Stocks: Investor Sentiment, Risk Appetite Subdued With Tariffs A Moving Target; U.S. Dollar Slides As Capital Flows From The U.S. To Europe, Allowing The Renaissance For Euro Area Stocks To Continue; Fiscal, Monetary Policies Supportive Of Further Gains For Euro Area, U.K. Equities.

Download Weekly Market Commentary | March 10 2025

What We’re Watching:

- The National Federation of Independent Business (NFIB) Small Business Optimism survey for February is released Tuesday with a reading of 101.0 expected, which would be a modest drop from the 102.8 reading in January.

- The February Consumer Price Index (CPI) is released Wednesday. Headline CPI is expected to rise 0.3% month over month and 2.9% year over year, this compares to 0.5% and 3.0% readings the prior month. Core CPI, which is more closely watched by policymakers, is expected to rise 0.3% month over month and 3.2% year over year versus 0.4% and 3.3% readings in January.

- The March preliminary University of Michigan Consumer Sentiment index is released Friday with a reading of 63.5 expected versus 64.7 in February. The February UMich survey sparked concerns surrounding the health of the U.S. consumer after a sharp drop in the future expectations component of the release and an equally concerning sharp upward move in the 5-to-10-year inflation outlook. We don’t expect much improvement this month, but some stabilization in these metrics would be welcome.

Key Observations

- U.S. stocks remained volatile with a downward bias amid more signs of cooling in the labor market and continued saber rattling on tariffs which weighed on investor risk appetite. Eurozone and U.K. stocks continued to benefit from concerns surrounding an economic slowdown stateside, with capital flowing out of the U.S. appearing to find a home across the pond. Accommodative monetary policies and the prospect of stepped-up fiscal support in the euro area are reasons to believe relative outperformance can persist.

- The S&P 500 bounced off its 200-day moving average at 5,730 on multiple occasions throughout the week and, encouragingly, closed above this closely watched level on Friday. The S&P 500 last closed below its 200-day moving average in October of 2023, and a weekly close under this key support level could turn support into resistance and usher in additional selling.

- The U.S. Dollar fell sharply versus the euro, British pound, and Japanese yen last week as U.S. tariffs on Canada, China, and Mexico went into effect, while Germany and the European Union expressed a willingness to step up military spending in defense of Ukraine. Increased fiscal spending could generate upside surprises to euro area economic growth in the coming quarters, and with the U.S. economy slowing while Europe is potentially poised to grow faster than previously expected or feared, the euro could remain strong versus the greenback as capital is attracted to higher yielding currencies.

What Happened Last Week:

Stocks: Investor Sentiment, Risk Appetite Subdued With Tariffs A Moving Target; U.S. Dollar Slides As Capital Flows From The U.S. To Europe, Allowing The Renaissance For Euro Area Stocks To Continue; Fiscal, Monetary Policies Supportive Of Further Gains For Euro Area, U.K. Equities.

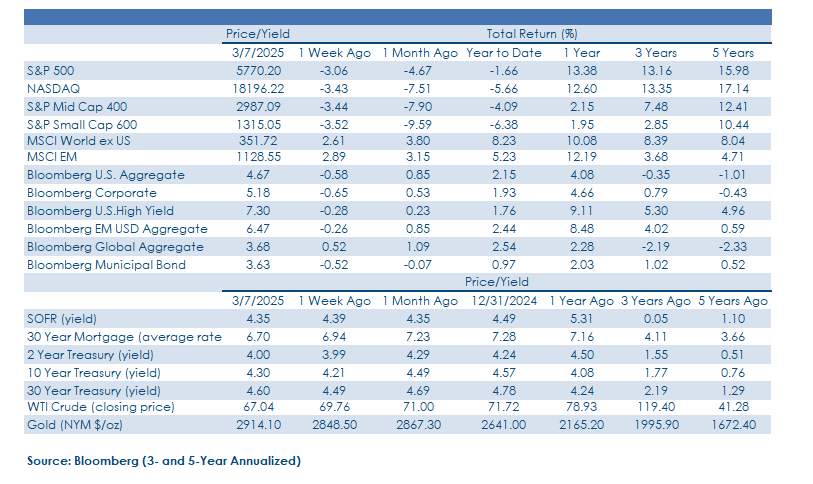

Headlines, Trade Uncertainty Continue To Weigh On Sentiment, Risk Appetite. The S&P 500 opened higher on Monday amid hopes for a last-minute resolution on the trade front, but gains proved fleeting as those hopes were dashed and tariffs on Canada, China, and Mexico went into effect as outlined on Tuesday. U.S. stocks continued to slide mid-week even as the Trump administration announced it would delay tariffs on some imports from Mexico until April 2, providing a reprieve for U.S. automakers, specifically, for another month. The S&P 500 fell 3% on the week, while the more U.S.-centric S&P Small Cap 600 Index fared worse, falling 3.5%. With tariffs garnering headlines and likely to remain a moving target and subject to change, investors will likely remain more comfortable on the sidelines with de- risked portfolios as they await some needed clarity on this front before redeploying capital back into U.S. stocks.

After Holding Up Well Last Month, Some Of February’s Winners Succumb To Selling Pressure. The energy and financial services sectors of the S&P 500 were two surprising winners in February, rising 3.2% and 1.2%, respectively, easily outpacing the S&P 500’s 1.4% monthly decline. The strong relative performance out of these two sectors during the month was surprising due to the package of economic data we received during February which, on balance, pointed toward the U.S. economy slowing, a backdrop that would normally weigh on cyclical sectors such as these. While the energy and financial services sectors helped prop up the S&P 500 during February, the opposite proved true last week with energy falling 3.7% and financials dropping 5.9%, contributing to the 3% weekly decline for the broader index.

U.S. Dollar Weakness Throws Fuel On The Fire For The Rally In Developed And Emerging Market Stocks. The U.S. Dollar Index, or DXY, fell sharply as U.S. tariffs on imported goods from Canada, China, and Mexico went into effect and more economic data pointed toward a U.S. slowdown taking place. Contributing the move lower in the greenback was the move higher in the euro amid hopes that Germany and the EU were move open to stimulating the eurozone’s economy. The DXY fell from 107.56 on February 28 to 103.85 last Friday, a 3.4% slide in just one week’s time – a rapid and unsettling move to be sure. We viewed the 105.70 level as a potential target on the downside as the DXY made a double-bottom there in November/December of 2024, but after slicing through that level we are now watching to see if 103.40, or the November pre-election low, holds and acts as support. The U.S. dollar’s drop has provided fuel for the rally abroad to start the year as capital flows have shifted in favor of Europe relative to the U.S. and further weakness would continue to buoy developed and emerging market stocks abroad. U.S. multinationals in the Notably, while developed and emerging market stocks abroad would be the biggest beneficiaries of a weaker dollar, a weaker dollar could also drum up demand in international markets for multinationals in the S&P 500, while offsetting potential headwinds from higher tariffs being levied by some of the U.S.’ largest trading partners.

U.S. Dollar Weakness, Prospect Of Fiscal Support Driving Europe’s Comeback. The MSCI Germany Index and broader MSCI Europe Index made new highs last week, returning 6.2% and 3.3% respectively, as German officials outlined plans to ease fiscal constraints in a bid to boost defense spending and growth. A potential policy pivot away from austerity and the century-long ‘German Debt Brake’ is a potential watershed moment and comes as euro area countries face the prospect of footing a higher portion of the bill in helping Ukraine defend itself against Russian forces. It should be noted that Germany’s outline is just that, and what can ultimately be agreed upon by the EU may look very different and perhaps fall short of lofty expectations. But the fact that Germany has publicly voiced its willingness to end fiscal austerity for the first time since World War II highlights the gravity of the situation and should bring fellow EU members to the table for serious discussions. We remain comfortable with our current neutral allocation to international developed market stocks, but we wouldn’t chase the move higher as many euro area country indices are either fast approaching or are already in overbought territory and could pull back amid any signs that some EU members are balking at Germany’s plan.

Bonds: Treasury Yields Close Little Changed, But Short-Dated Bonds Rally As The Economic Slowdown Narrative Picks Up Steam; Upward Pressure On Developed Market Sovereign Yields Abroad As Fiscal Stimulus Hopes Build In Europe; February Payrolls Point To Continued Labor Market Cooling, But Not A Collapse.

Yields On Short-Dated Treasuries Close Little Changed Even As Rate Cut Odds Rise, While The Long End Moves Higher As Euro Area Sovereign Yields Provide A Lift. Yields on shorter- dated U.S. Treasuries fell modestly over the balance of last week as continued signs of softness in the economic data spurred an uptick in bets that the FOMC would need to step in and cut rates more aggressively this year, with a total of 75-basis points of cuts now expected. The 2-year Treasury yield rose 1-basis point on the week to 4.0% even as slower economic growth and rate cuts were priced in, but the long-end of the Treasury curve was less focused on the economic data and was more in tune with the move higher in euro area sovereign bond yields, and the 10-year yield closed 9-basis points higher on the week at 4.30%.

Services Still In Good Shape While Manufacturing Teeters On The Cusp Of Contraction. Yields across the curve fell early in the week as the ISM Manufacturing Index for February was released Monday and came in at 50.3, barely in expansion territory above 50, shy of the 50.7 estimate and the 50.9 reading from January. On Wednesday, the release of the ISM Services Index put upward pressure on yields across the curve after coming in better than expected at 53.5 vs. the 52.5 estimate.

Euro Area Sovereign Yields Rise Sharply As Germany Voices Support For Fiscal Stimulus. The prospect of fiscal stimulus/spending in the euro area generated a sharp move higher for euro area sovereign bond yields with the yield on the 10-year German bund, specifically, rising 43 basis points on the week to close at 2.835%, its highest level since October of 2023. The rise in yields contributed to a meaningful rally in the euro which appreciated by 4.4% versus the U.S. dollar at 1.083€ to $1, its highest close since November. The European Central Bank (ECB) cut policy rates again last week while expressing renewed confidence that recent upticks in inflation are due to lag effects and that disinflation is well underway. Seismic shifts in eurozone spending policies are likely necessary and a welcome change for the economically sensitive economies in the bloc, but getting a consensus of member states in support of a sizable spending package is far from a guarantee at this juncture. Euro area sovereign yields could push higher in the near-term on hopes for fiscal stimulus, but expectations may already be ahead of reality and current yields appear relatively attractive, particularly on a currency hedged basis for U.S. investors.

February Payrolls Further Evidence Of A Cooling Labor Market, But One Not Yet Collapsing. February Nonfarm Payrolls grew by 151k in February, below the 160k expected in the latest sign that the labor market continues to cool but isn’t yet collapsing. The unemployment rate ticked higher to 4.1% from 4.0% in January and the labor force participation rate moved modestly lower to 62.4% from 62.6% in January. Payrolls growth in the prior two months was revised lower by a net 2k jobs, but January, specifically, was revised to 125k from 143k previously, highlighting recent deterioration in the labor market. We’ve seen the February payrolls report described as the “lull before the layoffs” with some 100k federal layoffs likely to flow through the data in the coming months, and payrolls growth is likely to decelerate further as corporations appear increasingly hesitant to hire given uncertainty on the trade/tariff front.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.