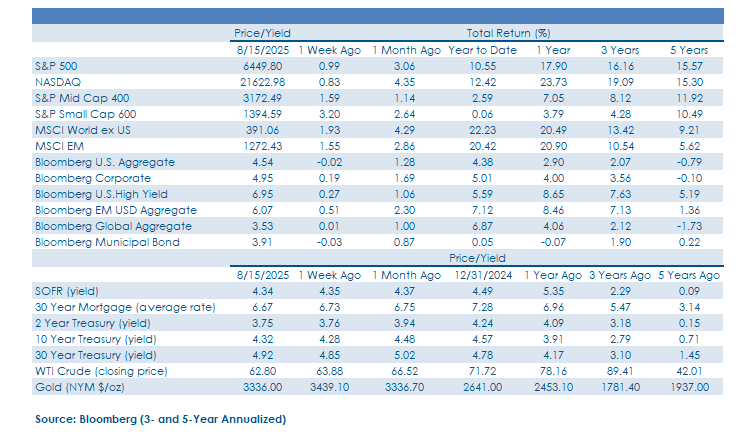

- U.S. large cap stocks remain on firm footing with the S&P 500 making a series of al-time highs on the week despite continued signs of rotation out of some of this year’s biggest winners tied to the buildout of artificial intelligence (AI) infrastructure and into laggards like homebuilders, biotechnology/pharmaceuticals, and small cap stocks, among others. Encouragingly, while the industrials, information technology, and utilities sectors lagged the S&P 500 on the week, consumer discretionary, communication services, and health care took the leadership baton and ran with it.

- Small cap stocks turned out their 2nd consecutive week of 2%-plus gains as investors implemented the rate cut playbook and bought some of the most heavily indebted companies that could be the biggest beneficiaries impending cuts to the Fed funds rate. Institutional investors have been carrying sizable short positions in small caps over recent months and strength could beget more strength as they are forced to cover those positions in the coming weeks.

- Japan continues to lead the way abroad and the country’s Nikkei 225 index posted another week of impressive gains on its way to an all-time high, but Eurozone and U.K. indices showed signs of life last week after lackluster relative returns in June and July. Measures of breadth show strong momentum behind the rally in Japanese stocks, but breadth measures across the Eurozone and the U.K. are more mixed and less convincing at present.

What Happened Last Week:

Stocks: Bulls Firmly In Control, Push The S&P 500 To A Series Of All-Time High Closes; Small Caps Surge As Rate Cut Bets Rise; Japan Rally Rolls On, Boosting Foreign Developed Indices; China Boosts Emerging Market Index And Brazil’s Bounce Helps.

You Can’t Keep A Strong Market Down As U.S. Large Caps Hit All-Time Highs. Broad-based strength pushed the S&P 500 to a new all-time closing high on three occasions last week, and even a hotter than expected July PPI reading Thursday failed to derail the rally with the S&P 500 reversing opening losses to end the day in positive territory. There were more signs of rotation under the surface as investors took profits in some of the biggest beneficiaries of the buildout of AI infrastructure in the engineering/construction, semiconductor, and cooling/energy management industry groups and redeployed capital into laggards such as small-caps, biotechnology/pharmaceuticals, and software names, among others. Homebuilding related stocks continued to surge, with the SPDR Homebuilders ETF (XHB) gaining another 4.8% on the week, taking its month-to-date gain to 11.2% as investors have implemented the rate-cut playbook in recent weeks and the 30-year mortgage rate reached a 2025 low on Friday. All told, we remain encouraged by the sector leadership profile of the market as the communication services, consumer discretionary, financials, health care, and materials sectors outperformed the S&P 500 last week, while the information technology sector took a back seat and modestly underperformed the headline index. We view this as a positive development and sign that indices can move higher even if capital rotates out of tech in a material way. It’s worth noting that just 52% of S&P 500 constituents were trading above their 20-day moving average at the end of last week, a sign the index has lost some momentum in recent weeks. However, just shy of 70% of index constituents were trading above the 100-day moving average, evidence of solid breadth over an intermediate-term time horizon which gives us comfort that U.S. large caps remain on firm footing.

Small Caps Surge Alongside Rate Cut Hopes. The S&P 600 Small Cap index has now put together consecutive weekly gains exceeding 2% after last week’s 3.2% advance, taking the index to its highest level since May. The accelerated advance was brought on by a steep decline in 2-year rates/yields as the July CPI allowed investors to get their hopes up that the Fed would be in rate cutting mode starting in September, with three 25-basis point cuts before year-end a not so farfetched possibility. Comments from Treasury Secretary Bessent suggesting 150-bps of cuts could be in order added to the rush of buyers in short-dated Treasuries, but yields turned higher as Core Producer Price Inflation (PPI) rose by 0.9% in July. The backup in yields weighed on small cap stocks into the weekend but market participants still appear to be willing to look through tariffs and focus on implementing the rate cut playbook, at least for now. From a technical perspective, the S&P Small Cap 600 remains well above its key 200-day moving average and now rests just 1.8% below its year-to-date high. Small cap stocks will likely take their cue from FOMC Chair Jerome Powell’s comments this Friday in Jackson Hole, with the rally continuing and pushing the index back to 2025 highs or leading to profit taking and a reversal of the recent good fortunes and animal spirits surrounding this cohort of stocks.

More Companies Going Public A Positive, But IPO Price Action Is Throwing Up A Caution Flag. Capital markets activity remained robust last week with application software company Bullish (BLSH) going public on Wednesday, taking North American IPO volume to $35.5B in 2025, a 38.6% improvement over last year’s volume at this point in the year. Bullish is just the latest in a string of recent high-profile IPOs, following on the heels of names like Circle, CoreWeave, Figma, Firefly Aerospace, and Sailpoint, to name a few, to go public in the past six months. While more companies going public is a sign of improved corporate confidence and ample liquidity, we may be teetering on the brink of too much IPO volume as price action in the days following the pricing of recent IPOs has left something to be desired. Case in point, Bullish priced above the high-end of its expected range at $37, spiked to north of $110 after it began trading, only to reverse course and close out the week around $70. While investors who were able to get in on the IPO in the pre-market were able to turn quick profits, retail investors buying after the issue began trading hoping to get in on the next IPO winner likely took on sizable losses in short order. We’re concerned there may be too much enthusiasm driving new issue activity at present, and investors should view forthcoming IPOs through a more cautious lens as some froth needs to come out of this corner of the market.

Japan Leading The Charge Abroad But EU, U.K. Equities Have Joined The Party. The MSCI Japan index continued to charge higher last week, tacking on another 3.7% on its way to an 8.5% monthly return. From a breadth perspective, shorter- and intermediate-term measures of participation are impressive with over 82% of Nikkei 225 constituents trading above their 20-day moving average and over 84% trading above their 100-day moving average at the end of last week, serving as evidence of broad-based momentum behind the move. Japan’s Tokyo Stock Exchange, or TOPIX, index which has greater exposure to less well-known smaller capitalization stocks than the Nikkei 225, also gained 3.11% last week and is higher by 8.1% in August, providing further evidence that demand for Japanese equities remains robust and has broadened out beyond large caps – this is far from bearish. Outside of Japan, it was nice to see Eurozone (+2.1%) and U.K. (+1.4%) indices participate for the 2nd consecutive week, but breadth measures across the Eurozone and the U.K. are more mixed and less convincing at present. We would like to see participation measures firm up in the coming weeks to provide investors with a sign the multi-month consolidation is over and the uptrend is set to resume.

Fading Trade Fears Boost Emerging Markets. The MSCI Emerging Markets (EM) index rose 1.5% on the week but fell short of its G10 counterpart (MSCI EAFE) even as Chinese equities, which account for the largest country weight in the index, advanced 2.9%. The enduring trend of strong performance out of the MSCI China index was prolonged by an extension of the 90-day trade truce with the U.S. which was followed by encouraging comments from the U.S. Administration. Positive price action stemming from the extension of trade talks coincided with earnings from Tencent, one of the country’s national champions, which beat expectations, and China’s government also announced new consumer-related stimulus efforts. Another rising star in the MSCI EM index last week was Brazil as President Lula unveiled sweeping aid to offset 50% U.S. tariffs, but questions remain as to how much fiscal flexibility the country has to increase spending to offset tariff pain. The technical setup is promising with the MSCI Brazil index now firmly above its 200-day moving average and not yet in overbought territory. If the index can retest and surpass its year to date high from July it could signal a more durable and positive trend change.

Bonds: Treasury Yields End The Week Unchanged To Modestly Higher As Investors Digest Mixed Inflation Data, Prepare For Jackson Hole This Week; Another Good Week For Credit As Spreads Narrow; Hot July PPI Muddies The Water For The Fed.

Treasury Yields End The Week Little Changed As Investors Digest July CPI, PPI In The Lead-Up To Jackson Hole. U.S. Treasury yields across the curve ended the week little changed but yields on shorter-term bills and notes moved modestly lower while yields on longer-dated notes and bonds moved modestly higher. The 2-year yield, which is more impacted by expectations surrounding the path forward for monetary policy, ended the week lower by 1-basis point. The modest move lower in the 2-year yield is evidence that while market participants may be a bit more confident the FOMC will cut the funds rate in September, they appear less convicted that the FOMC will be able to cut the funds rate by 75-basis points between now and year-end as they have been in recent weeks. The lack of movement in Treasury yields could also be a function of market participants sitting on their hands, unwilling to place their bets on rates/yields moving in either direction in the lead-up to the Kansas City Federal Reserve’s annual Jackson Hole Economic Symposium which runs from this Thursday through Saturday. FOMC Chair Jerome Powell is slated to speak on Friday, and his remarks will be closely parsed for signs as to which way he is leaning some three weeks out from the FOMC’s September meeting.

Inflation Data Muddies The Waters For The FOMC In September, And Beyond. The economic data point we were most closely watching last week was the release of the July Consumer Price Index (CPI) on Tuesday. Headline CPI rose 0.2% month over month and 2.7% year over year during the month, compared to the consensus estimate of 0.2% and 2.8%. Core CPI, which excludes food and energy prices and is more closely monitored by policymakers, rose 0.3% month over month and 3.1% year over year, versus the consensus which called for 0.3% and 3.0% readings. Higher prices for core services such as medical services and airfares drove the modest upside surprise to the consensus estimate, while, perhaps surprisingly, core goods prices came in a bit softer than expected. While the in-line CPI boosted expectations for a cut to the Fed funds rate in September, the release of the July PPI on Thursday threw cold water on expectations for aggressive monetary policy easing. The July Producer Price Index (PPI), which will flow into CPI in future months, came in hotter than expected across the board with headline PPI jumping 0.9% month over month and 3.3% year over year in July, with both readings well above the consensus estimates of 0.2% and 2.5%, respectively. Core PPI, which excludes food, energy, and trade, rose 0.6% month over month and 2.8% year over year, compared to consensus estimates of 0.2% and 2.5%. The debate among market participants on the heels of the CPI release centered around whether the FOMC had the cover to cut the Fed funds rate by 50-bps when it met in September, but hotter PPI lowers the odds of an outsized cut at that time. At the end of the week, Fed funds futures placed an 85% probability on a quarter-point cut in September, down from 93% last Thursday in the wake of the PPI release. Market participants also lowered expectations that the FOMC would be in cutting mode at all three of its remaining 2025 meetings, a view we agree with given our expectation that the FOMC will cut Fed funds by a total of 50 basis points between now and year-end.

A Good Week For Corporates As Credit Spreads Narrow. Investment grade corporate bond prices hit a new high for the year last Thursday, with the option-adjusted spread (OAS) on the Bloomberg U.S. Corporate index falling to just 75-bps over like Treasuries. That led the index to outpace the broader Bloomberg Aggregate benchmark on the week by 0.2%. The Bloomberg U.S. Corporate High Yield index outperformed its higher quality peer as credit spreads tightened a few basis points on the week, but the bulk of its 0.2% weekly advance came from yield/income. Some giveback for high yield bonds should be expected given the rally we’ve seen out of the asset class, which has seen only two weekly declines in the last three months. But at present appetite for low-grade debt remains robust, although potential buyers could reevaluate their conviction and desire to reach for yield given the challenging stretch in the calendar that lies ahead.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.