Stocks: Ceasefire and AI Send Nasdaq and S&P 500 to Record Highs, While The Dollar and Gold Slide As Investors Shed Safe Havens; Crude And Energy Equities Relinquish Recent Gains As Capital Flows Turn Back To Global Tech.

Download Weekly Market Commentary | June 30 2025

What We’re Watching:

- The Job Openings And Labor Turnover Survey (JOLTS) report is due out on Tuesday with the consensus estimating 7,300k job openings for the month of May, lower than the prior month openings number at 7,391k.

- Nonfarm Payrolls are set for release on Thursday in advance of the July 4th holiday, with forecasters anticipating 110k jobs added in June, a decline from the May reading at 139k. A weaker report could prompt the FOMC to give further consideration to lowering the Fed funds rate in the coming months.

- The Average Weekly Hours For All Employees will also be published by the Bureau of Labor Statistics on Thursday, with survey estimates expecting the reading to stand pat for the third consecutive month at 34.3 hours. A reading below that mark could indicate companies are cutting back hours to lower costs prior to reducing headcount.

Key Observations

- Risk sentiment reverberated through global equity markets, driving domestic indices to new all-time highs, as the truce between Israel and Iran pushed market participants out of commodities, including oil and gold, in favor of upside-oriented assets.

- Treasuries weren’t among the discarded haven trades last week, as intermediate and long-term rates declined after crude prices moderated, taking a potential commodity-related shock to inflation off the table for now.

- The third and final reading of first quarter US GDP came in at -0.5%, an uncommon shift lower from the prior reading, and consumer confidence fell off by more than the consensus estimate but markets are looking past the headline numbers with optimism towards trade.

What Happened Last Week:

Stocks: Ceasefire and AI Send Nasdaq and S&P 500 to Record Highs, While The Dollar and Gold Slide As Investors Shed Safe Havens; Crude And Energy Equities Relinquish Recent Gains As Capital Flows Turn Back To Global Tech.

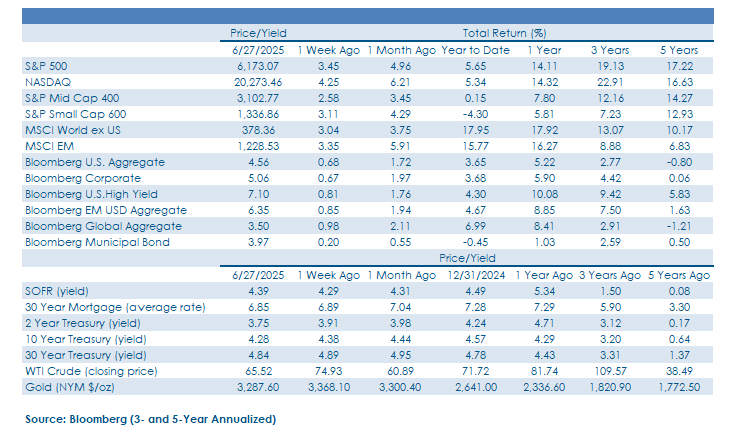

Ceasefire Outweighs Lacking Consumer Confidence As AI Optimism Reigns. Market participants were unphased by consumer confidence numbers released earlier last week, as global equities rallied on news of a fragile ceasefire between Israel and Iran that headlined much of Monday and Tuesday’s trading activity. The momentum in AI stocks proved its durability during the week as semiconductor names drove US equity markets, both the NASDAQ 100 and S&P 500 clinched new all-time highs to close the week as investors brushed off concerns over the trade war and Middle East tensions, capping a historic rebound for the quarter from the tariff-driven slump in April.

Semis Surge Around The Globe As South Korea Shrugs Off MSCI Snub. The spark in technology, specifically within semiconductors and e-commerce reverberated across the globe last week, with countries with extensive tech exposure including Tawain, South Korea, and China that all rose by more than 3% last week. Despite the announcement this week that South Korea would be excluded from the MSCI Developed Market Index during the firm’s annual market classification, Korean equities logged their highest trading volume in nearly two years during Tuesday’s trading session as the KOSPI broke 3,100—a level not seen since 2021. Strength was broad-based within global markets in the week prior as virtually all countries finished the week the week in the black, as conflict and trade concerns fade.

Dollar Drops, Gold Slips as Markets Rotate Into Risk Assets. The U.S. Dollar Index (DXY) reached a new low for the year last Thursday, falling to a three-year low of $97.15 as tensions in the Middle East moderated. If the dollar’s decline persists through the final days of the month, it will mark the steepest first-half decline since the advent of free-floating exchange rates in the early 1970’s. Gold spot prices fell 2.9% on the week, reaching a two-week low on Tuesday as the tenuous ceasefire between Israel and Iran weakened safe-haven demand for the precious metal. With geopolitical optimism coming out of Washington earlier in the week, the U.S. dollar, gold, and Japanese yen ended lower as investors rotated into risk assets.

Reality Check For Crude As Prices Plunge, Energy Sector Lags Crude prices dropped by as much as 6% on Tuesday alone as the devolving situation in the Middle East turned the corner early last week. Negative investor sentiment within commodities carried over into equity markets as the energy sector was the worst performing sector, closing the week down 3.4%. US West Texas Intermediate Futures contracts closed at $65.52 per barrel, an 11% decline on the week that reduces the risk of a near-term commodity shock to inflation.

Bonds: Corporate Debt Issuance In Full Swing As Treasuries Advance For The Third Consecutive Week And Crude Oil Concerns Collapse; Dollar Decline A Setup For Further Strength In Emerging Debt.

Long-term Treasuries See Price Gains Persist After Commodity Inflation Concerns Ease and US Growth Gets Revised Lower. Fixed income markets traded higher for the third consecutive week, as market participants ramped up treasury purchases after the recent shock higher in oil prices evaporated on news Israel and Iran had reached a ceasefire agreement. The sharp decline in crude prices led US inflation breakeven rates lower and had a hand in pulling the yield on 10-year treasuries to 4.28%, lower by 10bps on the week. The momentum in yields was sustained by the final reading on first quarter US GDP that was revised below survey estimates to -0.5%, in part due to weaker consumer spending with both goods and services taking a hit in the completed data. That slowdown in spending is noteworthy when considering services inflation is the primary component keeping Core PCE inflation above the Fed’s target, but risk assets including credit are taking their growth expectations from future economic forecasts and the high frequency data including the Atlanta Fed’s GDP Now forecast that ended the week at 2.9%.

Investment Grade Corporate Bond Issuance Comes Through Despite Conflict. The recent decline in interest rates is getting attention from corporate borrowers, with roughly $37B in new paper coming to market, making last week one of the busiest for bond issuance of the year thus far. Companies appear to be rushing to tap bond markets after absolute yields on the investment grade corporate bond index have declined by roughly 30bps in the last 30 days, with the yield-to-worst on the index at 5.06% at the end of last week. The shift lower in absolute yields carried the Bloomberg Corporate Credit Index to a 0.7% gain over the course of the week, outpacing the Bloomberg High Yield Index total return of 0.8%. Investment Grade credit spreads tightened early in the week after positive news surrounding the conflict between Israel and Iran reignited risk appetite, but spreads settled modestly wider as the influx of primary market deals likely tested the limits of investor demand. The uptick corporate bond issuance, paired with what we’ve seen out of recent initial public offering (IPO) success, bodes well for potential merger activity or CAPEX spending as firms have adequate capital on hand.

Emerging Market Bonds Backing Up Trends In Emerging Equities As Banxico Cuts. Bonds tied to developing economies were one of strongest segments in global fixed income last week, as the duo of dollar depreciation and lower interest rates brought the Bloomberg Emerging Market USD Aggregate Bond Index to a 0.9% gain on the week. Emerging market currencies continue to thrive at the dollar’s expense and the MSCI Emerging market currency index remains in one of the strongest uptrends we’re tracking across major asset classes. Growth trends in the most prominent issuers within the index are another beneficial country-level factor for debtholders evidenced by Mexico’s Central Bank, or Banxico, electing to ease monetary policy as growth expectations come in as the country emphasizes fiscal restraint. Lower deficit spending and slower growth expectations in Mexico could put bondholders in a prime position to collect higher yields with less price disruption.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.