Stocks: Large-Caps Melt-Up As Investors Return From The Thanksgiving Break; S&P 500 Ends The Week Higher As The ‘Magnificent 7’ All Catch A Bid; U.S. Small- Caps Cede Ground As Capital Rotates Out Of Economically Sensitive Sectors; China, India Bounce, But Political Dysfunction Weighs On Euro Area, South Korean Stocks.

Download Weekly Market Commentary | December 9 2024

What We’re Watching:

- U.S. Consumer Price Index (CPI) for November is released Wednesday. Headline CPI is expected to rise 0.3% month over month and 2.7% year over year versus 0.2% and 2.6% readings in October. Core CPI, which excludes volatile food and energy prices and tends to be a more closely watched metric by policymakers, is expected to rise 0.3% month over month and 3.3% year over year versus 0.3% and 3.3% readings the prior month, providing further evidence of ‘stickiness’ in the inflation data.

- The European Central Bank (ECB) meets Thursday and is expected to lower its key deposit facility rate by another 25-basis points, which would lead to a total of 1%, or 100-basis points of cuts this calendar year. The futures market also expects the ECB to cut by a quarter-point at its January, March, and April meetings as well as the euro area economy has been in a malaise. There’s a significant difference between cutting rates/easing policy because you can and because you have to, and the ECB falls firmly in the less desirable latter camp at present.

Key Observations

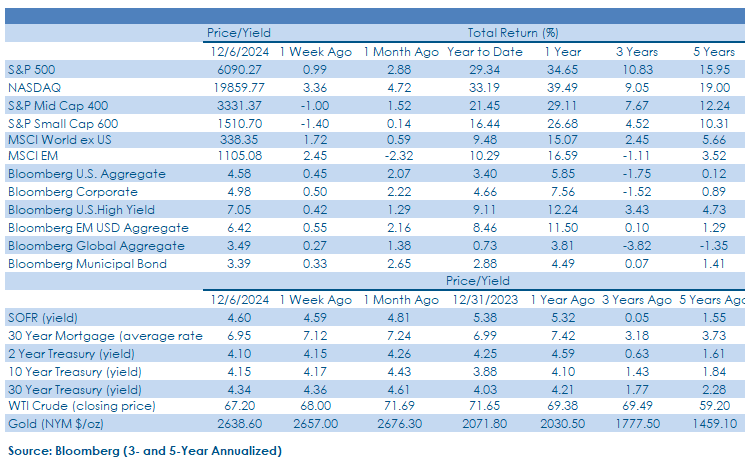

- U.S. large-cap stocks were in melt-up mode as capital rotated out of post-election leaders in the small and mid-cap areas and found its way back into year-to- date winners in the communication services, consumer discretionary, and information technology sectors, among others. The ‘Magnificent 7’ all rallied 2% or more on the week and outperformed the S&P 500.

- Small- and mid-cap (SMid) U.S. stocks, which had outperformed post-election amid hopes for deregulation and a more active mergers and acquisitions (M&A) environment in the coming years under the Trump administration, were sources of funds last week and lagged U.S. large caps as investors flocked back into the ‘Magnificent 7’ as portfolio window dressing took hold.

- Treasury yields ended the week little changed as fixed income investors digested a flurry of economic data releases and Fed chatter which resulted in Fed funds futures pricing in an 85% chance of a 25-basis point rate cut in December, up from 66% the day after Thanksgiving. The 10-year Treasury yield again encountered resistance around the 4.15% level, reinforcing our view that this is a key level worth watching as a break below could bring 4% into play in short order.

What Happened Last Week:

Stocks: Large-Caps Melt-Up As Investors Return From The Thanksgiving Break; S&P 500 Ends The Week Higher As The ‘Magnificent 7’ All Catch A Bid; U.S. Small- Caps Cede Ground As Capital Rotates Out Of Economically Sensitive Sectors; China, India Bounce, But Political Dysfunction Weighs On Euro Area, South Korean Stocks.

U.S. Large-Caps Melt-Up As Capital Rotates Back Into The ‘Magnificent 7.’. The S&P 500 closed the week higher by 1% with the broader index forced higher by the communication services, consumer discretionary, and information technology sectors as each ended the week with a gain of at least 2.5% with discretionary the big winner staging a 4.7% rally. After most constituents trailed the broader market post-election through Thanksgiving, the ‘Magnificent 7’ all caught bids with Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla each rising 3% or more on the week, while Apple turned out a weekly gain of around 2.3%. The Magnificent 7’s gains came at the expense of small and mid-cap (SMid) U.S. stocks as the S&P Small Cap 600 dropped 1.4% on the week and the S&P MidCap 400 fell 1%. The S&P 500 remains in a strong uptrend amid encouraging breadth with over 70% of constituents trading above their 200-day moving average as of last Friday, but momentum in recent weeks has been lackluster, leading to calls for a near-term market top and potentially a pullback into year-end. We see price action in recent weeks a bit differently and view the broader market moving sideways to modestly higher as the market’s way of building up the necessary energy for a push higher in the lead-up to Christmas. Low trading volume was a notable market characteristic last week, but this dynamic is a hallmark of early December trading following the Thanksgiving holiday. Trading volume is likely to pick up in the coming weeks as corporations buy back their own shares in advance of a new fiscal/calendar year, which should help put a floor under the market, particularly the S&P 500. Quarter/year-end rebalancing out of stocks and into bonds could act as an offset to buybacks to a degree in the coming weeks, but we still expect a healthy dose of holiday cheer to push stocks to new highs by year-end.

Political Dysfunction Rears Its Ugly Head Abroad, To A Mixed Response From Investors. Political discourse bubbled up in abroad last week as France and South Korea both experienced unsettling political events that rattled each country’s respective equity market. In France, the country’s parliament voted to oust the sitting prime minister via a no confidence vote due to his support of legislation supporting tax increases and budget cuts, which necessitated a new appointment from President Macron. Market participants brushed aside political uncertainty and the MSCI France Index gained 2.6% on the week as investors appear to be focused on the potential return of some long-awaited fiscal discipline in the country. This may not be the last we see political dysfunction hit the euro area in the near-term as Germany appears to be flirting with a similar move in the coming weeks, but there’s no guarantee that investors would cheer such an outcome there as they did in France. South Korea showed that it may still be deserving of the “emerging market” moniker after last week as the country’s president enacted martial law after a series of scandals decimated his approval rating. The shock factor of this move was apparent both in market reaction and in journalist accounts alike as the MSCI South Korea index declined by 4.3% on the week to a new year-to-date low even as martial law was quickly lifted by legislators. Unlike the situation in France, it’s unclear if the president will be impeached as his party holds a majority in the country’s parliament, but defending recent actions could cost officials their position in the next election cycle. Despite pockets of political uncertainty weighing on some country returns, the MSCI All-Country World ex-US Index gained 1.2% on the week as winners included Taiwan, Spain, Mexico, Italy, and Germany, again highlighting the importance of country selection both within developed and developing market indices abroad.

Bonds: Treasury Yields End The Week Modestly Lower As Investors Digest Economic Data, Fed Chatter, And Cabinet Appointments; Quietly Another Good Week For Emerging Market Debt On Its Way To A Strong Month.

Core Investment-Grade Bonds Post Gains As Yield Drop Boosts Longer Duration Assets. The Treasury yields were relatively unphased by a flurry of fresh labor market data which included upside surprises in the Job Openings and Labor Turnover Survey (JOLTS) as well as to the November nonfarm payrolls. Amid this backdrop, the Bloomberg Aggregate Bond Index managed to eke out its third consecutive weekly gain, returning 0.4. Investment grade corporate bonds performed quite well, evidenced by the Bloomberg U.S. Corporate Index gaining 0.5% on the week, modestly ahead of high yield corporates and in-line with emerging market debt.

Something For Both Bond Bulls And Bears To Cheer In The November Nonfarm Payrolls Report. Nonfarm payrolls grew by 227k in November, above the 220k consensus estimate, and payrolls for the prior two months were revised higher by an aggregate 56k jobs. Average hourly earnings rose 0.4% month over month and 4.0% year over year in the month, a notch above the 0.3% and 3.9% estimates. Payrolls growing above expectations and average hourly earnings surprising to the upside would argue for the FOMC to stand pat when it meets December 17-18, but the report also had some less desirable datapoints embedded in it as well. Specifically, the unemployment rate ticked higher to 4.2% during the month from 4.1% in October, and the labor force participation rate fell to 62.5%, below the 62.7% estimate and 62.6% the prior month. On balance, the November payrolls report modestly increases the likelihood of a quarter-point rate cut in December, in our view, but also increases the odds that the FOMC will pause in January and await more data before lowering the funds rate further. Fed funds futures shifted from pricing in a 70% probability of a cut last Thursday to 85% on Friday after the release.

Fed Speak Leans Toward A Cut In December, With Progress On Inflation Stalling Out A Risk In ‘25. Fed Governor Christoper Waller delivered a speech last Monday that presented a balanced argument for why the Committee should and shouldn’t ease policy later this month, but market participants ultimately viewed his remarks as skewing dovish and toward Waller being in favor of a rate cut in December. Waller addressed his concern that progress on inflation was stalling out with inflation meaningfully above the FOMC’s 2% target but noted that this is a risk, not a certainty. Market participants latched on to Waller’s quote that stated, “after reducing the policy rate 75 basis points since our September meeting, I believe that monetary policy is still restrictive and putting downward pressure on inflation without creating undesirable weakness in the labor market. I expect rate cuts to continue over the next year until we approach a more neutral setting of the policy rate.”

Emerging Market Debt Finding Its Footing As The U.S. Dollar’s Ascent Stalls. Bonds tied to developing economies found their footing mid-week and closed as one of the best performing fixed income segments with the Bloomberg USD Emerging Market Bond index turning out a 0.5% gain. A midweek decline in the US dollar provided a tailwind as emerging market currencies rallied versus the greenback and the Bloomberg EM Currency Index is attempting to carve out a near-term technical bottom around its 200- day moving average. EM debt’s struggles early last week coincided with a brief run up in US Treasury yields before the US 10-year ultimately reversed course and closed out the week modestly lower, a move that allowed credit spreads on EM bonds to narrow as higher yielding countries including Ecuador, Nigeria, and Peru outperformed. On the other hand, bonds tied to Argentina were volatile and prices fell on the week as inflation is now forecasted to tick modestly higher due to tax cut impacts, but a slight uptick was to be expected on the winding road to economic stability.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.