Stocks: The ‘Magnificent 7,’ Semiconductor Stocks Stage Impressive Rallies; Relative Calm Would Be Welcome, And Likely Healthy For The S&P 500; Small Caps Lag Despite Encouraging Economic Data.

Download Weekly Market Commentary | August 19 2024

What We’re Watching:

- Minutes from the Federal Open Market Committee’s (FOMC) July meeting will be released Wednesday and will be dissected for any clues as to how much dissention was in the Committee’s ranks when it met last month and how close it may have been to cutting rates at that time. The Kansas City Federal Reserve’s annual Jackson Hole Economic Policy Symposium kicks off Thursday with FOMC Chair Jerome Powell scheduled to speak on Friday morning.

- Initial Jobless Claims for the week ended August 17th and Continuing Jobless Claims for the week ended August 10th will be released Thursday. Along with upcoming inflation readings, labor market data will likely continue to garner headlines in the coming weeks in the lead-up to the FOMC’s September 17-18 meeting and investors will ratchet expectations for future policy easing higher or lower in response.

- Eurozone Purchasing Managers Index (PMI) for August is released Thursday. The Composite reading is expected to rise to 50.4 during the month from 50.2 in July with Manufacturing PMI falling to 45.5 from 45.8 the prior month and Services PMI falling to 51.5 from 51.9 in July. A reading above 50 indicates expansion or growth, below 50, contraction.

Key Observations

- Stocks staged a broad-based rally as investor risk appetite improved with U.S. large caps, U.S. small and mid-caps (SMid), international developed, and emerging market indices rebounding in unison. In the U.S., the consumer discretionary and information technology sectors, two of the worst performers in the early August pullback, led the charge as capital moved back into the ‘Magnificent 7’ and semiconductor stocks after many of those names sold off in recent weeks.

- U.S. small cap stocks rebounded as jobless claims data and retail sales pointed toward a resilient U.S. economy rather than one on the cusp of recession, but the bounce has been unimpressive as old habits die hard and investors appear eager to jump back into S&P 500 names with strong balance sheets tied to secular growth themes as opposed to economically sensitive small caps.

- Corporate bonds were the beneficiary of a series of not too hot and not too cold economic data releases last week as demand for credit returned despite issuance remaining well above levels from last year. U.S. dollar denominated emerging market debt was also a strong performer as the greenback continued to weaken versus most emerging market currencies, improving the fundamental outlook for a broad swath of developing economies and their ability to pay down debt.

What Happened Last Week:

Stocks: The ‘Magnificent 7,’ Semiconductor Stocks Stage Impressive Rallies; Relative Calm Would Be Welcome, And Likely Healthy For The S&P 500; Small Caps Lag Despite Encouraging Economic Data

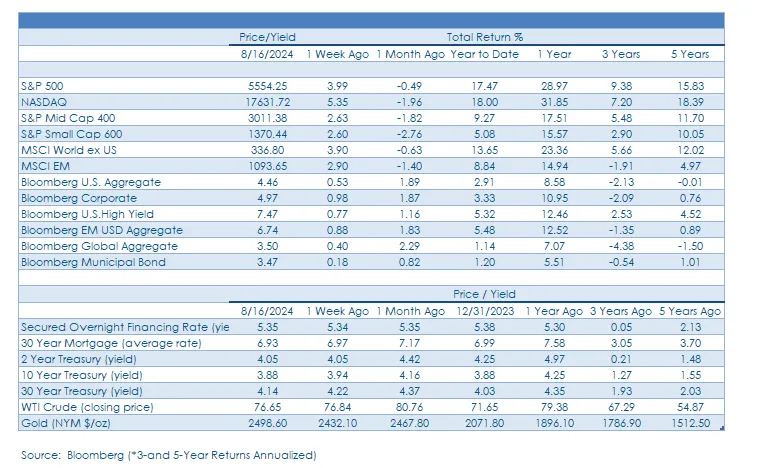

Risk Appetite Returns As Consumer Discretionary, Information Technology Leads The Charge. U.S. large cap stocks rallied last week, the S&P 500 rising just shy of 4% as good news on the inflation, labor market, and consumer spending fronts buoyed sentiment and improved risk appetite after a volatile two-week stretch. The S&P 500’s rebound from early August weakness has been impressive, but the market’s leadership profile left something to be desired as the consumer discretionary and information technology sectors were the only two sectors to outperform the broader S&P 500. Semiconductor stocks staged an impressive comeback, evidenced by a 9.8% gain out of the Philadelphia Semiconductor Index on the week, and the closely watched ‘Magnificent 7’ rode the coattails of Amazon (+8%), Nvidia (+18.9%), and Tesla (+8%) to a 6.2% weekly return. Economically sensitive sectors such as financial services, industrials, and materials each rose 2% or more on the week but failed to keep pace, despite a series of data releases that, on balance, pointed toward an economic soft landing while throwing cold water on the slowdown or recession narrative making the rounds in recent weeks.

After A Sharp Selloff And V-Shaped Recovery, A Period Of Relative Calm Would Be Welcome. After last week’s rally, the S&P 500 sits just 2% below its all-time high made in mid-July and, perhaps surprisingly, is back in positive territory month-to-date. Encouragingly, from a technical perspective, the S&P 500 closed out the week at 5,554 and the index is now back above its 50-day moving average which sits at 5,464. The move back above the 50-day has forced some systematic strategies to increase stock allocations after short-term signals told them to reduce exposure just a few weeks ago. With the bulk of that forced repositioning now behind us it would be healthy for the S&P 500 to retest support at its 50-day moving average in the coming weeks and move sideways as opposed to charging higher into overbought territory as a move such as this would invite sellers as trends become stretched or overextended.

Low Trading Volume, Limited Liquidity Can Lead To Big Moves In Both Directions. The recent bout of market volatility has been all but erased as the CBOE Volatility Index (VIX) settled last week at 14.8, below where it started the month, and back to where it was in mid-July. Spikes in the VIX can be notoriously short-lived, and August has been one of the most common spots in the calendar for volatility to spike with low trading volume and limited liquidity, or market depth, key contributors. Seasonal factors and the speed with which stocks recovered losses lead us to wonder if we’re simply in the eye of the volatility storm, but only time will tell. Periods of heightened volatility coinciding with pullbacks in stocks can present attractive opportunities to either rebalance portfolios or deploy cash for long-term investors as outsized moves during this stretch in the calendar on low trading volume and/or no news should likely be embraced.

Small Caps Get A Boost From Retail Sales But Still Lag Large Caps On The Week. The S&P 600 Small Cap Index generated a 2.6% gain on the week after rising 2.5% on Thursday as retail sales from July came in well above expectations. Markets ran up on the upside surprise in retail sales, interpreting the release as evidence that consumer spending remains robust, and that the odds of an economic slowdown or recession are lower now than they were a few weeks ago. The technical setup for small caps improved last week as the index closed above its 50-day moving average for the first time in almost two weeks, while not yet moving into overbought territory, a condition that had a hand in pulling capital away from smaller capitalization stocks late in July.

Bonds: ‘Goldilocks’ Economic Data Eases Fears Of A Slowdown; A Good Week For Corporate Bonds As Credit Spreads Narrow Despite Elevated Issuance; A September Rate Cut Remains Likely, But The Data Justifies Gradual, Not Aggressive, Policy Easing.

Treasury Yields Trade In A Narrow Range As ‘Goldilocks’ U.S. Economic Data Rolls In. Last week was a busy one on the economic data front with recent readings on inflation (CPI, PPI), retail sales, and the labor market all potentially market moving. Taken together, all the above data releases proved to be not too hot, nor too cold. On Tuesday, Producer Price Index (PPI) for July was released and both the headline and core readings came in light versus the consensus estimate. On Wednesday, the July Consumer Price Index (CPI) was released, with the headline and core readings in-line with consensus estimates and year over year readings ticking lower. Good news on the U.S. economy continued to roll in on Thursday with retail sales for July rising 1% month over month, well ahead of the 0.3% estimate, and initial jobless claims for the week ended August 10th came in at 227k, below the 233k estimate, while continuing jobless claims also came in below expectations. Wrapping up the week, the University of Michigan’s Consumer Sentiment Index for August was released Friday and improved to 67.8 from a 66.4 reading the prior month. Inflation data continues to point toward pressures gradually easing, while remaining sticky in some areas, and with PPI rising less than expected in July, prices of goods should continue to fall in the coming months. Initial and continuing jobless claims in recent weeks point toward signs of stabilization and potential improvement from July’s doldrums, easing concerns that a cracking labor market would quickly spillover and weigh on U.S. economic growth in the coming months. With a soft landing for the U.S. economy still our base case, we expect the 3.80% to 3.85% range on the 10-year Treasury yield to provide a floor of support in the coming months. It’s possible, given our outlook, that yields on long-term Treasuries rise as the FOMC begins to cut rates next month as less restrictive policy could lead to expectations that economic growth and/or inflationary pressures could reaccelerate in the coming quarters.

Credit Where Credit Is Due. Corporate credit markets have returned to form quickly with both investment grade and high yield bond indices returning 0.9% and 0.7%, respectively, last week. Prices rose across the credit-quality spectrum as wider spreads in recent weeks attracted buyers and credit spreads fell to levels at or below where they started the month, recovering from the recent selloff. At the same time, Treasury yields fell further on continued signs inflationary pressures were gradually easing, albeit alongside signs of moderating economic growth as well. That backdrop should bode well for corporate bonds, broadly speaking. The speed at which corporate bonds have undone the damage that stemmed from an economic growth scare can be attributed to several factors. Selling pressure was limited due to strong fundamentals of underlying issuers, as well as the constructive technical backdrop in place even as demand has held firm with new issuance orderbooks last week oversubscribed relative to historical norms, despite supply increasing 26% year on year.

Emerging Market Bonds Remain A Strong Performer. The U.S. Dollar Index’s (DXY) weakening trend persisted last week, registering it’s third consecutive weekly decline relative a basket of emerging market currencies. Emerging market bond indices have been beneficiaries of stronger EM currencies in August and the credit spread for the Bloomberg USD Emerging Market Aggregate Bond Index narrowed by 9-basis points last week to 271-basis points over Treasuries with a similar maturity due to an improved outlook on the ability for many countries to pay down debt. Spread tightening was largely concentrated in higher yielding issues with Argentina, Ecuador, and Chile among last week’s leaders while returns in higher quality names like Saudi Arabia and Brazil were modest. The Bloomberg Emerging Markets USD Index returned 0.8% last week on its way to a 5.4% year-to-date gain, and while we are tempering our expectations for the asset class a bit over the near-term, the 6.7% yield-to-worst on the index provides investors with adequate compensation to remain allocated to this segment of the fixed income market.

July Inflation Data Gives The FOMC The Cover To Cut In September, But Makes A 50-Basis Point Move Less Likely. The July Producer Price Index (PPI) was released Tuesday, with the headline reading rising 0.1% month over month, below the 0.2% estimate, and the 2.2% year over year reading also below the 2.3% estimate. The following day, the Consumer Price Index (CPI) for July was released, with headline CPI rising 0.2% month over month, in-line with the consensus estimate, and the core reading, which excludes food and energy, also higher by 0.2% month over month. Wholesale prices (PPI) coming in cooler than expected should point toward a modest drop in prices of goods in the coming months, welcome news for consumers.

CPI, while not the FOMC’s preferred inflation measure, was undoubtedly the more closely monitored of the two readings by policymakers, and with the headline reading rising 2.9% year over year and core CPI higher by 3.2% year over year, Committee members are seeing progress, albeit slower than they would like. On the heels of the PPI and CPI releases, along with improving jobless claims data and retail sales topping estimates, Fed funds futures lowered the odds of a more aggressive 50-basis point rate cut when the FOMC meets in

September to around 28% from closer to 55% early in the week and are now pricing in less than 100 basis points between now and year-end. On balance, the economic data released last week reinforces our view that a 25-bp cut in September is the most likely outcome, and we see no reason to alter our view that the FOMC will deliver a total of 75-basis points of cuts this year, with cuts in September, November, and December.

IMPORTANT DISCLOSURES: THIS PUBLICATION HAS BEEN PREPARED BY THE STAFF OF HIGHLAND ASSOCIATES, INC. FOR DISTRIBUTION TO, AMONG OTHERS, HIGHLAND ASSOCIATES, INC. CLIENTS. HIGHLAND ASSOCIATES IS REGISTERED WITH THE UNITED STATES SECURITY AND EXCHANGE COMMISSION UNDER THE INVESTMENT ADVISORS ACT OF 1940. HIGHLAND ASSOCIATES IS A WHOLLY OWNED SUBSIDIARY OF REGIONS BANK, WHICH IN TURN IS A WHOLLY OWNED SUBSIDIARY OF REGIONS FINANCIAL CORPORATION. RESEARCH SERVICES ARE PROVIDED THROUGH MULTI-ASSET SOLUTIONS, A DEPARTMENT OF THE REGIONS ASSET MANAGEMENT BUSINESS GROUP WITHIN REGIONS BANK. THE INFORMATION AND MATERIAL CONTAINED HEREIN IS PROVIDED SOLELY FOR GENERAL INFORMATION PURPOSES ONLY. TO THE EXTENT THESE MATERIALS REFERENCE REGIONS BANK DATA, SUCH MATERIALS ARE NOT INTENDED TO BE REFLECTIVE OR INDICATIVE OF, AND SHOULD NOT BE RELIED UPON AS, THE RESULTS OF OPERATIONS, FINANCIAL CONDITIONS OR PERFORMANCE OF REGIONS BANK. UNLESS OTHERWISE SPECIFICALLY STATED, ANY VIEWS, OPINIONS, ANALYSES, ESTIMATES AND STRATEGIES, AS THE CASE MAY BE (“VIEWS”), EXPRESSED IN THIS CONTENT ARE THOSE OF THE RESPECTIVE AUTHORS AND SPEAKERS NAMED IN THOSE PIECES AND MAY DIFFER FROM THOSE OF REGIONS BANK AND/OR OTHER REGIONS BANK EMPLOYEES AND AFFILIATES. VIEWS AND ESTIMATES CONSTITUTE OUR JUDGMENT AS OF THE DATE OF THESE MATERIALS, ARE OFTEN BASED ON CURRENT MARKET CONDITIONS, AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. ANY EXAMPLES USED ARE GENERIC, HYPOTHETICAL AND FOR ILLUSTRATION PURPOSES ONLY. ANY PRICES/QUOTES/STATISTICS INCLUDED HAVE BEEN OBTAINED FROM SOURCES BELIEVED TO BE RELIABLE, BUT HIGHLAND ASSOCIATES, INC. DOES NOT WARRANT THEIR COMPLETENESS OR ACCURACY. THIS INFORMATION IN NO WAY CONSTITUTES RESEARCH AND SHOULD NOT BE TREATED AS SUCH. THE VIEWS EXPRESSED HEREIN SHOULD NOT BE CONSTRUED AS INDIVIDUAL INVESTMENT ADVICE FOR ANY PARTICULAR PERSON OR ENTITY AND ARE NOT INTENDED AS RECOMMENDATIONS OF PARTICULAR SECURITIES, FINANCIAL INSTRUMENTS, STRATEGIES OR BANKING SERVICES FOR A PARTICULAR PERSON OR ENTITY. THE NAMES AND MARKS OF OTHER COMPANIES OR THEIR SERVICES OR PRODUCTS MAY BE THE TRADEMARKS OF THEIR OWNERS AND ARE USED ONLY TO IDENTIFY SUCH COMPANIES OR THEIR SERVICES OR PRODUCTS AND NOT TO INDICATE ENDORSEMENT, SPONSORSHIP, OR OWNERSHIP BY REGIONS OR HIGHLAND ASSOCIATES. EMPLOYEES OF HIGHLAND ASSOCIATES, INC., MAY HAVE POSITIONS IN SECURITIES OR THEIR DERIVATIVES THAT MAY BE MENTIONED IN THIS REPORT. ADDITIONALLY, HIGHLAND’S CLIENTS AND COMPANIES AFFILIATED WITH HIGHLAND ASSOCIATES MAY HOLD POSITIONS IN THE MENTIONED COMPANIES IN THEIR PORTFOLIOS OR STRATEGIES. THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR AN INVITATION BY OR ON BEHALF OF HIGHLAND ASSOCIATES TO ANY PERSON OR ENTITY TO BUY OR SELL ANY SECURITY OR FINANCIAL INSTRUMENT OR ENGAGE IN ANY BANKING SERVICE. NOTHING IN THESE MATERIALS CONSTITUTES INVESTMENT, LEGAL, ACCOUNTING OR TAX ADVICE. NON-DEPOSIT PRODUCTS INCLUDING INVESTMENTS, SECURITIES, MUTUAL FUNDS, INSURANCE PRODUCTS, CRYPTO ASSETS AND ANNUITIES: ARE NOT FDIC-INSURED I ARE NOT A DEPOSIT I MAY GO DOWN IN VALUE I ARE NOT BANK GUARANTEED I ARE NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY I ARE NOT A CONDITION OF ANY BANKING ACTIVITY.

NEITHER REGIONS BANK NOR REGIONS ASSET MANAGEMENT (COLLECTIVELY, “REGIONS”) ARE REGISTERED MUNICIPAL ADVISORS NOR PROVIDE ADVICE TO MUNICIPAL ENTITIES OR OBLIGATED PERSONS WITH RESPECT TO MUNICIPAL FINANCIAL PRODUCTS OR THE ISSUANCE OF MUNICIPAL SECURITIES (INCLUDING REGARDING THE STRUCTURE, TIMING, TERMS AND SIMILAR MATTERS CONCERNING MUNICIPAL FINANCIAL PRODUCTS OR MUNICIPAL SECURITIES ISSUANCES) OR ENGAGE IN THE SOLICITATION OF MUNICIPAL ENTITIES OR OBLIGATED PERSONS FOR SUCH SERVICES. WITH RESPECT TO THIS PRESENTATION AND ANY OTHER INFORMATION, MATERIALS OR COMMUNICATIONS PROVIDED BY REGIONS, (A) REGIONS IS NOT RECOMMENDING AN ACTION TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON, (B) REGIONS IS NOT ACTING AS AN ADVISOR TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON AND DOES NOT OWE A FIDUCIARY DUTY PURSUANT TO SECTION 15B OF THE SECURITIES EXCHANGE ACT OF 1934 TO ANY MUNICIPAL ENTITY OR OBLIGATED PERSON WITH RESPECT TO SUCH PRESENTATION, INFORMATION, MATERIALS OR COMMUNICATIONS, (C) REGIONS IS ACTING FOR ITS OWN INTERESTS, AND (D) YOU SHOULD DISCUSS THIS PRESENTATION AND ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS WITH ANY AND ALL INTERNAL AND EXTERNAL ADVISORS AND EXPERTS THAT YOU DEEM APPROPRIATE BEFORE ACTING ON THIS PRESENTATION OR ANY SUCH OTHER INFORMATION, MATERIALS OR COMMUNICATIONS.

SOURCE: BLOOMBERG INDEX SERVICES LIMITED. BLOOMBERG® IS A TRADEMARK AND SERVICE MARK OF BLOOMBERG FINANCE L.P. AND ITS AFFILIATES (COLLECTIVELY “BLOOMBERG”). BARCLAYS® IS A TRADEMARK AND SERVICE MARK OF BARCLAYS BANK PLC (COLLECTIVELY WITH ITS AFFILIATES, “BARCLAYS”), USED UNDER LICENSE. BLOOMBERG OR BLOOMBERG’S LICENSORS, INCLUDING BARCLAYS, OWN ALL PROPRIETARY RIGHTS IN THE BLOOMBERG BARCLAYS INDICES. NEITHER BLOOMBERG NOR BARCLAYS APPROVES OR ENDORSES THIS MATERIAL OR GUARANTEES THE ACCURACY OR COMPLETENESS OF ANY INFORMATION HEREIN, OR MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO THE RESULTS TO BE OBTAINED THEREFROM AND, TO THE MAXIMUM EXTENT ALLOWED BY LAW, NEITHER SHALL HAVE ANY LIABILITY OR RESPONSIBILITY FOR INJURY OR DAMAGES ARISING IN CONNECTION THEREWITH.